Five years from now, buy now, pay later (BNPL) providers may look a lot more like “tech-enabled” digital banks as companies in the space evolve and expand their financial services offerings, according to Sezzle CEO Charlie Youakim.

“At Sezzle, our mission is to financially empower the next generation, and getting deeper into financial services makes a lot of sense for us,” Youakim told PYMNTS’ Karen Webster in an interview. “We’re seeing a customer who loves our product, and if they love us and trust us, what else can we offer them?”

Commerce will always be a key component of how Sezzle and other BNPL providers help merchants with sales and promotions, but companies are also looking at what consumers need. Many are just starting their customer journeys with financial services, “and we see that they need some help in that path,” he said.

“If we can walk them down that path and give them great products, that’s our priority,” Youakim added. “And if we do that, we find that our retail partners love it because we’re helping their customers.”

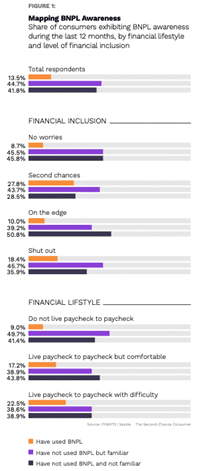

According to PYMNTS research, conducted in collaboration with Sezzle, 14% of online shoppers — more than 28 million U.S. adults — paid for purchases on the internet with BNPL at least once over the last 12 months. Nearly 28% of consumers who have used BNPL may have needed a “second chance” to build their credit scores, while 18% were shut out from other credit options.

Additionally, 47% of consumers who had heard of BNPL programs would be interested in using them to pay for expensive, one-time retail purchases, and 29% would use the payment method to pay for medical bills.

See more: Offering BNPL Is Key to Unlocking Retail Spend for One-Quarter of US Consumers

“Buy now, pay later players will continue to evolve,” Youakim said. “That’s built into our genes — we’re used to evolving and adapting.”

Rewarding Customers

As the BNPL space matures, he said, it will probably become more common for merchants to partner with providers to offer store credit cards that feature the same types of rewards and installment plans people look for with BNPL.

But he said that Sezzle doesn’t currently see a lot of crossover between its customers and those who are interested in-store cards, although providers that offer longer-term installment plans might. (Sezzle offers customers interest-free installment payments for six weeks, a niche that generally appeals to customers who aren’t getting approved for a store card — or aren’t trying to.)

“Our viewpoint is that at some later stage, the customer might be interested in that, and we can help them walk that path in partnership with our retail partner,” Youakim said.

Currently, the “core reward” consumers get from using Sezzle’s BNPL product is the fact that payments are interest-free. But the company has started to build out other reward systems — for instance, its Sezzle Spend program, which allows it to issue credit to an account through a promotion.

“Just like store cards are evolving, I think the buy now, pay later space will evolve over time and probably grab onto rewards in more depth,” Youakim predicted.

Providing Simplicity

As BNPL providers continue to work with retail partners, Youakim said he expects that companies will “pull in some pieces of more traditional store cards” that work for them to incorporate private-label credit cards into customers’ digital wallets, where they have typically been left out.

“I have about 15 cards,” Youakim said. “I don’t think the future is that. I think the future is really … just a phone, and it’s all-digital lines.”

PYMNTS research has found that consumers are increasingly looking for a more streamlined ecosystem in the connected economy because they want to manage their time and spending more efficiently and responsibly. Keeping track of all the promotions, discounts, passwords and registrations that saving time and money requires can be a difficult task, to say the least.

“The customer is always craving simplicity and ease of use,” Youakim said. “The more you can focus on that in your offerings, the more you’re going to drive engagement with that customer.”