Consumers face tricky decisions when they want or need items that they cannot easily afford to pay for at once. Shoppers in the United States have long turned to credit cards to let them get the products now while delaying payments until they have a chance to save up. However, this approach does not work well for everyone, and the pandemic may cause some households to become especially leery of the interest fees they will face if they are late paying their card bills.

Consumer awareness of buy now, pay later (BNPL) options is increasingly rising as an alternative option. These plans fund retail purchases that consumers can then pay off over time in typically four installments. Customers who meet each payment deadline can avoid fees, and some find that the late fee structures used by these flexible payment plans better suit their tastes than those used by credit card companies. Consumers who do not qualify for credit cards or become reluctant to use those tools may see BNPL plans as a  convenient alternative method for deferring payments.

convenient alternative method for deferring payments.

The January “Buy Now, Pay Later Tracker®” explores how consumers across the financial spectrum have been leveraging BNPL options during the pandemic and how and when both high-income shoppers and those living paycheck to paycheck choose to deploy the tool.

Around The Buy Now, Pay Later Space

BNPL options are drawing interest from consumers in various income brackets and seemed especially popular among top earners during the Black Friday shopping holiday. Recent PYMNTS data found that twice as many consumers earning more than $100,000 used BNPL that day compared to those making below $50,000 or between $50,000 and $100,000. Consumers frequently used BNPL to buy clothing, with that merchandise category claiming 71 percent of transactions made with the financing tool.

Interest in BNPL is not limited to the U.S. either. A United Arab Emirates-based FinTech recently took in $23 million in Series A funding to power its delivery of such services. The FinTech, tabby, intends to use the funds to improve its lending and engineering capabilities and scale its product, which currently helps consumers in the UAE and Saudi Arabia pay off purchases made with domestic and global merchants’ operations in the countries.

Buy now, pay later options have developed differently across nations, with trends in C hina seeing retailers often providing their own installment payment plans rather than offering third-party plans at checkout. These retailers’ installment payment offerings appear to be drawing particular interest from younger consumers who might not qualify for much credit from banks. Eighty percent of Ant Financial’s Huabei credit offering users are from the Generation Z or millennial demographics, for example, according to recent reports.

hina seeing retailers often providing their own installment payment plans rather than offering third-party plans at checkout. These retailers’ installment payment offerings appear to be drawing particular interest from younger consumers who might not qualify for much credit from banks. Eighty percent of Ant Financial’s Huabei credit offering users are from the Generation Z or millennial demographics, for example, according to recent reports.

Find more on these and the rest of the latest headlines in the Tracker.

How BNPL Plans Help Shoppers Defer Payments With Predictable Fees

Consumers who see long-desired clothing items come back in stock in their sizes may want to snap them up right away — but not everyone has room in their weekly budgets to comfortably pay for such purchases. Some shoppers are also concerned that using credit cards to pay could end up costing them later if they cannot stay on top of the bills and become penalized with interest charged on overdue payments.

Retailers need to help reach these shoppers, too, and including BNPL as an additional payment option could help merchants make the sale, says Stacey Blicker, vice president of digital for fashion retailer Chico’s FAS. Some consumers may find the late fees charged by BNPL plans to be more predictable and easier to plan around, making them interested in this option. In this month’s Feature Story, Blicker explains the importance of adding BNPL to merchants’ mix of checkout options.

Retailers need to help reach these shoppers, too, and including BNPL as an additional payment option could help merchants make the sale, says Stacey Blicker, vice president of digital for fashion retailer Chico’s FAS. Some consumers may find the late fees charged by BNPL plans to be more predictable and easier to plan around, making them interested in this option. In this month’s Feature Story, Blicker explains the importance of adding BNPL to merchants’ mix of checkout options.

Read the full story in the Tracker.

