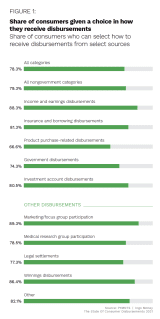

The share of disbursements received via instant payment rails has tripled since 2020, approaching even that of the most common method, same-day automated clearing house (ACH), which commands 22% of disbursements received. In 2021, 17% of all disbursements received were through instant payment channels, compared to 5.7% in 2020. By contrast, cash disbursements fell more than 35% and check disbursements fell more than 50% from 2020 to 2021.

The effort to infuse the economy with funds through stimulus payments following the pandemic’s onset significantly contributed to the number of disbursements consumers received. By July 2020, the United States government had issued approximately 171 million payments totaling more than $400 billion. As economic pressures increased the urgency of receiving funds, consumers grew more interested in instant payments. Given multiple disbursement options, consumers favor instant payments when available.

That desire for faster payments also extends to how consumers connect their accounts. Fifty-eight percent of consumers have linked their bank accounts to at least one other platform or service, such as Venmo or Apple Pay, and 57% of those with linked accounts would consider using a connected service in place of a traditional bank account. This month, PYMNTS Intelligence examines the money-in side of money mobility, including consumer preferences when opening and funding accounts, the trends shaping disbursements and what consumers expect from account providers.

Taking the Nondigital Route

Consumers generally favor digital rails when opening new accounts, but exceptions remain. It may seem counterintuitive that 29% of consumers between the ages of 18 and 24 would prefer to open a financial account through traditional rails such as phone and mail, while less than 8% of consumers older than 65 prefer these legacy methods. Despite mobile apps’ ubiquity in younger consumers’ lives, just 49% of consumers under 25 said they would be comfortable downloading a financial institution’s (FI’s) app to open a new account.

The type of new account they are opening also affects consumers’ channel preferences. Seventy-one percent of consumers said they would be willing to open a new credit card account digitally, 64% would do so for cell phone billing and 62% would open checking and deposit accounts in digital channels. Meanwhile, just 24% of consumers said they would be comfortable using digital means to open either a mortgage account or a personal loan. Despite the close linkage of buy now, pay later (BNPL) accounts with online transactions, just 23% of consumers said they would feel comfortable opening a BNPL account purely through digital rails.

The Pull of Digital Channels

There is no doubt that digital has become integral to most consumers’ financial lives. A recent survey of U.S. consumers found that 84% were able to name at least one banking app feature they use, and 39% said they rely on budgeting apps to track their finances. Another survey found that 35% of U.S. consumers considered mobile check deposit to be a banking app’s most valuable feature, followed by statement and account-balance viewing at 33%, the ability to transfer funds at 31% and bill payment at 28%.

Comfort with digital channels has prompted many consumers to consider using digital-first entities as their primary FI. Thirty-seven percent of consumers aged 40 or younger said they would select a FinTech over a traditional bank when selecting a primary FI. Fifty-seven percent of all consumers said they would consider using an app, such as Apple Pay or Venmo, for this purpose. That share jumped to 75% among Generation Z respondents but fell to just 20% among baby boomers.

Putting it Together

FinTechs may face a daunting task if they attempt to build in-house solutions to meet consumers’ widely varying money-in account needs and preferences. The operational costs of managing multiple rails can quickly become overwhelming, and risk mitigation is always more challenging when working alone. Partnerships can offer the means of fulfilling those needs without getting bogged down in costs and details that can detract from a FinTech’s core mission.