Are installment payments evolutionary or revolutionary? They are both, with an emphasis on the latter, as consumers worldwide join the alternative-credit resistance in record numbers.

The July 2021 Buy Now, Pay Later: The Financial Self-Care Revolution Report, a PYMNTS collaboration with Sezzle, is packed with facts on this rising payments powerhouse, as discovered in a survey of more than 7,000 adult consumers.

Among other eye-openers, PYMNTS researchers found that buy now, pay later (BNPL) adoption “may introduce merchants to previously inaccessible audiences while improving their in-store revenue prospects: BNPL users tend to make more in-store purchases than consumers paying with other methods. We also examine the potential positive effects of BNPL access on consumer financial health and their access to the full range of retail and online shopping experiences.”

Our research reveals the emergence of three distinct BNPL personas: the “worry-free” consumer who is financially stable with a good credit score; the “second-chance” consumer who is financially sound yet with credit histories and scores that impede access to traditional credit; and “shut-out” consumers, 57 percent of whom earn less than $50,000 per year, struggle to pay monthly bills and are using BNPL as the only credit option available to them.

It’s a fascinating microcosm of the larger credit landscape, although there’s nothing “micro” about the appeal of point-of-sale credit, from well-off shoppers to those in financially difficulty.

BNPL As Gateway To Financial Inclusivity

Of the many faces of BNPL, perhaps the most compelling is how consumers of all income levels are using POS credit to manage their spending while getting items they need or want.

Researchers found that “BNPL can be a gateway to both better economic health for all types of consumers and improved financial inclusivity for those with damaged credit. Our data shows that 33 percent of shut-out consumers reported that they would use an improved credit score to purchase necessities. This share is three times greater than the share of worry-free consumers who said the same (11 percent). We also learned that 34 percent and 30 percent of shut-out consumers would use their improved credit scores to buy homes and cars, respectively. This figure is more than twice the corresponding figures for consumers with no financial worries (13 percent and 14 percent, respectively).”

A revealing finding is how many BNPL users see it as a way access traditional unsecured credit lines. According to the Buy Now, Pay Later: The Financial Self-Care Revolution Report, 51 percent of consumers who used or said that they would use it “believe that BNPL products will allow them to improve their credit scores. This rate is higher for financially underserved consumers (57 percent and 69 percent of second-chance and shut-out consumers, respectively).” That moves to 77 percent of shut-out consumers and 70 percent of second-chance consumers seeing BNPL “as an option that improves their ability to buy things that they want without overspending.” Additionally, 46 percent said that BNPL offerings “made it possible for them to make purchases they could not have otherwise afforded.”

An Untapped Market Beckons

Between the headlines it’s been generating and the understandable consumer buzz around BNPL brands (and the concept itself), researchers found that there’s room to grow for alt-credit, as millions have yet to sample its ability to obtain items and pay them off incrementally.

As the study states, “Around 29 million U.S. adults have used BNPL for online shopping at least one time during the last 12 months, and 7.6 million who have not used BNPL already are interested in using it in the future. PYMNTS’ research found that 47 percent of respondents who are familiar with BNPL programs would be interested in using them to pay for expensive, one-time retail purchases. Twenty-nine percent would use BNPL to pay for medical bills.”

The figures signal a broad and deep future for BNPL, and its utility beyond the apparel and accessories that popularized the concept in the early going.

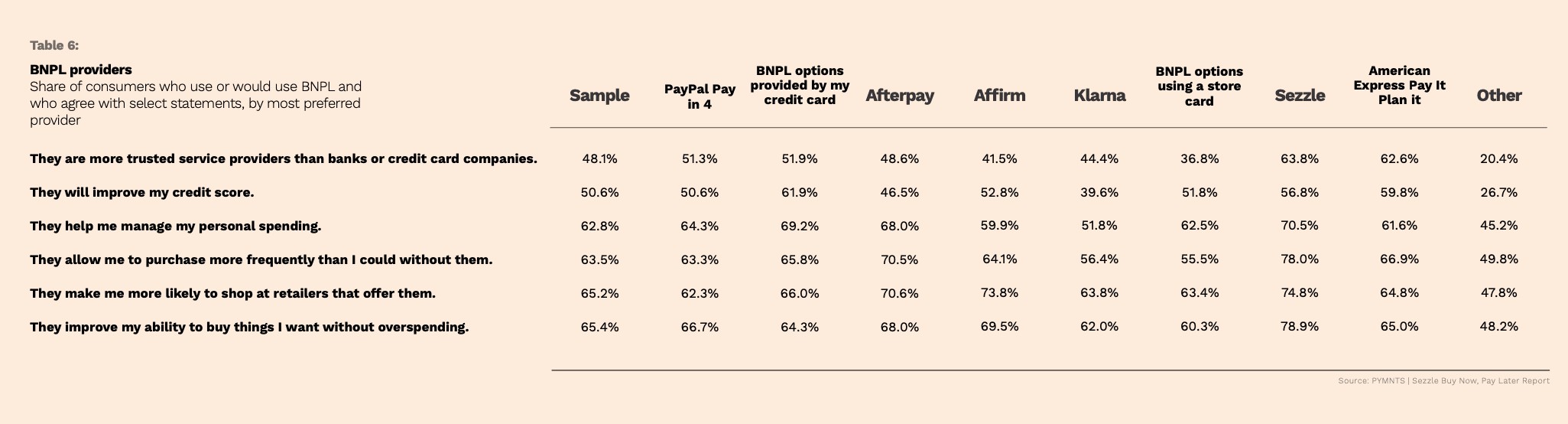

Additionally, the report notes that “65 percent of consumers who use or would use BNPL see it as a tool to purchase items without overspending and state that they are encouraged to shop at retailers that offer these programs.” Here again, the opportunity for merchants is clear.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More