Sure, among many consumers (including younger people), dollar bills, C-notes and the like stand almost as relics — to these consumers, cash is a retro payment tool at best, and a dirty, logistically costly waste of paper and ink at worst. (Don’t even get us started on coins, all those pieces of metal just taking up space.) Cash is easily stolen, lost, laundered, hidden from the tax man, and rendered unhip by P2P and other rising mobile payment methods.

However, even as the use of cash declines, there is mounting evidence that it’s not going anywhere, whether it be the ongoing political backlash to the concept of a cashless retail economy or merely the realization among many consumers that using cash instead of credit cards is a better way to keep from sinking into debt.

So, in the spirt of “if you can’t beat ‘em, join ‘em,” PYMNTS recently caught up with two entrepreneurs determined to bring digital expertise and efficiency to cash management — the type of cash management that can make or break employees and some business operators, especially in the restaurant space.

Better Cash Management?

In a discussion with Karen Webster, Co-CEOs Brian Hassan and Justin Roberts of Kickfin — a company that is trying to outdo armored car services and bring more digital sense to cash management — spoke about the cash landscape, and why players in the quick-service restaurant (QSR) and full-service restaurant spaces need more options when it comes to cash. The general idea behind Kickfin is to provide businesses with hardware and digital technology that can eliminate the need for night deposits and tipping out in cash in favor of daily disbursements to payment cards, as the cash powering those payments essentially sits in storage.

“The most progressive brands in the market have gone cashless,” Hassan said, thanks in large part to the relatively high labor and financial costs of handling, depositing and processing bills and coins. Still, wishing for a cashless world doesn’t make it so.

He explained that, for instance, of the immigrant population in Los Angeles (one of the most diverse and economically powerful cities on the planet), some 8.6 percent of consumers are unbanked, which pretty much forces them into a cash-centric lifestyle. Woe to any retailer or service provider that turns its back to such a potential consumer base — or pool of labor.

The interview comes at a busy, perhaps significant, time for the concept of cash and cashless retail. Seemingly important patterns and precedents are being set.

Cash Versus Cashless

Earlier this month, news emerged that the Mercedes-Benz Stadium in Atlanta has gone cashless. Only credit cards, debit cards and mobile payments will be accepted at the venue — though, in a nod to those customers without bank accounts, the stadium will have roughly 10 machines that will let users exchange cash (ranging from $10 to $1,000) for a prepaid Visa debit card.

Meanwhile, local politicians (and some national ones) are pushing back against the slow, but steady, spread of cashless-only-transaction policies by certain businesses. Earlier in the month, Philadelphia — home of the first U.S. Mint building — became the first major U.S. city to ban cashless stores. Such stores have taken on an almost-utopian tint, and are a prime source of innovation from the likes of Amazon, with its cashless “Go” stores linking to Amazon accounts through mobile devices and automatically charging for purchases.

Kickfin Play

That’s the context in which Kickfin is operating.

“How do we solve the problems associated with cash?” Hassan asked Webster. “How do we address cashless in a way that does not enable [more] friction?”

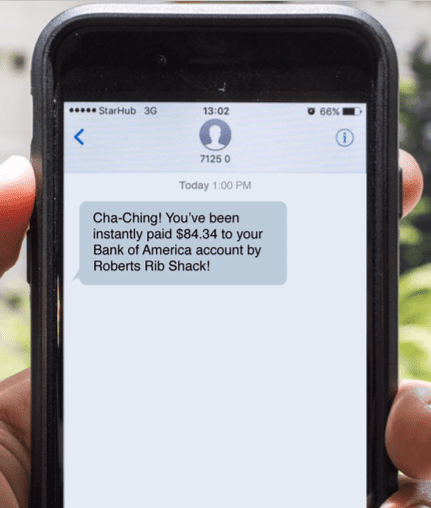

According to Kickfin, here’s how: Cash moves from the customer to the business, then is deposited by that business into what Kickfin calls a “smart cash recycler.” That device is similar to what an armored car operation markets as a “smart safe.” Data about the cash deposited into the recycler goes to Kickfin, which, in sync with its banking partner, credits the merchant for that deposit, using ACH for next-day disbursement. The cash can also be sent to workers who have earned tips, and deposit to their debit cards, with access to those funds in real time.

Among the differences between Kickfin and the armored car operations, Kickfin customers don’t have to go to banks to set up any deposit or disbursement operations, but can work through Kickfin’s banking partners. In addition, according to Hassan, the Kickfin system saves workers money, as they don’t have to pay fees to use the prepaid cards onto which tips are digitally deposited. The money goes onto those workers’ own payment cards, saving them per-transaction fees on mandated prepaid cards that can run up to $5 for just $40 worth of redemption, he said.

Night Deposits

The specific problems this can solve, according to Hassan? Sparing night managers the danger and hassle of taking large amounts of cash away from their businesses — think QSRs or full-service restaurants — for night deposits. It makes the disbursement of tips easier, without adding too much time to the process. After all, so many service industry workers live paycheck to paycheck, and adding to that burden is unlikely to win the employer any extra loyalty among the workforce.

The space Kickfin is targeting, Hassan said, receives 88 percent of its payments via payment cards, with the remaining 12 percent in cash. Cash certainly does not represent a majority of transactions, but even reducing a bit of hassle when it comes to coins and bills can make general business operations more efficient. Once a person moves toward the center of the country, away from the coasts (the location of most cashless retail experiments), cash use becomes even more pronounced, he said — adding that 60 percent of transactions under $10 are still conducted in cash.

The great cashless push will continue, and there’s nothing bad about that. Yet, as the politics of cashless and this young service both show, there are still good reasons to bet on the continued survival of cash.