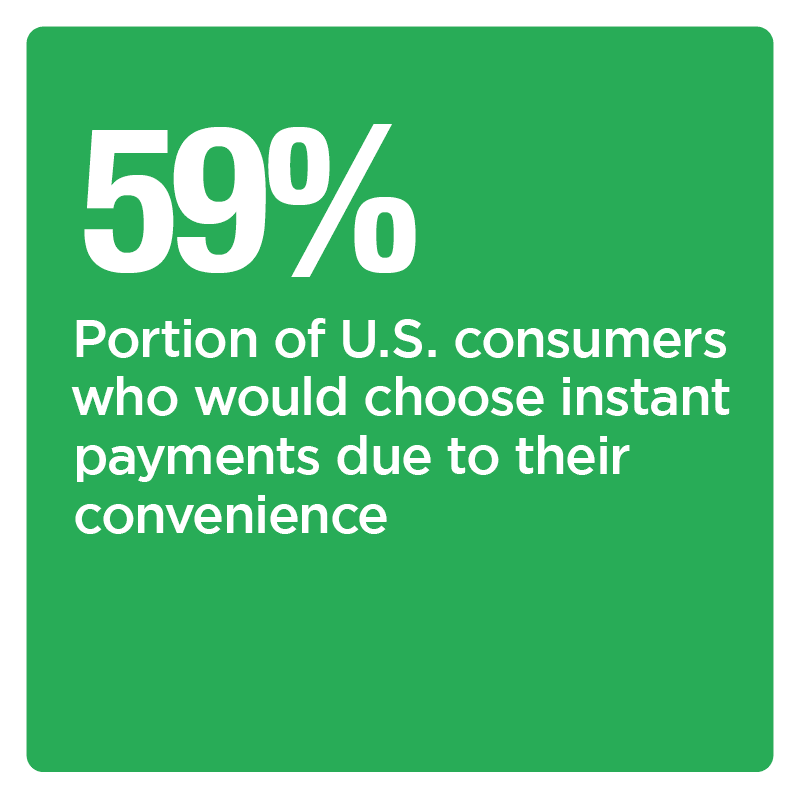

The global payments ecosystem is still in flux after a year of rapid changes caused by the pandemic, and instant payments are becoming more intriguing to consumers around the globe. One PYMNTS study found that 59 percent of United States consumers would use instant payments because of their convenience, for example. Roughly the same number would choose them for their primary virtue: speed.

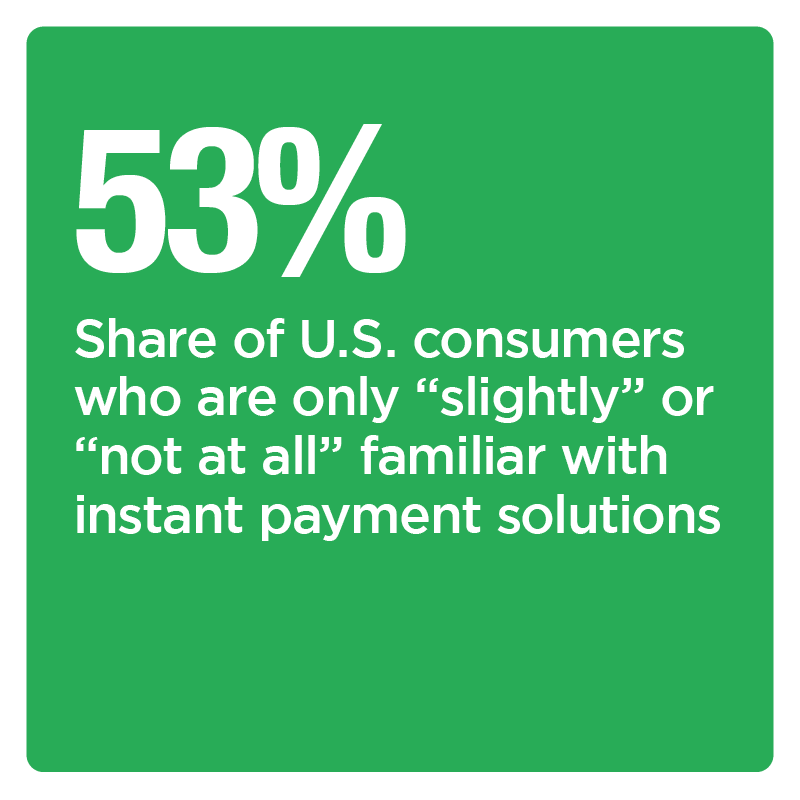

Financial institutions (FIs) and financial players in the U.S. still face numerous challenges to creating the support for the instant disbursements consumers demand, however, including a lack of awareness among potential users. The same PYMNTS report found that 53 percent of consumers are either only “slightly” familiar or “not at all” familiar with instant payment solutions, in fact. Determining how to bridge that awareness divide and build out instant payments at speed might require these entities to look outside of their own markets, such as toward regions like the Nordics where instant payment solutions and usage has been s teadily gaining ground.

teadily gaining ground.

