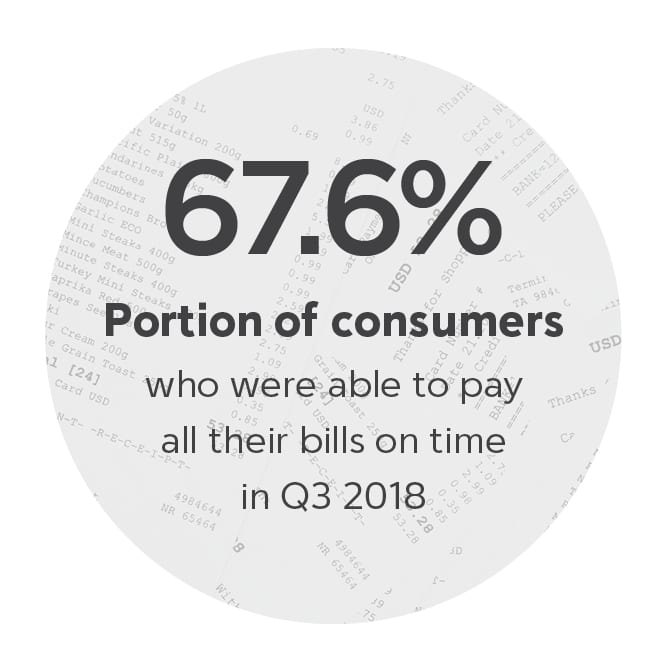

For one thing, the portion of consumers who fell behind on bill payments went way up, increasing from 30.7 percent in Q2 2018 to as much as 41.2 percent in Q3 2018. Meanwhile, the portion who faced delinquency increased by more than a third, with 36.3 percent falling so far behind that they had to be contacted by debt collectors to settle accounts.

For one thing, the portion of consumers who fell behind on bill payments went way up, increasing from 30.7 percent in Q2 2018 to as much as 41.2 percent in Q3 2018. Meanwhile, the portion who faced delinquency increased by more than a third, with 36.3 percent falling so far behind that they had to be contacted by debt collectors to settle accounts.

More concerning still was the fact that, even among consumers who had resolved their outstanding debts and pulled themselves out of delinquency, as much as 22.7 percent said they expected to fall right back in again in as little as a few months’ time.

Yet, on the positive side, they were feeling better about their finances than they had in the past year. So, what’s behind this feel-good factor?

In the Q3 2018 edition of the Financial Invisibles Report™, PYMNTS surveyed more than 2,000 American consumers to get to the bottom of what was driving their financial confidence — even in the face of delinquency.

Consumers, the survey revealed, were feeling more confident in their financial stability because they were using credit cards to pay their bills. The usage of credit cards to pay off debt shot up from 44.6 percent to 61.8 percent in Q3 2018 — and, while this may have helped them keep the heat on in the short term, it was  eating up their credit lines, pushing them closer to delinquency.

eating up their credit lines, pushing them closer to delinquency.

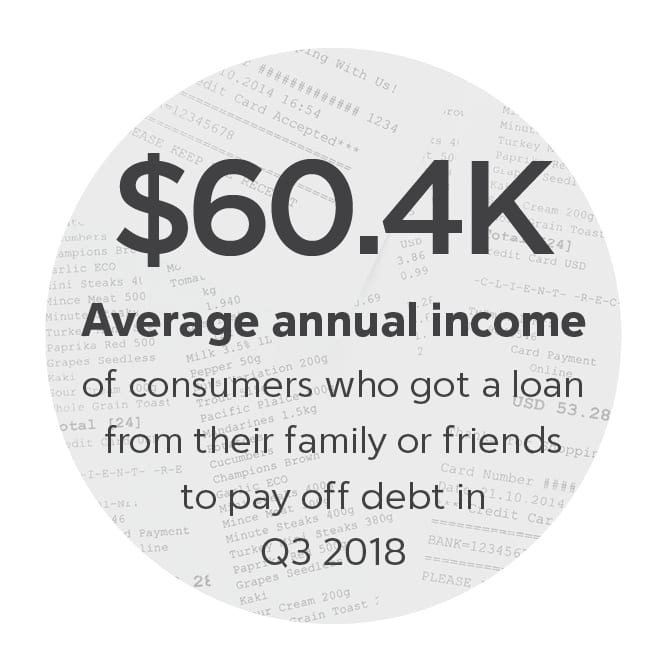

At the same time, the use of alternative products like pawnshop and payday loans went up — even among consumers with high annual incomes. In fact, the average income of consumers who took out pawnshop loans was surprisingly high at $78,600 per year. Meanwhile, the average income of those who took out payday loans was even higher at $80,500 per year.

However, as the research demonstrated, a high income is not always enough to stave off financial delinquency.

To learn more about how consumers tackled bills and debts in Q3 2018, download the report.

When it comes to managing personal finances, consumers are seemingly taking one step forward and three steps back.

When it comes to managing personal finances, consumers are seemingly taking one step forward and three steps back.