In 2021, 59% of United States consumers opened at least one new account with a financial services provider. At the same time, 67% of U.S. consumers access their bank through digital channels, from checking balances and paying bills to monitoring transaction alerts. Bank of America CEO Bryan Moynihan recently said that 85% of deposits are handled or enabled digitally, with only 15% even involving a teller.

As consumers continue engaging with a growing number of options for their financial account needs, account providers need to ensure they are providing the best services to stand out from the competition. Accounts serve as a financial control center for account holders and are critical in maintaining their financial health. As such, account providers must be able to ensure that customers can not only deposit and withdraw funds securely, but can also do so easily and quickly, regardless of the transaction rails involved.

Account holders expect to be able to move money from any account to any account, payer or payee, including moving funds between accounts they hold at different financial institutions. Whether those consumers transfer money into an account through cash, check or electronic means, they now expect to have immediate access to those funds.

This month, PYMNTS examines the growing demand for banking services that enable money mobility, especially for account-to-account (A2A) transactions, and how the innovation of money mobility will continue to play an important role in account providers’ competitiveness.

The Challenges of Digital-First Banking

Account providers such as FinTechs and neobanks face additional challenges when handling non-electronic transactions. While traditional banks have ATM networks and branches to handle such transactions, digital account providers lack that physical infrastructure. Although in-person deposits are in decline, many consumers have turned to ATMs as a substitute for teller visits, and lacking this infrastructure represents a disadvantage to nontraditional account providers. This affects more than cash deposits, as checks deposited digitally have added risk compared to those deposited physically.

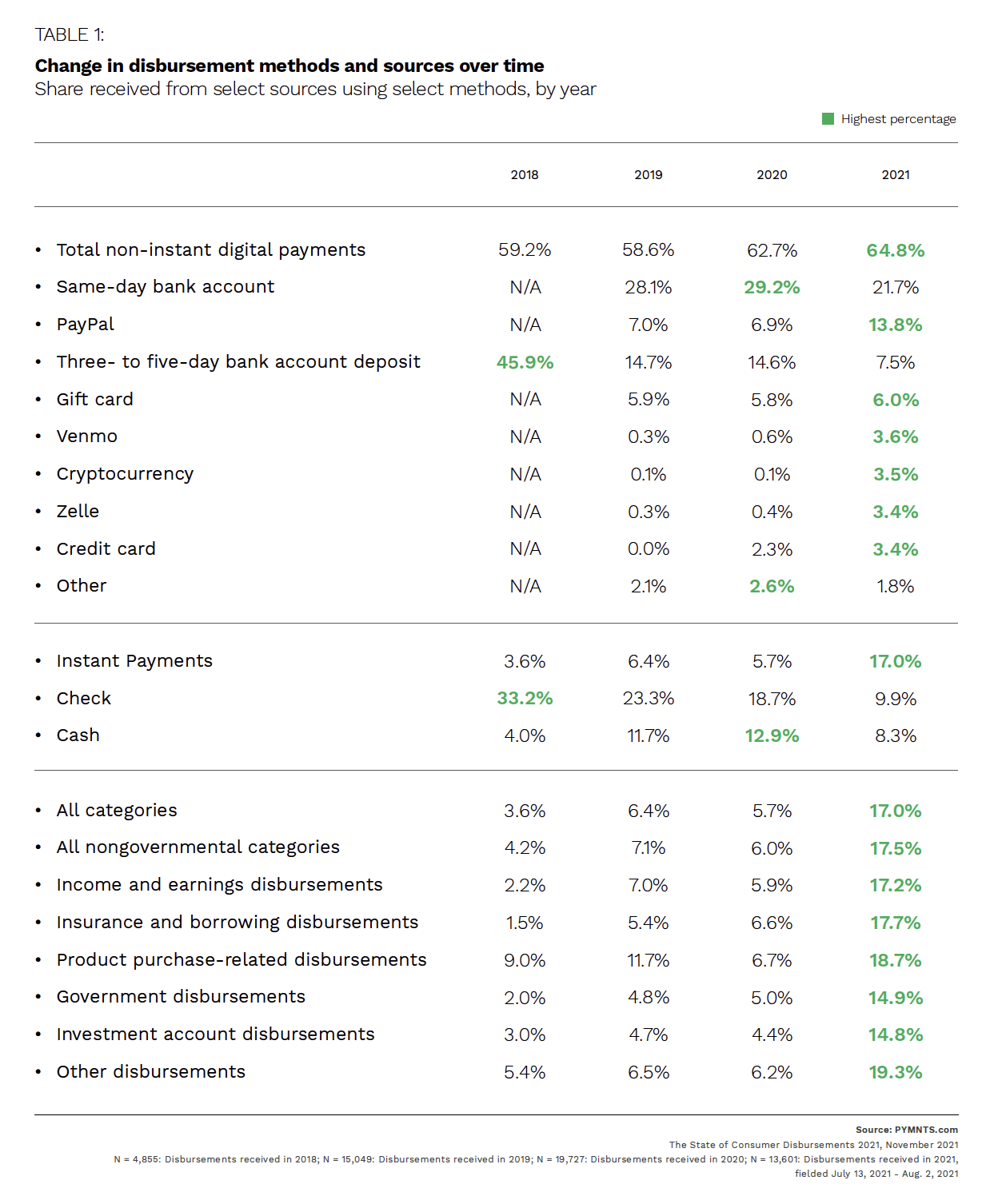

Cash is still used in 21% of transactions in the U.S. and checks account for 50% of payment volume, as they are still a staple for everything from payroll to benefit and tax disbursements. As such, providing reliable and timely support for money-in transactions involving paper while also mitigating fraud remains important for nontraditional account providers. For account providers without physical infrastructure, partnerships can offer a strong solution for providing access to paper transactions while managing risk, and those same partnerships can help maintain a digital edge as well.

