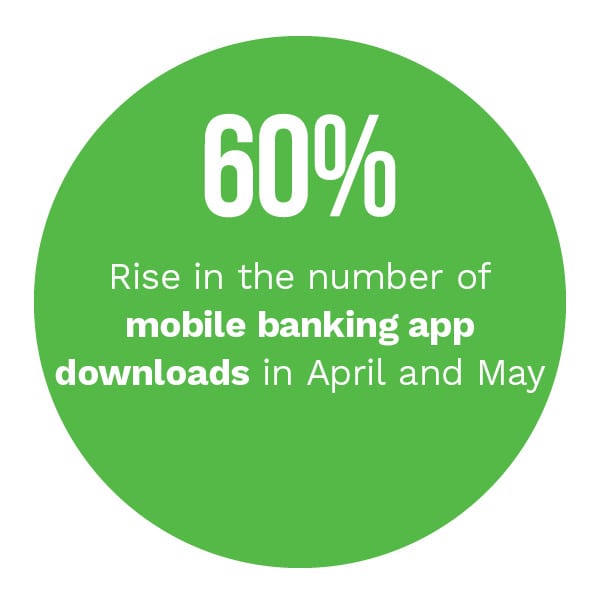

PYMNTS research found that financial institutions (FIs) in the United States alone saw a 60 percent increase in the amount of consumers who downloaded mobile banking apps in April and May, for example. The overall use of digital banking tools has also shot up, with 46 percent of consumers claiming they have increased their use of online or mobile financial tools since the start of the global health crisis.

Yet consumers are still clinging to traditional channels such as brick-and-mortar branches even as  they accelerate their use of online and mobile technologies. PYMNTS research found that 21.6 percent of consumers consider themselves omnichannel banking users, meaning they use both physical and digital channels to conduct their banking activities.

they accelerate their use of online and mobile technologies. PYMNTS research found that 21.6 percent of consumers consider themselves omnichannel banking users, meaning they use both physical and digital channels to conduct their banking activities.

In the November-December Digital-First Banking Tracker®, PYMNTS examines how the pandemic is pushing the adoption of omnichannel banking forward, as well as the changing role of the physical bank branch within this new financial environment.

Developments From Around The World of Digital-First Banking

Consumers are using more digital banking tools than ever, but they still want bank branch access, according to one study, which found that 98 percent of consumers who have recently swapped their FIs in favor of a new bank chose one that supported physical branches, for one example. This indicates that having the option of such a familiar channel still holds some sway over consumer loyalty, even during an age when they expect instant, digital access to their financial accounts. Banks must therefore be careful to achieve the right balance between digital connectivity and the familiarity of brick-and-mortar banking to retain these customers.

Research has also found that striking that balance can have notable impacts on banks’ bottom lines. One study found that supporting omnichannel banking can double their revenues, as well as reduce the amount of customer churn. The study also found that offering this type of omnichannel banking experience makes it easier to cross-sell products to customers because it provides multiple points of contact. More opportunities for contact allows banks to collect more data and potentially pitch more personalized products, for example. This also allows them to communicate more freely and easily with consumers, both factors that can increase the potential to gaining their loyalty and thus bumping up their revenue.

One aspect of brick-and-mortar banking that appears to be becoming more important to consumers — especially during the pandemic — is it the ATM, with consumers heading to these machines to withdraw cash or conduct other financial activities without having to interact closely with human tellers. Many of these consumers are still expecting these ATMs to meet their changing digital standards for seamlessness and convenience, however. This is why New York-based Northern Credit Union is in the process of creating an advanced ATM at its Sackets Harbor location. Advanced ATMs enable consumers to conduct all of the typical transactions one might conduct through that interface, but with a few digital twists.

One aspect of brick-and-mortar banking that appears to be becoming more important to consumers — especially during the pandemic — is it the ATM, with consumers heading to these machines to withdraw cash or conduct other financial activities without having to interact closely with human tellers. Many of these consumers are still expecting these ATMs to meet their changing digital standards for seamlessness and convenience, however. This is why New York-based Northern Credit Union is in the process of creating an advanced ATM at its Sackets Harbor location. Advanced ATMs enable consumers to conduct all of the typical transactions one might conduct through that interface, but with a few digital twists.

For more on these and other digital-first banking news items, download this month’s Tracker.

Citizens Financial Group On The Importance Of Consistency In Omnichannel Banking

The early months of the pandemic had many consumers reaching for their mobile phones first and visiting branches second. The pandemic may be accelerating digital-first banking, but FIs must take an omnichannel approach to offering consistent messaging in whichever channel the consumer may choose, especially considering more consumers may return to branches in the future.

Banks themselves must therefore prepare to offer a seamless experience across every channel, explained Eric Schuppenhauer, president of consumer lending and national banking at Citizens Financial Group in a PYMNTS interview.

To learn more about how Citizens Financial is approaching these pandemic-driven changes, visit this month’s Feature Story.

Deep Dive: How Upgrading Brick-and-Mortar Branches Can Help FIs Stay On Top Of Digital Banking

Deep Dive: How Upgrading Brick-and-Mortar Branches Can Help FIs Stay On Top Of Digital Banking

Consumer adoption of digital and mobile banking tools is only picking up since the start of the global health crisis, but that does not mean that banks should place all of their focus on digital channels alone. Research indicated that consumers who do not necessarily value digital solutions over physical bank branches are coming to expect the same seamless and convenient banking experience, regardless of whether they head into a branch or whether they open their mobile apps. Banks should therefore not discount the role of branches just yet.

To learn more about why digitizing aspects of this channel can help keep consumers engaged and satisfied with their banking experiences, visit the Tracker’s Deep Dive.

About The Tracker

The Digital-First Banking Tracker®, done in collaboration with NCR Corporation, is your go-to monthly resource for updates on trends and changes in digital-first banking.

Consumers were forced to swiftly adapt to a world where their primary way to interact with businesses or banks became digital-first, with the pandemic seemingly increasing the number of consumers turning to digital tools to conduct their financial activities.

Consumers were forced to swiftly adapt to a world where their primary way to interact with businesses or banks became digital-first, with the pandemic seemingly increasing the number of consumers turning to digital tools to conduct their financial activities.