Consumers tend to overestimate their financial literacy, according to a survey by research provider Raddon; 44 percent said they were “very” or “extremely” literate, but when given a financial quiz only 6 percent scored an “A.” Overconfidence can lead to costly mistakes.

The good news according to a February 2019 PYMNTS and Unifund study, Financial Invisibles, is that many consumers were eager to learn more, though. In Q3 2018, 28.0 percent were “very” or “extremely” interested in financial education, higher than in the previous two quarters.

In the PYMNTS and Unifund study, those who indicated they had experience with living paycheck-to-paycheck had higher interest in financial education; 44.0 percent of this group were “extremely” interested in becoming more financially literate. Most consumers (52.3 percent) expressed an interest in hints and tips as far as financial education was concerned rather than attending in-person or online classes.

But education can only go so far.

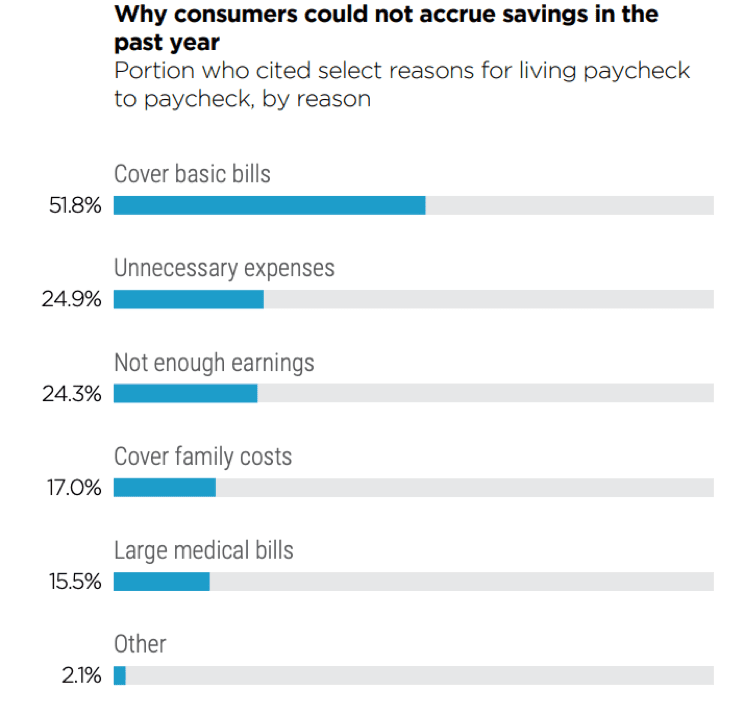

Consumers who find themselves living paycheck-to-paycheck aren’t blowing money frivolously. The majority (51.8 percent) are stretched covering basic bills, and nearly one-quarter (24.3 percent) simply don’t make enough to cover their costs.

In Q3 2018, more consumers reported being better off financially versus one year ago, but perception doesn’t always match reality; 41.2 percent said they had fallen behind on bill payments, up from 33.3 percent in Q1 2018.