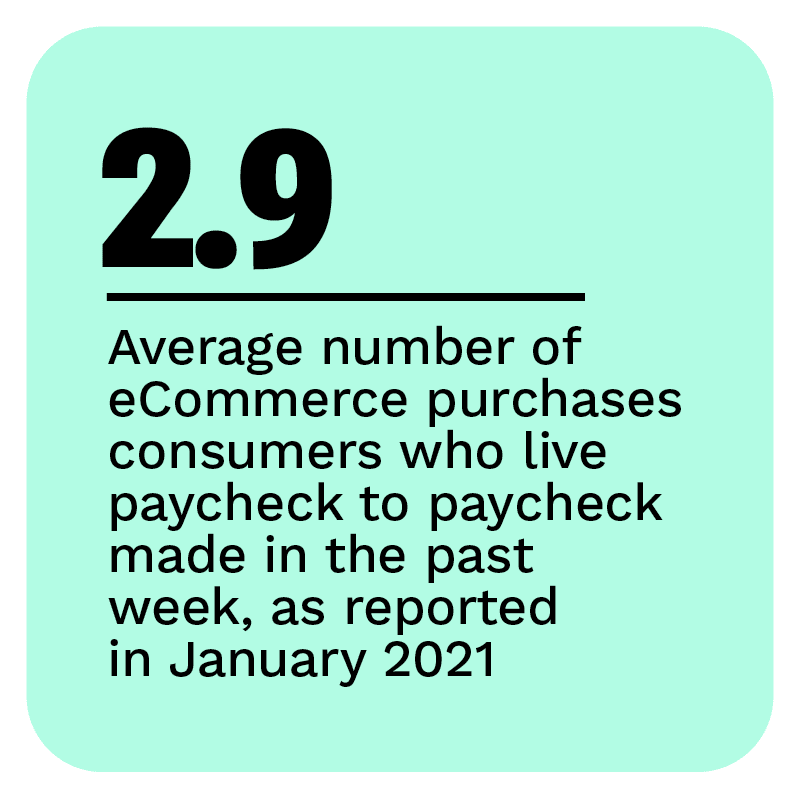

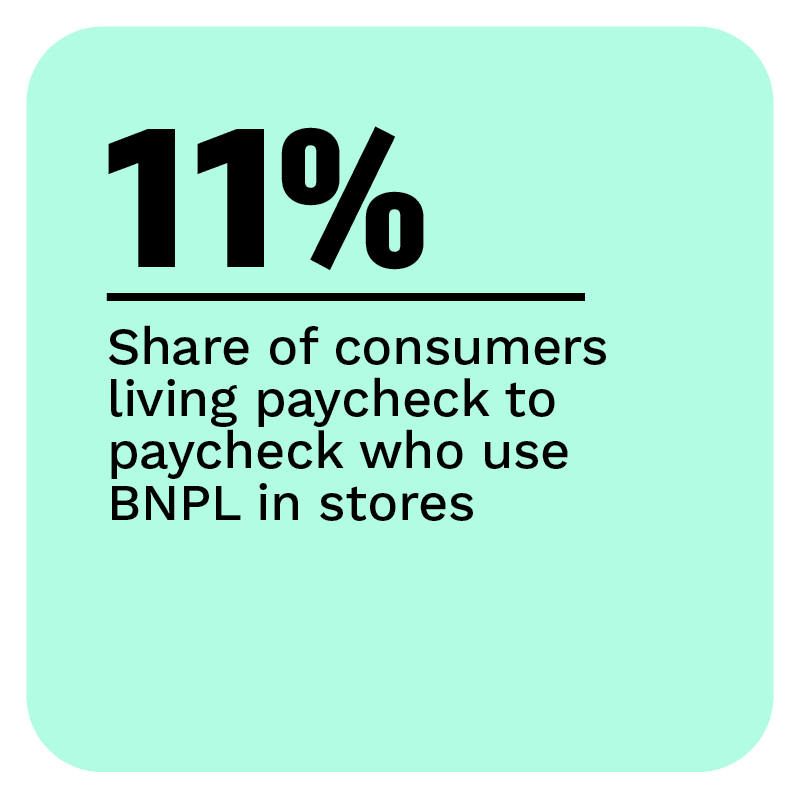

Deep Dive: How Consumers Across The Income Spectrum View Payments In 2021

Many households have seen their finances overturned during the course of the ongoing pandemic. This could compel them to reconsider the tools they use when making purchases. This month’s Deep Dive examines how consumers living paycheck to paycheck and those with more financial stability consider the payment tools they use at in-store and online checkouts. The findings detail when and how financially secure households, as well as financially unstable ones, select BNPL, credit cards, debit cards, mobile wallets or other options.

Learn more in the Tracker.

About The Tracker®

The “Buy Now, Pay Later Tracker®,” a PYMNTS and Afterpay collaboration, brings you the latest news and research from the buy now, pay later space. It features new data about how and when consumers across the financial spectrum turn to BNPL and why some fashion retailers adopt the payment option.