Maintaining a Digital Focus

Account providers seeking to maintain a footing in the paper transactions space cannot lose sight of consumer demand for greater digital payments ubiquity. Accounts that are money-mobility ready need to deliver consumer-driven payments ubiquity, enabling consumers to have the funds they need, both when and where they need them. Whether that means funding a balance in another account or paying a bill on time, consumers need to be able to move money in and out of their accounts with ease. Instant transactions are no longer an added value for consumers, but rather a baseline expectation.

Consumers are even willing to pay a premium for speed and convenience. Thirty-three percent of consumers said they would pay as much as 5% of their total disbursement in order to have instant access to funds. Many peer-to-peer (P2P) payment apps take advantage of this, enabling users’ instant access to funds in exchange for fees.

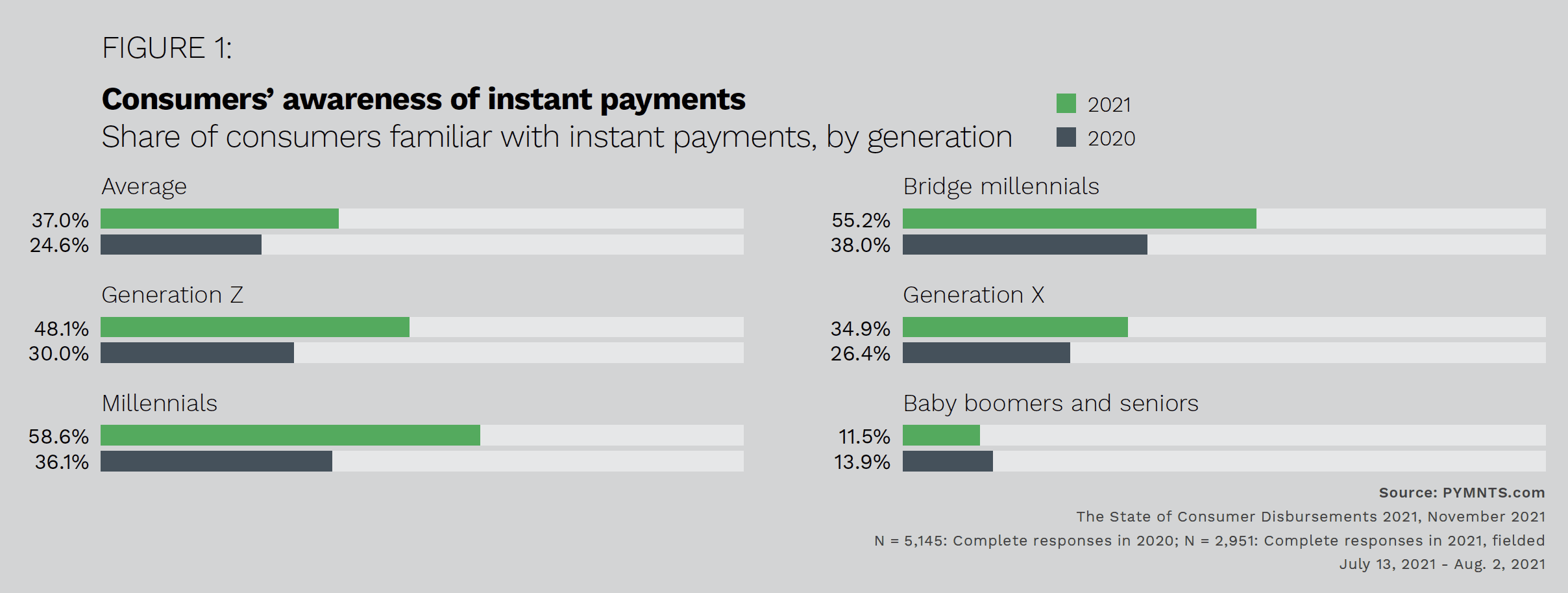

Consumers have grown increasingly accustomed to instant disbursements. Thirty-seven percent of surveyed consumers in November 2021 said they were aware of instant disbursements, a 50% increase over 2020. Among millennials and bridge millennials, that familiarity rose to 59% and 55%, respectively, compared to 36% and 38% in 2020.

Exceeding Consumer Expectations

In an increasingly crowded marketplace, account providers need to modernize money outflows. That requires effective payments management functionality and networked data that provides granular insights and enables real-time risk scoring for transactions. By working with solutions providers, financial services companies can access network ecosystems that make it possible to connect to common payment endpoints and fast payment rails. This can also enable in-demand functionality such as voice commands and other emerging technologies.

As consumers become more accustomed to being able to streamline payments and track spending with digital wallets, they will only expect that convenience to increase. In addition to adding features, providers need to be aware of the desire for greater payments ubiquity and focus on lowering walls that might interfere with money mobility.