A new PYMNTS Intelligence report suggests the most important shift in consumer credit may not be happening among prime borrowers at all.

The report, “Who Is the Subprime Consumer? A Behavioral Profile,” examines how roughly 44 million Americans with subprime credit scores are adapting to sustained financial pressure and changing payment options.

Its central finding is that subprime consumers are not a temporary or cyclical segment. They are a durable and increasingly distinct part of the consumer economy whose payment behaviors are diverging from traditional credit card models.

The data suggests the old assumption that subprime consumers primarily revolve credit card balances is becoming less reliable.

Instead, many are piecing together payments through a mix of buy now, pay later (BNPL) products, store cards, healthcare payment plans and informal borrowing networks.

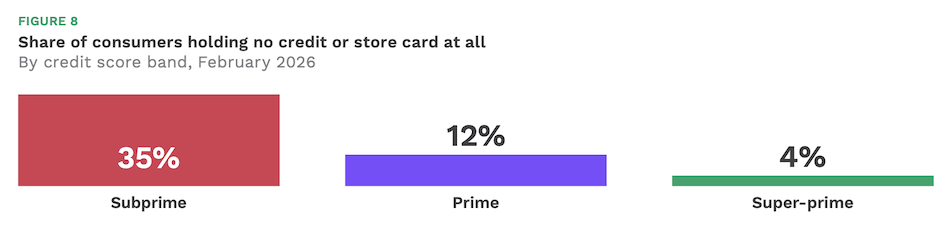

Three findings from the report illustrate the scale of the shift:

- 35% of subprime consumers report holding no credit or store card at all, compared with just 4% of super-prime consumers, pointing to a large population operating partially outside traditional revolving credit systems.

- The share of subprime consumers who always or usually revolve balances fell from roughly 50% in mid-2023 to 38% in January 2026, suggesting that installment and alternative financing products are increasingly replacing traditional revolving behavior.

- 67% of subprime tax refund recipients said refunds were either critical or very important to their finances, reinforcing how dependent many households remain on periodic liquidity events to manage ordinary expenses.

The report also finds that BNPL usage among subprime consumers is highly provider specific.

Klarna, Sezzle, Quadpay/Zip, FuturePay and Acima all over-index with subprime users, while PayPal Pay in 4 and travel-focused provider Uplift under-index sharply. PYMNTS Intelligence argues that the providers attracting heavier subprime usage tend to rely more heavily on thin-file approvals, provider-led underwriting and smaller transaction limits.

Healthcare is emerging as another pressure point reshaping payment behavior.

Among subprime consumers ages 18 to 43, 23% delayed a doctor’s visit because of cost, while 14% did not fill a prescription and 11% rationed medication or reduced dosage. More than one-quarter used BNPL or installment products to cover healthcare expenses and 38% borrowed from family or friends to manage medical bills.

The report argues these behaviors reflect structural cash-flow stress rather than temporary financial disruption.

That pattern also appears in how subprime consumers use tax refunds and one-time payments. More than one-third directed the largest share of their last tax refund toward everyday expenses and bills, while just 14% primarily used refunds for savings or investments.

The broader implication is that subprime consumers are increasingly managing finances around liquidity timing rather than long-term borrowing capacity.

For issuers, lenders and merchants, the report suggests the opportunity may lie less in traditional revolving products and more in financing models built around cash-flow flexibility, smaller approvals and point-of-need payment options. Companies that continue treating subprime consumers primarily as a risk category may miss a large and stable customer segment whose payment behaviors are already reshaping the economics of consumer finance.

At PYMNTS Intelligence, we work with businesses to uncover insights that fuel intelligent, data-driven discussions on changing customer expectations, a more connected economy and the strategic shifts necessary to achieve outcomes. With rigorous research methodologies and unwavering commitment to objective quality, we offer trusted data to grow your business. As our partner, you’ll have access to our diverse team of PhDs, researchers, data analysts, number crunchers, subject matter veterans and editorial experts.