To get a sense of where we are right now in the omnichannel evolution, it pays to have a holistic view — a global view, in fact.

As recounted in “The 2022 Global Digital Shopping Index,” a collaboration between PYMNTS and Visa’s Cybersource, more than 3,100 consumers and 3,100 merchants across Australia, Brazil, Mexico, the United Arab Emirates, the United Kingdom and the United States recounted the ways in which the lines in commerce have truly blurred.

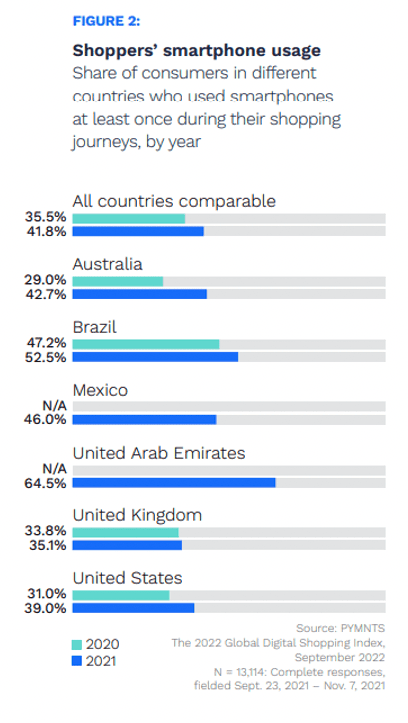

In-store, online, or through a combination of both, the devices are ubiquitous, where the smartphone makes an appearance at some point in the journey between browsing and buying. It’s no surprise that consumers are using their devices more often that they were even as recently as 2020, as the pandemic alighted.

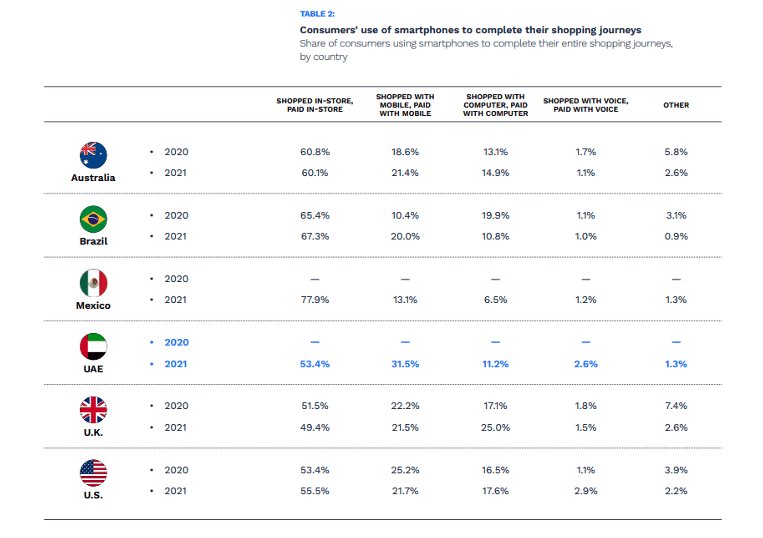

Drill down a bit, and although the phone may be the one constant — wielded by individuals at some point, we find a wide variety of ways and means through which consumers actually complete the transactions. In other words, the final piece of the puzzle is how they use these same devices to seal the deal, and even take physical possession of what they’ve paid for. A majority of consumers still shop in store and pay in store. A growing number of individuals shop through mobile means and pay with mobile devices. A very small sliver of consumers, in the low-single-digits, have embraced voice conduits.

The broad range of shopping activities, the mashup of online channels and the variance market to market offer up some key lessons for merchants, especially the ones who want to go global.

One lesson is that no two markets are really the same. What works in the U.K. might not work in the UAE. But regardless of country or markets, it is imperative that merchants be finely attuned to payment preferences among their existing and would-be customers.

Fortunately, the data also shows that a majority of merchants also offer, as part of their shopping “features,” the ability to craft and use consumer profiles that, among other things, include payments-related details. Being able to have the relevant shopping history on hand means that merchants can “meet” consumers where they want to be met and can offer the payment methods most often used by those individuals in a proactive way. Having some personalization in the mix can cement consumers’ affinity to a brand, to a merchant and even to a brick-and-mortar location.

The flip side of the coin also applies here. The merchants who do not offer payments optionality wind up risking the loss of a customer. Having those individuals make their way to the store, or to the checkout page, only to find friction in the process — well, time’s been wasted. And for an omnichannel commerce landscape where there’s no shortage of merchants to choose from, every second counts.