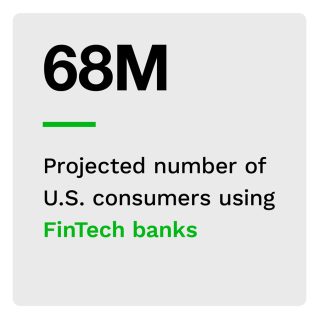

FinTechs have rapidly become an integral part of the United States banking ecosystem. Sixty-eight million consumers across the country use FinTechs such as Chime, Sofi and Ally, and 30 million consumers use such FinTechs as their primary financial institution (FI) in place of traditional banks — and their numbers are growing stronger with each passing year.

Which consumers are signing up to bank with FinTechs? What is driving them away from traditional banks and credit unions, and what can they teach FinTechs about attracting new customers?

In “The Role Of FinTechs,” a collaboration with Ingo Money, PYMNTS goes into the field to learn more about the role FinTechs play in consumers’ everyday lives. We surveyed a census-balanced panel of 3,633 consumers about whether they used FinTechs, the services they used from those banks and what they expect and demand from them.

Key findings from our research include:

Key findings from our research include:

• FinTechs are most popular among bridge millennials, low-income consumers and paycheck-to-paycheck consumers who struggle to pay their bills. Bridge millennials — the cohort of consumers including younger members of Generation X and older millennials — are the most likely of all these demographic groups to use FinTechs, with 48% of them doing so.

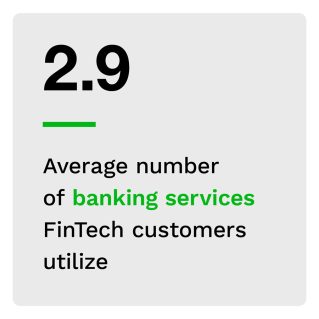

• On average, consumers who use FinTechs as their primary FI use nearly twice as many services as those who use them as secondary FIs — and Chime customers use the most services of all.  Consumers who use FinTechs as primary FIs use these banks for 3.7 services, while those who use them as secondary FIs use these banks for 2.3 services.

Consumers who use FinTechs as primary FIs use these banks for 3.7 services, while those who use them as secondary FIs use these banks for 2.3 services.

• Many consumers specifically use FinTechs to avoid paying fees to send or receive instant disbursements. Just 16% of consumers who use FinTechs as their secondary FIs say they are very or extremely willing to pay extra for instant disbursements, making them far less likely than other FinTech customers to do so.

These are only a few of the industry trends reshaping the banking ecosystem in the U.S. “The Role Of FinTechs” provides actionable insights about how FinTechs can learn from these trends and encourage more traditional banking customers to make the switch.

To learn more about how FinTechs can tailor their services to meet banking customers’ rapidly shifting demands, download the report.