Retailers can’t solve card declines caused by insufficient funds, but incorrectly entered pay information may be a more fixable problem.

Merchants and retailers, especially in the eCommerce space, have a lot riding on reducing checkout friction. After all, 55% of consumers say a frustrating checkout experience is enough to make them quit the process mid-transaction. Adding to that pressure are the 91% of consumers who cite a satisfying checkout experience as significantly affecting their decision about whether or not to return to a given merchant. The stakes are even higher for the direct-to-consumer (D2C) sector, where 48% of subscribers have terminated their subscriptions because of a payment decline. The rewards for reducing checkout friction are high, however, as a streamlined checkout process has been found to turn deal-chasers into loyal customers.

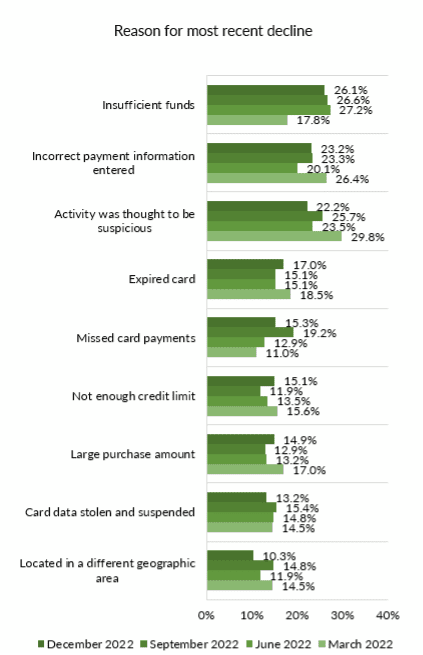

Fortunately for merchants and consumers alike, card declines overall are on the decline, dipping to 17% after the previous quarter’s 18%. PYMNTS’ “Digital Economy Payments: The Ascent of Digital Wallets” details the causes behind surveyed consumers’ recent payments declines.

Source: PYMNTS Digital Economy Payments: The Ascent of Digital Wallets, February 2023 N = 419: Respondents who experienced any payment declines in the last 30 days, fielded Dec. 9, 2022 – Dec. 14, 2022

Data entry errors have consistently been a top-three cause of payment declines over the course of our study and have settled in second place, with 23% of consumers who have experienced a payment decline in the past 30 days implicating them. As a result, efforts to mitigate wrongly entered data may be worthwhile for merchants and retailers. Promoting stored information payment options, such as a credentials vault, may be a potential solution for checkout friction stemming from incorrectly entered information. By reducing the rate of consumers entering their payment details onto a merchant site, it follows that the likelihood of input errors would also go down.

These offerings have garnered consumer interest. PYMNTS research has found that consumers can be incentivized to use a money-storing app, for example, a solution in which consumers’ sensitive details would be securely stored. Data also shows that 40% of consumers are very or extremely interested in using a payments and credentials vault. Given these large rates of consumer adoption or curiosity when it comes to these alternative payment tools, promoting options where customers data are already entered may be as simple as moving the option to the top of payment choice options.

PayPal remains the FinTech to beat when it comes to platforms fitting the bill and is often considered automatically as a pay option. A collaboration with tech firm Bold Commerce allows brands and retailers to both launch sales beyond their websites and broaden their accept payment options to include PayPal and Venmo, as well as credit and debit cards.

Across the Atlantic, business payments FinTech Adyen is the first to provide the Real-Time Visa Account Updater in Europe, meant to reduce involuntary churn. Previously limited to businesses in North America, the tool enables companies to streamline authorization rates from stored Visa payments by automatically updating those accounts — meaning that no merchant integration is necessary.

Most of the reasons behind payment declines are out of merchants’ hands. However, taking steps to reduce the rate of incorrectly entered payment information may be an effort businesses can control. And in this ultra-competitive online retail environment, any edge could be make or break when it comes to customer loyalty and revenue streams.