PYMNTS Intelligence documented that through 2024, most consumers made changes in how and where they shopped in response to persistent inflation. Roughly a third of respondents pulled back regardless of whether they were comfortably meeting monthly expenses or struggling to afford goods, services and shelter.

In the meantime, PYMNTS research showed that the overall average credit card debt carried by households stood at more than $5,000, while $7,000 was the commensurate credit card debt held by consumers living paycheck to paycheck with issues paying bills.

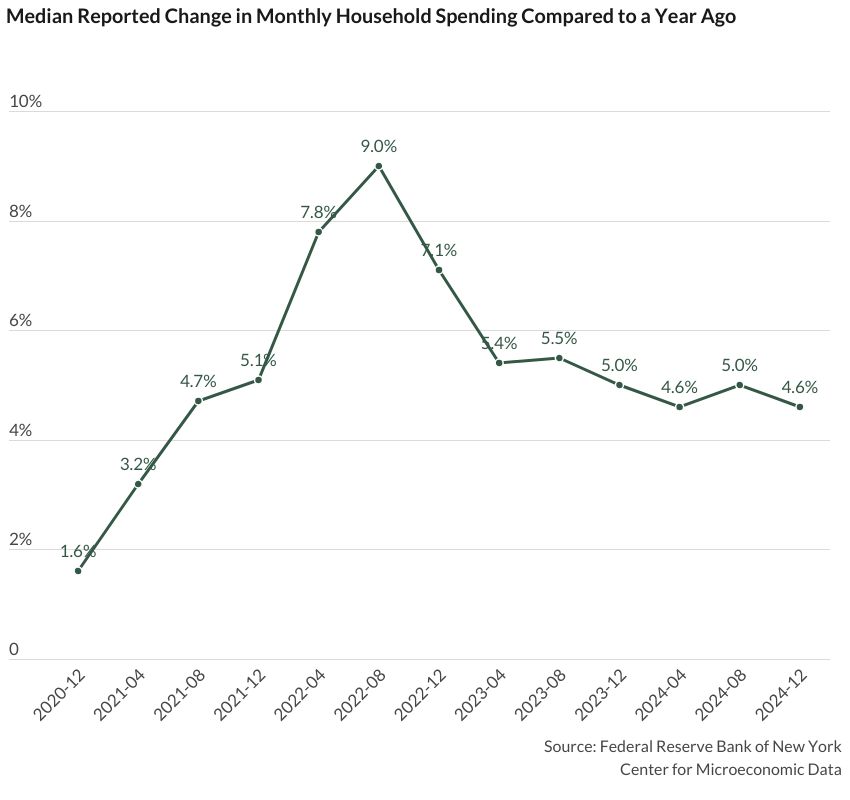

The Federal Reserve Bank of New York released findings Tuesday (Jan. 21) from its December 2024 SCE Household Spending Survey. SCE stands for survey of consumer expectations.

The survey found that spending is healthy but moderating. The median year-over-year increase in monthly nominal household spending decelerated to 4.6% in December, down from 5% in August. We’re well off the peaks seen in 2022 of 9% gains. The biggest impact, most recently, was among the subset of low-income consumers, where spending dropped 1% compared to August’s 4.8%.

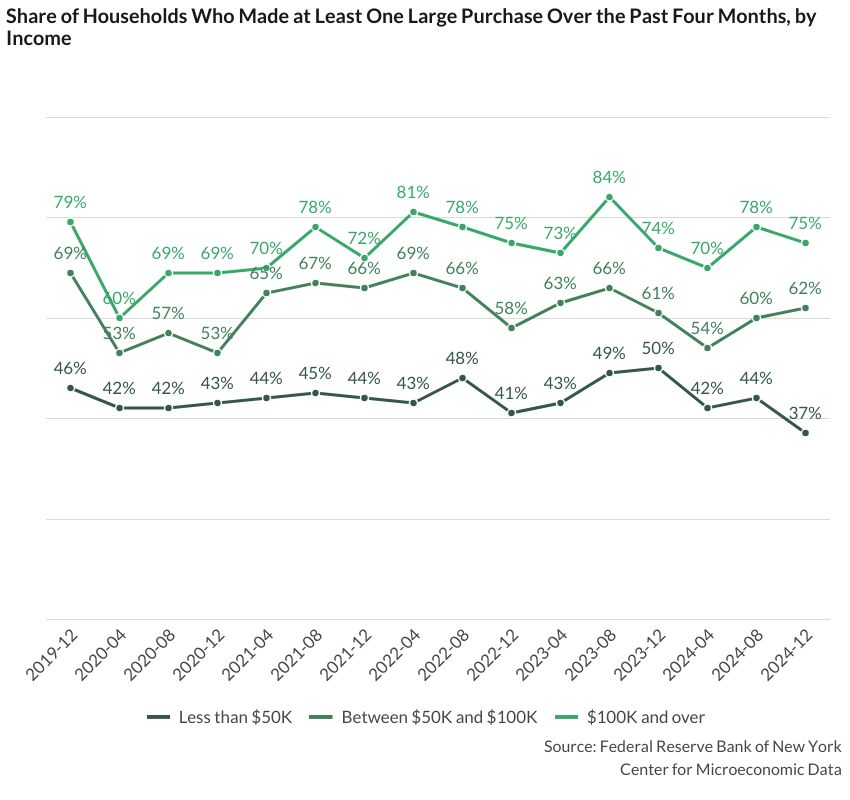

At the same time, the share of households earning less than $50,000 annually that made at least one large purchase over the last quarter of the year dropped to an all-time low of 37%.

The data showed that among these households, the large items purchased most often were electronics (15.2%), home appliances (10.4%) and home improvements (10.1%). In contrast, 3 in 4 high-income households made a large purchase, with vacations (41.1%), home improvements (28.1%) and electronics (27%) being the most popular items. Large purchases were somewhat confined to middle- and high-earning households.

The data showed that among these households, the large items purchased most often were electronics (15.2%), home appliances (10.4%) and home improvements (10.1%). In contrast, 3 in 4 high-income households made a large purchase, with vacations (41.1%), home improvements (28.1%) and electronics (27%) being the most popular items. Large purchases were somewhat confined to middle- and high-earning households.

Looking Toward the Future

Households’ expectations for spending have remained steady at 3% since December 2023, above the 2.4% to 2.6% levels seen in 2019 before the pandemic. Overall, households anticipate their essential spending will grow more than their nonessential spending, with expected increases of 4.1% and 1.5%, respectively.

While the median expected increase for essential spending has dropped since August 2023 across all income groups, low-income households expect the largest increase, with half predicting it will rise by more than 4.4%. In contrast, half of households earning over $100,000 annually expect an increase of up to 3.6%. For nonessential spending, the median expected increase for households earning less than $50,000 annually is 0.7%, compared to 2.7% for those in the highest income bracket.

Should a hypothetical 10% jump in incomes materialize, respondents to the Fed’s survey would seemingly be intent on improving their financial standings. Households queried said they would allocate 47% of the gains to savings or investments, 35% to paying down debt and 18% to spending. Low-income households would allocate 45% to savings, compared to 54% for high-income households, and 21% to spending — 25% more than households earning over $100,000 annually. The remaining 35% would go toward paying off debt.