Buy now, pay later (BNPL) continues to gain popularity across all age groups, and U.S. consumer use in 2021 was up 81% from 2020. Most of that growth came from younger age groups, however. Millennials made up 40% of BNPL users in 2020, the largest share of users by age group. Generation Z consumers are expected to catch up to millennials in time and are already adopting BNPL at a higher rate than millennials. While millennials will continue to make up the most significant portion of total BNPL users, 44% of all Gen Z consumers are expected to use BNPL services at least once by the end of 2022, compared to 37% of millennials.

Millennial and Gen Z consumers both report strong awareness of major BNPL providers, and BNPL is likely to gain a significant position in their wallets as it becomes a common payment method. Across all generations, 56% of consumers already prefer BNPL to credit cards due to the ease of set payments, the simple approval process and lack of interest charges.

This month, PYMNTS examines why BNPL appeals to Gen Z and millennial consumers, as well as how merchants and providers can ensure they attract the fastest-growing BNPL user demographics.

Money Management Across Generations

The portion of consumers living paycheck to paycheck in a recent PYMNTS study peaked in December 2020 at 65%, fell to 54% by May 2021 and, in a sharp uptick, rose again to 61% by December 2021.

The portion of consumers living paycheck to paycheck in a recent PYMNTS study peaked in December 2020 at 65%, fell to 54% by May 2021 and, in a sharp uptick, rose again to 61% by December 2021.

While 77% of those annually earning less than $50,000 reported living paycheck to paycheck at the end of 2021, greater income levels were no guarantee of being able to set money aside. Among those making between $50,000 and $100,000, 66% reported that they were living paycheck to paycheck, along with 42% of those earning more than $100,000. Additionally, 22% of those who said they live paycheck to paycheck said they struggle to pay their bills each month.

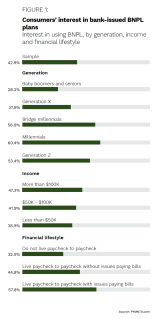

Generational demographics appear to play a role. Of all age groups, bridge millennials and millennials reported struggling the most to live within their incomes, with 70% of those age groups reporting that they were living paycheck to paycheck in May and December 2021. Gen Z consumers reported a sharp increase in living paycheck to paycheck, from 55% in May to 65% in December. Complicating matters, Gen Z consumers also reported the lowest average savings at $1,158.

Among consumers who live paycheck to paycheck, another PYMNTS survey found that 58% of those who struggle to pay their bills have a strong interest in BNPL products provided by their banks, as do 45% of those who do not have problems paying their bills. That compares to 32% of those who do not live paycheck to paycheck.

Fifty-four percent of Gen Z consumers, 57% of bridge millennials and 60% of millennials said they would be interested in BNPL from their banks.

The Importance of Having Options

Payment preferences also play a role in how millennial and Gen Z consumers engage with BNPL. Fifty-one percent of millennial consumers in a recent survey said the availability of payment options such as BNPL influences where they shop, a portion 14 percentage points higher than the multigenerational average. In addition, 54% of all mobile wallet users said they prefer to shop with merchants who offer BNPL, compared to 26% of nonusers. While 42% of all consumers have used mobile wallets, that portion rises to 53% among millennials and 62% among Gen Z consumers.

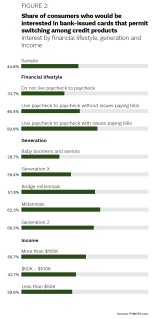

Sixty-two percent of millennials also said they would prefer a bank-issued card that enabled them to switch seamlessly among preferred payment methods. Bridge millennial and Gen Z consumers share that preference, with more than half of consumers from those age groups expressing interest in cards that would give them added flexibility in choice of payment method.

Reaching a Growing User Base

Budgeting and value have become increasingly important for U.S. consumers in the past year. Shoppers know they have options and expect businesses to meet them with tailored payments and products such as BNPL. Forty-five percent of BNPL consumers use BNPL to make purchases that would not otherwise fit into their monthly budgets, while 37% want to avoid paying credit card interest. BNPL installment plans help users bridge gaps between paychecks without running up credit card debt.

Some BNPL providers are also exploring such added incentives as high-yield savings accounts and rewards programs to further cement their relationships with BNPL users. By ensuring that millennial and Gen Z consumers have access to BNPL options that fit their shopping and payment preferences, merchants and providers can secure a place of prominence with these consumers.