In the February Disbursements Tracker®, PYMNTS analyzes instant payments’ rise in the Nordics with a critical eye to how entities in other regions may be able to use it as a blueprint. The Tracker examines how FIs can apply the Nordic instant payments approach in their own markets, what technologies and tools can help and what challenges may be holding them back.

Around The Disbursements World

Contactless payments in the Nordics have continued to jump in popularity since the start of the pandemic. Fifty-six percent of Nordic consumers were using the payment method at the start of 2020, according to one study, a figure that then rose to 74 percent by November of that year. Many Nordic countries appear to be moving steadily toward their goal of becoming cashless societies, in fact, with another report noting that only 4 percent of transactions in Norway were made via cash. Digital and instant payments thus appear to be taking center stage in the payments economy within this region.

Instant payments are also on the rise in other markets, notably in Pakistan where the country’s State Bank announced the development of its “Raast” or “direct way” instant payments service. The FI plans to roll out the availability of the system in three stages over the next few years. Development of the system will allow payments to move with more speed, but it should also lead to more financial inclusion within the country, particularly among women and more financially vulnerable groups, according to the bank. The development of the system also comes at a time when digital and mobile payments and disbursements are seeing increased use within the country.

This move to digital tools is occurring globally and appears to have influenced FIs in other markets to further innovate their own payments systems. This is especially the case in regions where the popularity of instant payments has also been growing since the start of the global health crisis. Ninety percent of U.S. consumers are now looking for instant payment support from their FIs, for example. Banks are on board with this shift and moving quickly, explained Drew Edwards, CEO of Ingo Money in a PYMNTS interview. The emphasis on digital innovation may be opening up the stage for the development of the next generation of instant payments, in fact — meaning FIs that are still struggling to master the first stage must work to catch up.

This move to digital tools is occurring globally and appears to have influenced FIs in other markets to further innovate their own payments systems. This is especially the case in regions where the popularity of instant payments has also been growing since the start of the global health crisis. Ninety percent of U.S. consumers are now looking for instant payment support from their FIs, for example. Banks are on board with this shift and moving quickly, explained Drew Edwards, CEO of Ingo Money in a PYMNTS interview. The emphasis on digital innovation may be opening up the stage for the development of the next generation of instant payments, in fact — meaning FIs that are still struggling to master the first stage must work to catch up.

For more on these and other stories, visit the Tracker’s News & Trends.

How Global Markets Can Take A Page From The Nordics’ Instant Payments Playbook

Banks and businesses worldwide are attempting to keep pace with the pandemic-driven changes to how consumers want to shop and pay. Many are therefore eyeing how tapping solutions such as instant or real-time payments could help them to process disbursements or transactions at a faster speed — but for those entities still dragged down by outdated payment infrastructure, that is easier said than done.

Expanding instant payments’ availability therefore requires banks to take a collaborative approach in order to be successful, explained Bengt Nilervall, payment expert for the Swedish Trade Federation, in a PYMNTS interview.

To learn more about how instant payments in the Nordics are progressing and how this could influence the expansion of instant payments globally, visit the Tracker’s Feature Story.

Deep Dive: Why U.S. Entities Should Heed The Nordics’ Approach To Instant Payments

Deep Dive: Why U.S. Entities Should Heed The Nordics’ Approach To Instant Payments

The pandemic appears to be highlighting the benefits of these instant solutions in other markets. U.S. consumers’ payment expectations have shifted widely since the start of the global health crisis, for example, with more users turning to digital or contactless payments to make daily transactions than ever. Successfully supporting the kind of seamless, instant payments consumers want means that U.S. banks, FinTechs and payment players may have to make some adjustments to their payment infrastructure, however. Analyzing how Nordic banks and providers have adapted to support instant payments in that market could potentially give these entities the blueprint they need to do so.

To learn more about how U.S. FIs and financial players can apply the Nordics’ instant payment approach in their own market, visit the Tracker’s Deep Dive.

About The Tracker

The PYMNTS Disbursements Tracker®, powered by Ingo Money, is the go-to monthly resource for the latest trends and changes in the digital disbursements space, covering disbursement developments within government agencies, insurance and the retail sectors as well as how instant payments adoption is progressing globally.