Retailers that offer a variety of credit options draw in consumers battling the constraints of higher prices and stagnant wages to help them smooth things over.

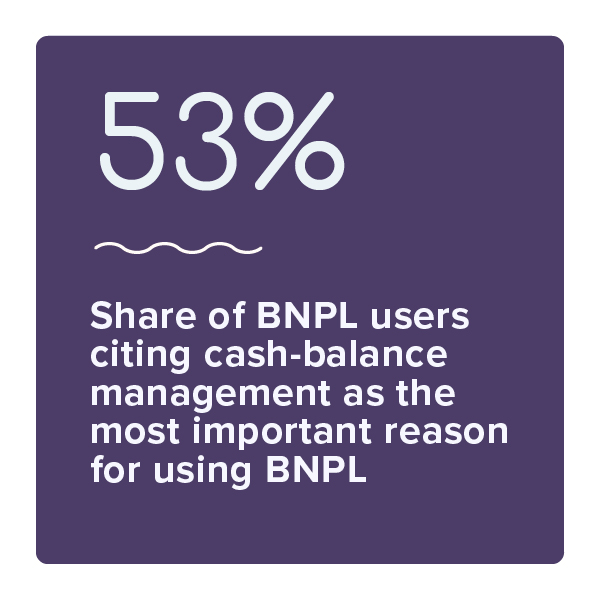

Prior PYMNTS’ research established improved spend management as a top reason for younger consumers to use credit products. Our most recent survey on buy now, pay later seconds this. Preserving cash and lines of credit was the primary reason 53% of BNPL users chose that payment method.

Prior PYMNTS’ research established improved spend management as a top reason for younger consumers to use credit products. Our most recent survey on buy now, pay later seconds this. Preserving cash and lines of credit was the primary reason 53% of BNPL users chose that payment method.

The BNPL aspect that enables consumers to conserve cash is that it functions as a low- or no-interest installment loan. Consumers’ willingness to pay in installments and keep cash on hand can also affect whether they complete purchases, which is an important actionable takeaway for retailers.

This detail is one of the key findings in “The Credit Accessibility Series: BNPL’s Wide-Ranging Impact on Consumers and Merchants,” a PYMNTS and Sezzle collaboration. This report is based on a survey of 3,177 U.S. consumers conducted from April 26 to May 2 and assesses the rising popularity of this payment method as a credit option, examines consumers’ reasons for using it and explores the potential to improve consumer credit profiles.

More key findings from the study include the following:

Merchants that do not offer BNPL could lose potential sales. Those that do offer BNPL may help boost customer spending on larger-ticket items.

Offering these plans can potentially head off cart abandonment at the pass. Four in 10 users said they were extremely likely to delay or cancel a purchase or opt for a cheaper product if a retailer or merchant did not offer BNPL. For example, 26% of baby boomers and seniors said they would cancel a purchase if they could not use the method to pay.

An inflationary environment may motivate increased usage.

Preserving a cash cushion and avoiding interest are consumers’ main motivations behind BNPL use — motivations popular in a time of inflation. BNPL allows consumers to pay for large-ticket items in installments with no additional interest charges. For 28% of consumers, the low- to no-interest rate is an important factor; for 11%, it is the most important reason to use it. For millennials, the availability of this. method can actually prevent them from using high-interest loans.

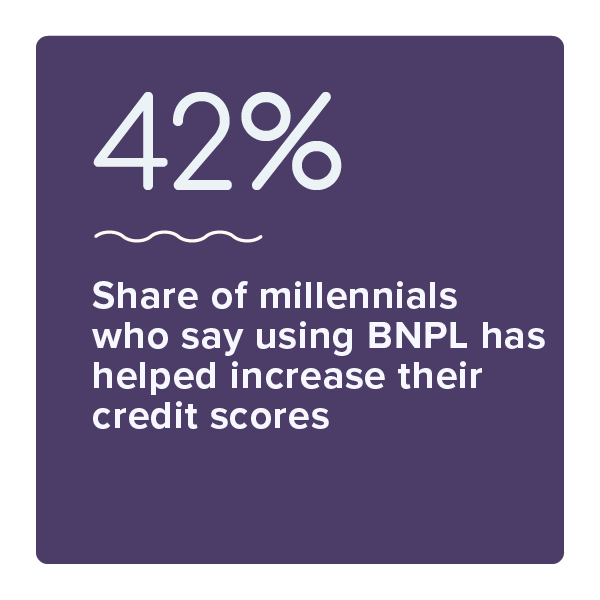

Consumers say that using this payment method has helped increase their credit scores.

One-third of BNPL users say that using the payment method has increased their credit scores, while 17% said improving their credit scores was the reason for applying for it. Various factors may be at play here, including that these plans do not affect a consumer’s credit score or that the plans allow consumers to better manage their cash flows and reduce the number of late payments. Millennials, at 42%, seem to be most aware of BNPL’s potential to boost credit their scores.

Download the report to learn more about how BNPL impacts consumer buying behavior.