Amid persistent financial strain for many U.S. households, a new report highlights how convenience services, often seen as time-savers, have become a focal point for household budgeting and spending adjustments.

A PYMNTS report, “How Do Consumers Weigh Convenience Services Against Financial Pressure? It’s About Buying Time,” derived from a survey of 2,878 U.S. consumers conducted between Jan. 8 and Jan. 20, offers a detailed examination of how factors such as price, accessibility and necessity influence the usage of convenience services. These services encompass a broad range, including grocery and restaurant delivery, home maintenance and personal care, all designed to save time but inherently coming at an additional cost. A key finding from the report is that the affordability of these services stands as the single largest barrier to their broader adoption, surpassing concerns about service quality. This underscores that while consumers recognize the time-saving benefits, the financial trade-off in an uncertain economic landscape often dictates their choices.

The report further delineates how the ability to pay and geographical accessibility significantly drive convenience service usage. For instance, urban consumers, who typically benefit from greater service availability, are the most frequent users, with 79% having utilized these services in the past year, spending an average of $234 monthly. In stark contrast, only 51% of rural consumers used such services, with their average monthly spend at $186. Income disparities also play a role; high-income consumers are notably more inclined to use convenience services (75%) compared to lower-income earners (59%).

The analysis suggests that extensive spending on convenience services could be a factor contributing to why some higher-income individuals may still live paycheck to paycheck, indicating a strong prioritization of time over excess liquidity. While grocery and restaurant delivery emerge as the most widely adopted convenience services, each reporting 55% overall adoption, other categories like home maintenance and house cleaning reveal a clearer financial divide, used predominantly by those with greater financial flexibility rather than consumers struggling with bill payments.

Key data points from the report include:

- As of January, 67% of all consumers in the United States lived paycheck to paycheck, representing an increase from 65% in December. This pervasive financial reality shapes a substantial portion of consumer spending decisions, particularly concerning discretionary services.

- Affordability is the paramount concern for consumers regarding convenience services; 51% cite lower prices as the most important factor for increasing their usage, a figure more than twice that of those prioritizing improved service quality.

- Consumers not living paycheck to paycheck demonstrate significantly higher adoption rates for specific services such as home maintenance (34%), lawn care (32%), and house cleaning (28%), in contrast to paycheck-to-paycheck consumers with bill-paying issues, who report rates of 25%, 18%, and 14% for the same services, respectively. This highlights how financial stability enables the use of more costly, less universally essential convenience services.

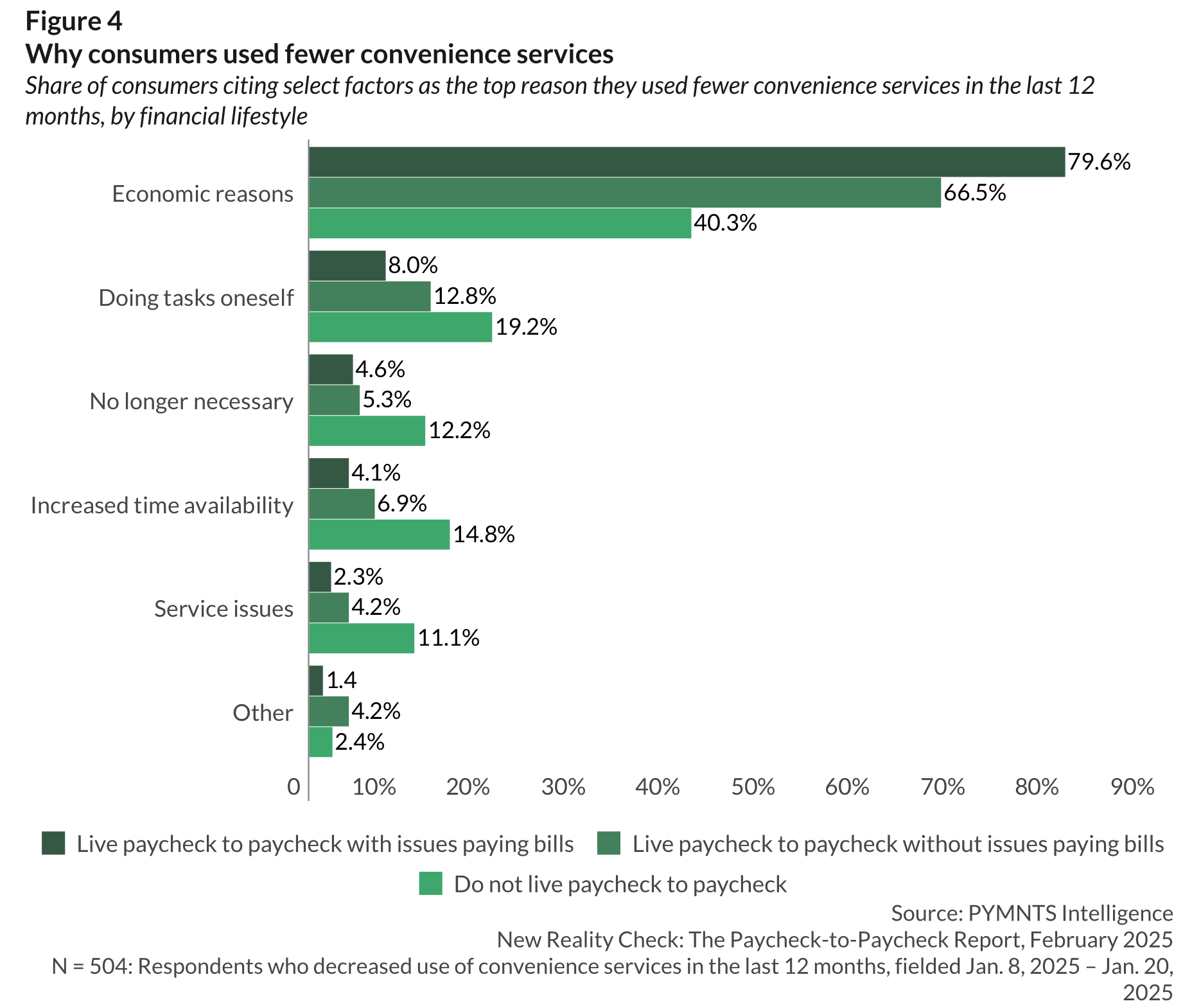

For many consumers, especially those facing financial pressure, the inherent time-saving benefit of these services is often insufficient to justify the accompanying cost. This implies a critical insight for providers: pricing strategies, including the introduction of subscription models, flexible financing options, and targeted discounts, are likely to be far more effective in driving adoption than merely enhancing service quality. The study also observes that reduced usage of convenience services is not always solely due to financial hardship; some consumers not living paycheck to paycheck may cut back due to lifestyle shifts that afford them more available time.