Credit unions (CUs) have long been known for the personal relationships they build with their members. After the pandemic forced customers to adopt a digital-first mindset, customers still wanted individualized attention, but they wanted it delivered through digital channels, with in-person services and live call centers as an option, if needed.

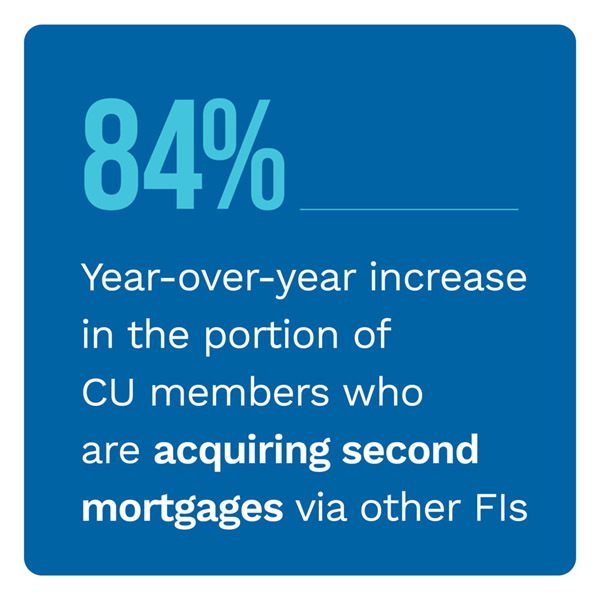

Many CUs are hesitant to innovate, due to either lack of resources or indifference to new technology. This mindset can be detrimental to CUs’ continued success, however, as 84% more CU members are securing second mortgages from other financial institutions (FIs) this year than in 2020. Despite their lack of urgency, 85% of CU executives reported members refinancing mortgages at another FI would negatively impact their institutions’ profit margins.

In the latest “Credit Union Tracker®,” PYMNTS examines how CUs can increase member retention and ensure customer satisfaction through a combination of personalized digital tools and human-first experiences.

Around the Credit Union Space

Financial uncertainty made consumers wary of purchasing new cars during the pandemic. Lending services from CUs for new car loans subsequently took a hit, but used car loans, first-time mortgages and credit card loans made up for the lost revenue. Used car loans increased 6.4% to $254.1 billion in July, according to a released Consumer Credit Report released by the Federal Reserve. Additionally, first mortgages rose 8%, adding momentum to the 13.4% increase during July of the previous year.

Consumers have come to expect the most up-to-date digital apps and tools from their FIs. The accelerated digitization that resulted from the pandemic gave technologically inclined challenger banks and FinTechs a competitive edge over traditional banks and CUs. Eleven million customers joined the competition, while only 4.2 million members signed up at CUs during the same period. However, Jeremiah Lotz, managing vice president of digital and data at PSCU, told PYMNTS that challenger banks often lack the level of personalization CUs provide, and CU executives can use the trust they have built with customers combined with emerging tools to regain their leader status.

CUs need to invest in digital tools and services to remain relevant among emerging challenger banks. The board of directors for PSCU, a credit union service organization (CUSO), signed off on an additional $54 million investment into Lumin Digital, a cloud-native digital-banking subsidiary. The investment is expected to fund product innovation and platform automation for a more personalized banking experience, reported Lumin Digital President Jeff Chambers. A total of 1.2 million users across 23 CUs already use the services Lumin Digital offers.

CUs need to invest in digital tools and services to remain relevant among emerging challenger banks. The board of directors for PSCU, a credit union service organization (CUSO), signed off on an additional $54 million investment into Lumin Digital, a cloud-native digital-banking subsidiary. The investment is expected to fund product innovation and platform automation for a more personalized banking experience, reported Lumin Digital President Jeff Chambers. A total of 1.2 million users across 23 CUs already use the services Lumin Digital offers.

For more on these and other stories, visit the Report’s News & Trends.

Community First Credit Unions Leverages Personalization to Outcompete FinTechs

Over the past 18 months, consumers have gotten used to and even prefer mobile and digital banking platforms. Through online portals and mobile applications, customers can pay bills, view statements, deposit checks and even apply for loans and mortgages.

One definitive change that CUs underwent during the pandemic was that branch-centric customers began interacting with call centers, said James Urban, assistant vice president of the Member Experience Center at Community First Credit Union. Although members looked favorably upon new technology, they still wanted the option to speak to a human representative to address more nuanced issues.

To learn more about why CUs should combine human banking experiences with digital ones such as live support via chat or phone, visit the Tracker’s Feature Story.

Deep Dive: Why CU Members Want Improved Mortgage, Loan Options

CU members often report they are highly satisfied with the customer experience their FI offers. While CUs offer many of the same tools and services as challenger banks, their nonprofit status allows them to provide members with additional perks, such as higher yielding interest on accounts, lower rates on loans and reduced costs and fees. However, customer approval is slowly declining, likely the result of friction-filled online loan services. A lack of seamlessness in digital operations is another potential culprit, with banks and FIs usually performing better in this department. CU executives lack interest in innovating new digital products for loans and lines of credit, but failure to do so may result in a hit to their revenue stream.

To learn more about how refusal to advance technology for financial tools and services can lead to unsatisfied customers and profit loss, visit the Tracker’s Deep Dive.

About the Tracker

The “Credit Union Tracker®,” done in collaboration with PSCU, is the go-to monthly resource for updates on trends and changes in the credit union industry.