So PYMNTS, in conjunction with BNPL firm Afterpay, surveyed them for an upcoming report on the segment — talking to 304 business owners, founders or solo practitioners who spend at least 25 percent of their time working at their firms and have physical locations at which customers can purchase products and services. These respondents earned less than $10 million in 2020 and belonged to select industry segments.

What we saw is BNPL is rapidly, but unevenly infiltrating the small and medium-sized business (SMB) segment. A firm’s age, geographic location and vertical make a major difference as to whether a given SMB has embraced offering BNPL options as of yet.

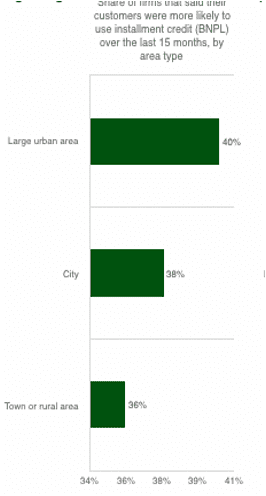

1. Urban SMBs Are More Likely To Embrace BNPL Options

The bigger the city the more likely the SMB is to have embraced offering BNPL options for their consumers. That is the take-away from PYMNTS preview data. Firms that are established in large urban areas — those with at least 1 million inhabitants — experienced the greatest demand for installment credit over the last 15 months (40 percent), dramatically leading both SMBS located in smaller urban areas of less than 1 million inhabitants and those established in towns or rural areas.

Thirty-eight percent of merchants working in smaller cities and 36 percent in rural areas and towns also reported making BNPL offers, however, meaning in any geography BNPL’s penetration among SMBs has cleared the one-third mark in terms of SMB acceptance.

2. The $250K-$2.5M Revenue Sweet Spot

How much revenue a firm brings in per year, according to the upcoming data release, also makes a notable difference in how much BNPL business they tend to do annually. The sweet spot for BNPL offerings seems to be single SMBs bringing in between $250,000 and $2.5 million a year in revenue, who report some 39 percent of their consumers use BNPL options to pay.

Those figures drop off some outside of that range, according to the data. Firms that make less than $250,000 a year report about 35 percent of their customer base uses BNPL options while firms with revenue above $2.5 million reported 36 percent use among their consumers.

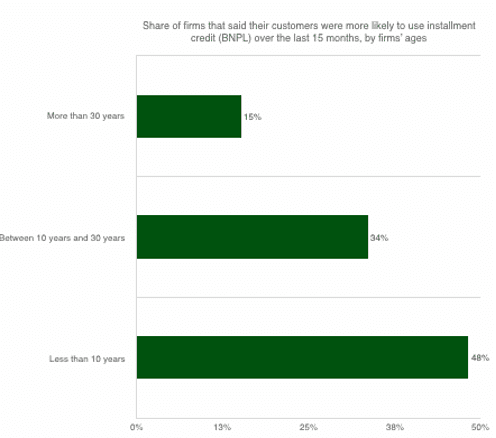

3. Younger Firms Lead BNPL Adoption

When looking at factors that affect BNPL adoption, more than geography or annual revenue, age of the firm makes the most definitive difference as to whether or not they are leveraging BNPL, with firms younger than 10 years far and away leading the field.

Firms under a decade old report high use of BNPL service among 48 percent of their customers. That compares with older firms (more than 30 years old) with the lowest use rate among their customer base of 15 percent. Sliding between them are middle aged firms — between 10 and 30 years old — which report a BNPL use rate among their customers of 34 percent.

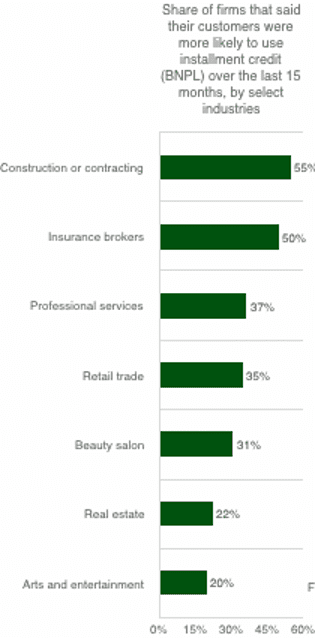

4. Construction’s BNPL Growth Spurt

Demand for BNPL is on the rise, and the data show, across a wider range of verticals. More than half (55 percent) of construction or contracting firms are seeing an increase in demand for installment credit, according to the data.

Construction is followed closely by insurance, where half of firms have reported an increase in demand for BNPL offerings; professional services, where 37 percent report the demand increases; and retail trade businesses, where 35 percent report an uptick in demand.

5. Gaining Ground In Retail Sales

BNPL is also showing up in a wider range of retail contexts, and seeing soaring usage in several. Some 86 percent of retailers that sell sporting goods, for example, are seeing greater demand for BNPL options.

And while sporting goods are the biggest surge, more than two thirds of retailers that sell health and beauty products, musical instruments or automobiles parts (67 percent in all cases) report seeing greater BNPL use, while 57 percent of those selling clothing and accessories report an uptick.