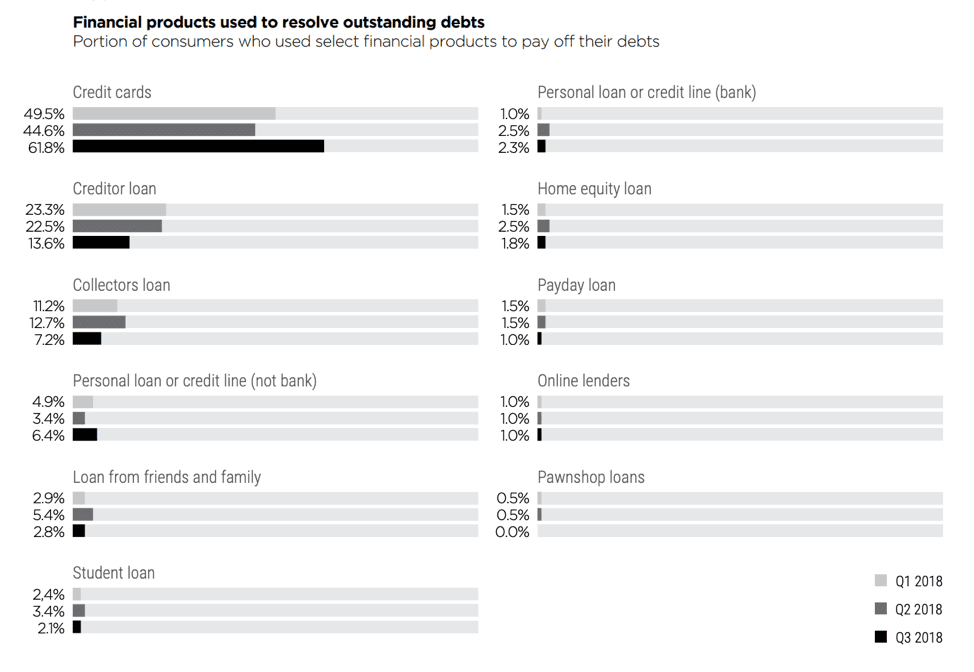

The study also discovered a vicious cycle that kept consumers trapped by debt. The number one financial instrument for paying bills was credit cards; 61.8 percent used credit cards this way in Q3 2018, up markedly from 49.5 percent in Q1 2018.

Those who had used credit products to resolve debt weren’t feeling very confident about their situation. Only half (50.3 percent) reported no delinquency and that they were doing well while 22.1 percent were debt-free but struggling. More than one-in-four (27.7 percent) felt likely to face delinquency again in three months.

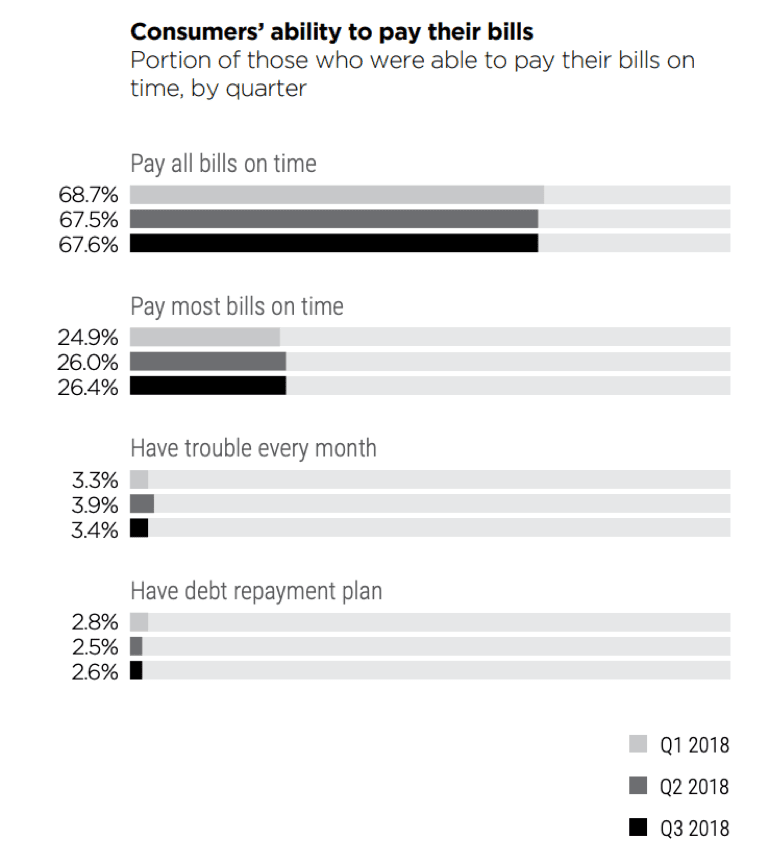

On the surface, that more than 67 percent of consumers in 2018 were able to pay their bills on time sounds good, but using credit to pay these bills is an unsustainable game and perhaps a symptom of much needed financial literacy.

Using credit in this manner is often a short-term fix, which is why many of these consumers continue struggling to pay down bills.

One of the few bright spots in this method of resolving debt is that using credit and making regular payments can raise a credit score. Indeed, in Q3 2018 36.2 percent said their credit score rose over the past year.

It would be easy but unfair to assume that many of these struggling consumers were lower income, and it turned out that many who turned to alternative financial products like pawnshop or payday loans didn’t fit the typical profile.

More than one-quarter (25.5 percent) of those who took out pawnshop loans in the past year had college degrees and 65.5 percent had full-time jobs, while one-third (33.3 percent) of those taking out payday loans had college degrees, 69.6 percent were employed with an average household salary of $80.5k.

At first glance, these consumers wouldn’t seem to be struggling financially, which is further proof of income and academic education being no substitute for financial literacy.

But there might also be value in simply discussing finances among families, according to a Penny Hoarder study released today. It found that one-third of Americans did not discuss personal finance topics growing up. This lack of early discussion led to lower savings and lower earnings as an adult.