Seventy-one percent of U.S. consumers planned to spend at least as much on holiday gifts this year as they did in 2020, if not more, and buy now, pay later (BNPL) could prove to be a popular payment method among those looking to manage their budgets as holiday spending rises. BNPL programs enable shoppers to break up payments for their purchases into several installments without the additional interest that comes with traditional credit products.

Consumer interest in using BNPL to treat loved ones this holiday season is high, especially after enduring the pandemic for 21 months: 42% of BNPL-interested consumers cite this as the reason why they want to splurge using BNPL. Another 33% said they are still facing financial uncertainty because of the pandemic, but noted that they will have greater stability after the new year.

Consumers are looking to spend this holiday season, and BNPL options could help them treat not just themselves, but also their loved ones. This month, PYMNTS examines how BNPL could boost spending during the holidays as consumers reacquaint themselves with shopping for everything from travel tickets to holiday gifts.

Paying Tomorrow for a Happier Holiday Season Today

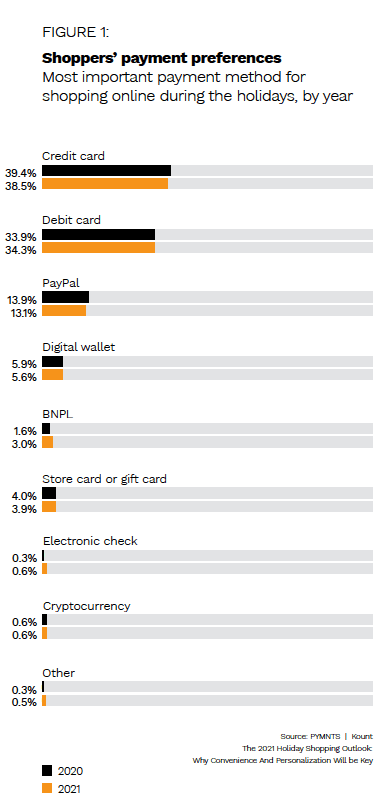

U.S. consumers expect to spend an average of $598 during the 2021 holiday season, compared to the $539 they expected to spend in 2020. With 76% of consumers looking forward to spending time with loved ones following the 2020 holiday season that saw reduced travel, 43% planned to give gifts related to experiences or services, including paying for travel or airline tickets. Among millennial consumers aged 32 to 39, 40% planned to pay for someone else’s travel expenses for the holidays, while 33% of Gen Z consumers expect to spend on experiences such as visits to amusement parks or weekend getaways. Additionally, the 3% of shoppers who told PYMNTS they planned to use BNPL for holiday purchases is nearly double the 1.6% who used the option during the 2020 holiday season.

BNPL may be making a significant mark on the retail world and how consumers prefer to spend, yet credit cards have remained the most popular way for consumers to make purchases beyond their immediate means. Seventy-five percent of consumers plan to pay for gifts with their credit cards, including 15% who plan to use credit cards for all of their gift purchases.

BNPL may be making a significant mark on the retail world and how consumers prefer to spend, yet credit cards have remained the most popular way for consumers to make purchases beyond their immediate means. Seventy-five percent of consumers plan to pay for gifts with their credit cards, including 15% who plan to use credit cards for all of their gift purchases.

Just 54% of consumers went the credit card route in 2020 and paid off the added debt in 2.2 months, on average, while 28% paid off the added debt by the next statement period. However, 29% of consumers who paid for holiday gifts with credit cards in 2020 still had that added debt heading into the 2021 holiday season.

BNPL is becoming a more mainstream payment option, and 42% of consumers planned to use BNPL for some portion of their 2021 holiday spending. Merchants that offer BNPL options could see customers that are more willing to spend: If BNPL options were available, 32% of consumers would spend up to $99 more and 26% would spend up to $200 more. Forty-six percent of consumers said that they would have to spend less this holiday season if they could not access BNPL, indicating how such options make a significant difference in consumers’ willingness to spend.

BNPL also appears to have replaced layaway as an installment payment preference among consumers, 75% of whom said they see no reason for layaway services if BNPL is available. The change from layaway to BNPL shifts consumers from paying ahead for something they receive in the future to paying in the future for something they receive immediately.

Major retailers, such as Amazon and Walmart, have pushed their BNPL options — and Affirm, which provides BNPL services for both companies, has an estimated 12,000 merchants with which it works. Much like the layaway option it replaces, consumers perceive BNPL as lower risk than traditional credit methods. The option is also attractive to younger consumers who may not be able to secure much traditional credit. BNPL’s availability is also a selling point for some consumers, with 31% of bridge millennials reporting that they would be more interested in shopping at physical stores that have BNPL options.

Managing BNPL Accounts and Payments

One of the biggest challenges BNPL users identified is the ability to track all their different pay ments with various providers: 58% of consumers were uncertain how much they owed, while 46% found it difficult to keep track of their BNPL accounts. Even millennials, who are among the younger consumers who favor BNPL options, face these struggles.

ments with various providers: 58% of consumers were uncertain how much they owed, while 46% found it difficult to keep track of their BNPL accounts. Even millennials, who are among the younger consumers who favor BNPL options, face these struggles.

Seventy-eight percent of millennials could not readily estimate how much they owed without checking each of their accounts. One solution to this issue could be an app or website that helps users track their BNPL accounts and payments under one interface. Eighty percent of consumers would welcome such a service, and 82% would also like to make payments to all of their BNPL accounts via this type of solution. Keeping track of BNPL payments and paying in a timely manner is every bit as important as avoiding carrying a balance on a credit card.

BNPL’s growth could mean greater profits for businesses over the holiday season, as it allows consumers who could not otherwise access credit to make larger purchases. BNPL may also provide those consumers with a more manageable credit option through scheduled payments. Spending during the 2021 holiday season will also be affected by unique factors related to the 2020 economic downturn, as well as by pandemic restrictions that kept individuals away from their loved ones last year. As a result, it may be difficult to predict how much insight the trends of the 2021 holiday season give into consumers’ future BNPL use.