Markets were roiled this past week by concerns over inflation, and over Fed rate hikes, and over consumer demand, especially — and it may have felt that no companies emerged unscathed.

FedEx might be called the harbinger of bad news this past week, and a whole sector — the buy now, pay later space — looks set to be upended by increased regulatory scrutiny.

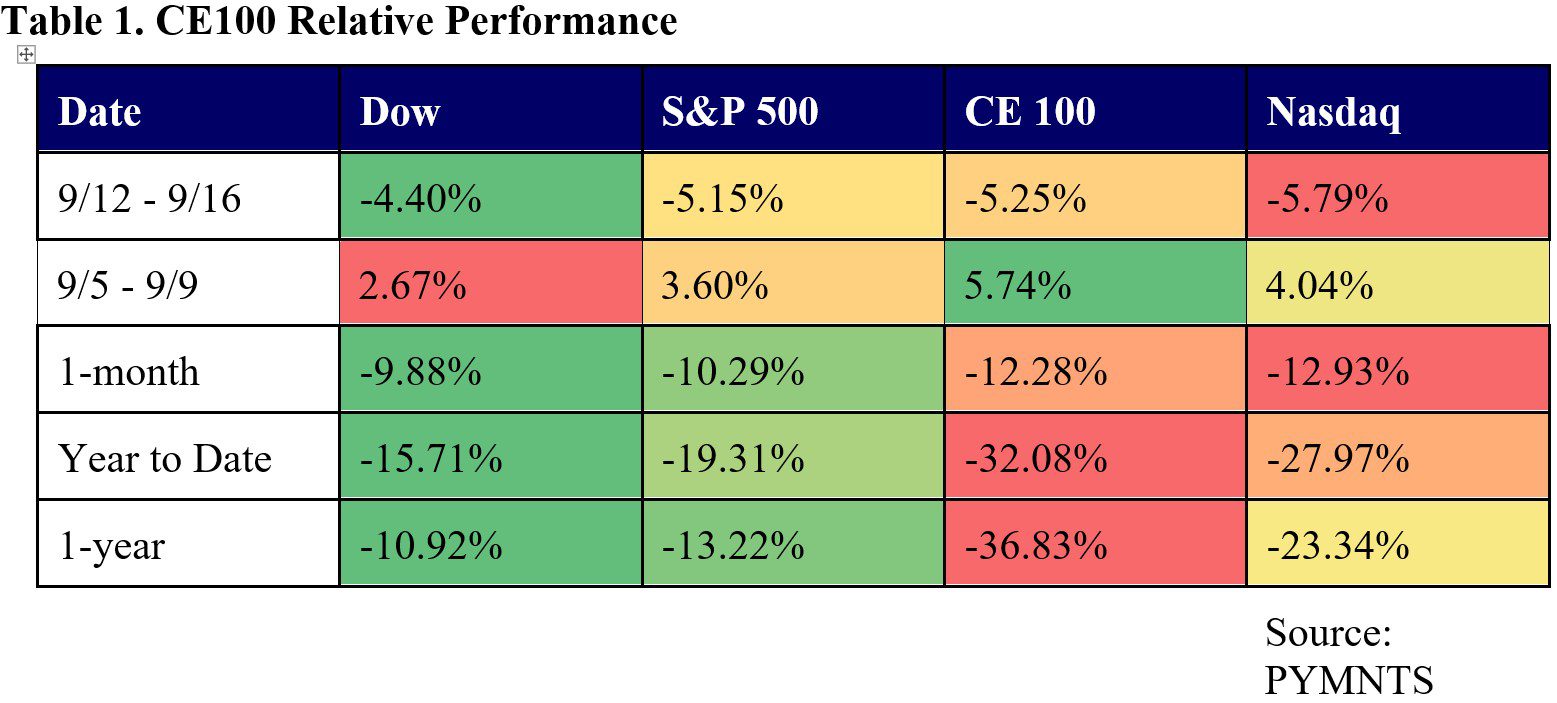

To that end, the PYMNTS ConnectedEconomy™ 100 (CE100™) Index lost 5.3% in the past week, though it did fare a bit better than the tech-heavy Nasdaq, which fell 5.8%.

Each of our 10 pillars lost ground, with the best performers down a relatively muted low-single-digit percentage points. That would include the Live pillar, which gave up 2.4%, and the Have Fun pillar, which slid 4%.

But the Pay and Be Paid, Work, and Move segments were all swamped by heavy losses, sending those groups down a respective 7.9%, 7.4% and 6.1%.

FedEx’s Bleak Picture

FedEx was the standout here, with a 23% loss on the week, spurred by the announcement that the Move giant is effectively idling at least some operations — by closing offices and parking aircraft — as eCommerce slows and package volumes decline.

Read also: FedEx Closes Stores and Grounds Planes as eCommerce Volume Falls

The headwinds are widespread, as a release on Thursday detailed that the company’s Express has seen macroeconomic weakness in Asia and service challenges in Europe, resulting in a $500 million shortfall compared with the company forecast. FedEx Ground saw its revenue around $300 million below the company forecasts.

FedEx’s warnings also have implications for the Pay and be Paid group in particular — a rocky road for eCommerce signals that people are buying less, which means they are transacting less often, which of course implies some real and near-term challenges for payments-specific names. Affirm slipped 15% on the week, Sezzle was down 13.2%, Block lost 12.7%.

In addition to macro concerns, the buy now, pay later players (and their investors) will have to grapple with increased interest on the part of Consumer Financial Protection Bureau on how to regulate the space. The CFPB released a report this week, “Buy Now, Pay Later: Market Trends and Consumer Impacts.” The agency put forth the recommendation that there be new measures put in place to safeguard consumers.

The CFPB warned that the BNPL loans are structured in ways that present “operational hurdles” such as the lack of clear disclosures of loan terms, challenges in filing and resolving disputes, and the mandate that autopay be used for those loan payments. The report also warns, specifically about the risks of consumer “overextention.” The CFPB found that 10.5% of borrowers were charged at least one late fee in 2021, up from 7.9% in 2020.

Muted Gains

A few individual names eked out gains, albeit muted ones as the “best” performing sectors were the Live pillar, down 2.4% and the Have Fun pillar, which lost 4%. In Live, for example, Porch Group was up 4.9%, though no company-specific headlines drove the action over the past five days.

There was at least one theme that emerged among the winners — tied, it seems, to streaming media and to entertainment.

In the Have Fun pillar, DraftKings gained 5.5%. News came this week that DraftKings has signed on as official sponsor of Thursday Night Football (TNF) on Amazon Prime in a multiyear agreement, offering up a big chunk of the 1.5 million average monthly unique payers (MUPs) DraftKings reported in its second quarter 2022.

Per the announcement from those two companies, “As part of the multiyear agreement, TNF will contain DraftKings integrations in the live pregame, including odds and additional sports betting insights. DraftKings and Amazon will also collaborate on TNF-themed offerings, including same-game parlays, which will be available on the DraftKings Sportsbook app.”

Netflix was up 2.8%, driven by reports, as detailed here, that the company’s new ad-supported streaming service could reach around 40 million viewers globally by the third quarter of next year.