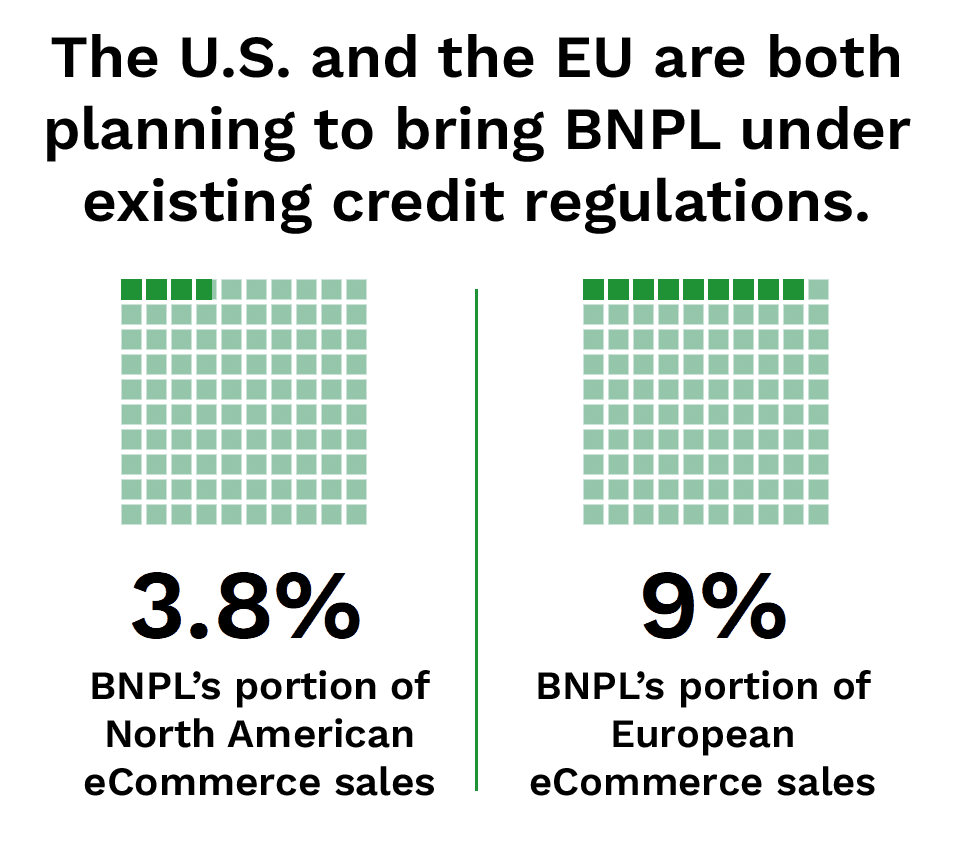

This laissez-faire environment could quickly be drawing to a close, however, as governments across the globe consider regulations that would apply many of their existing credit laws to the BNPL market. This month, PYMNTS explores pending regulations in the United States and the European Union and how these regulations could affect BNPL providers.

This laissez-faire environment could quickly be drawing to a close, however, as governments across the globe consider regulations that would apply many of their existing credit laws to the BNPL market. This month, PYMNTS explores pending regulations in the United States and the European Union and how these regulations could affect BNPL providers.

US and EU Regulations Under Consideration

The U.S. BNPL regulation is being spearheaded by the Consumer Financial Protection Bureau (CFPB), which recently unveiled a study detailing the potential risks of BNPL. The report highlighted risks to consumers that include the potential not just for debt accumulation and overextension but also for having their data harvested without their knowledge by BNPL providers.

While BNPL regulation is generally absent in the U.S., experts predict that the CFPB will unveil proposed rules sometime in the near future. The exact regulations are unknown, but they may bring BNPL under the same umbrella as traditional credit companies and will curtail the amount of data that providers may harvest and leverage from their customers.

The EU’s BNPL regulatory framework is much further along. Like the U.S., the EU plans to bring BNPL under the existing credit umbrella — in this case, the Consumer Credit Directive. The European Commission approved a revision to the directive in 2021 that would extend it to BNPL, including new protections geared toward a mobile-first market. Among these would be banning pre-ticked contract agreement boxes and requiring all contracts to be presented in a mobile-friendly format so that users more concretely understand the terms before agreeing to credit.  The European Council announced it had decided on final regulatory language in late 2022, but the full regulation is still forthcoming.

The European Council announced it had decided on final regulatory language in late 2022, but the full regulation is still forthcoming.

Potential Massive Impact of BNPL Regulation

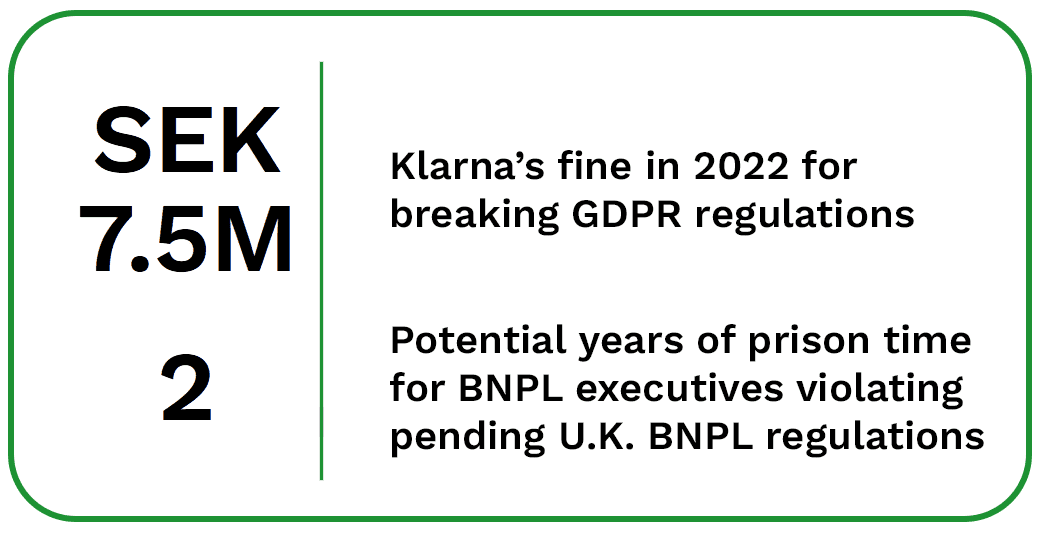

The U.K. will soon have the power to ban BNPL providers from doing business altogether if they fall under the jurisdiction of the Financial Conduct Authority once pending legislation passes. BNPL providers will need to ensure that their affordability checks are up to code, as well as the information provided to prospective customers about their loans, if they wish to avoid fines, imprisonment or both.

In other European countries, BNPL providers are already being punished when they break regulatory rules. Sweden, for example, fined BNPL provider Klarna 7.5 million Swedish krona (about $723,000) when it found the company in violation of GDPR’s personal data protection clause.

Regulations Will Have Unequal Impact on BNPL Providers

BNPL providers that leverage customers’ own credit cards to make purchases rather than using independent apps already fall under many of the same credit regulations as normal payment cards. These organizations will thus likely see little change under the new rules. Other BNPL providers will need to comply proactively with the anticipated regulations if they wish to avoid difficulties such as Klarna’s.