Bad actors deploy a staggeringly diverse array of tactics to exact their crimes, ranging from impersonating bank officials to unleashing high-tech botnets.

FIs are working on a number of technologies to fight these financial crime attempts, however. Artificial intelligence (AI) and machine learning (ML) can analyze the thousands of transactions banks process each day in real time, and employee education efforts are proving effective in preventing deception via phishing emails or other social engineering techniques.

The new Preventing Financial Crimes Playbook explores the latest financial crime developments, including a rise in financial fraud related to the ongoing COVID-19 pandemic, new threats targeting digital payment apps and guidance from PNC Financial Services on how multilayered defense systems can help curb the tide of digital scams.

Developments Around The Financial Crimes Space

Developments Around The Financial Crimes Space

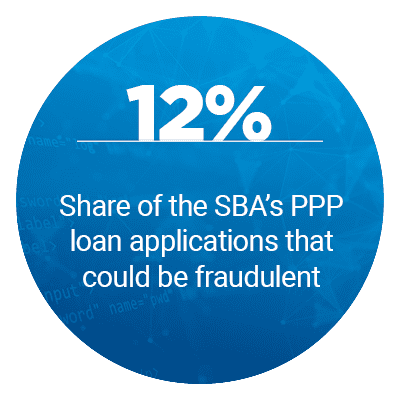

The Paycheck Protection Program (PPP), which offers loan forgiveness to companies that do not lay off any employees, is one of fraudsters’ many targets during the pandemic. Authorities estimate that up to 12 percent of all applications for the program could be fraudulent, with bad actors impersonating businesses to apply for loans they have no intention of repaying. This fraud could account for up to $20 billion of the $660 billion program, although the Small Business Administration (SBA) said that it would not hold banks responsible for issuing fraudulent loans and would instead prosecute fraudsters itself.

Identity theft is also a constant fraud threat, with the Federal Trade Commission (FTC) stating that more than 650,570 cases of identity theft were reported in 2019. This accounted for 20.3 percent of 3.2 million total fraud incidents last year, and also set a new record for the highest amount of identity theft cases in any year in history. The identity theft rate in 2019 was 46.4 percent higher than 2018 and had 160,000 more reported cases than the previous record year of 2015. The FTC attributes this increase to the trove of personal data leaked by high-profile breaches, such as at Capital One and Equifax.

Peer-to-peer (P2P) payment apps are also popular fraud targets, with the Better Business Bureau (BBB) warning against a new threat against Venmo users. Victims receive an unexpected influx of cash and a message from the fraudster asking for the money back, but this money originated from stolen credit cards. The user then returns the money in good faith, but the fraudster has already swapped out the stolen credit card for their own and keeps the stolen funds. The BBB advised Venmo users to prevent this fraud by never accepting transfers from strangers.

For more on these and other financial crime news items, download this month’s Playbook.

PNC Financial Services on Fraud Prevention During the COVID-19 Pandemic and Beyond

Financial crimes of all types are seeing an upswing amid the ongoing pandemic, with bad actors exploiting FI customers’ uncertainty and vulnerability by impersonating tax and public health officials and attempting to steal their money and personal data. The wide variety of fraud tactics requires a variety of tools to stop them, according to Debbie Gould, chief security officer at PNC Financial Services. For this month’s Feature Story, PYMNTS spoke with Gould about why a multilayered defense system that leverages both employee education and AI is the most effective tool at protecting FI customers from bad actors.

Deep Dive: How COVID-19 is Affecting Financial Crime and Efforts to Prevent It

Deep Dive: How COVID-19 is Affecting Financial Crime and Efforts to Prevent It

More than one in five Americans have been targeted by scams or fraud attempts related to COVID-19, including phishing, scam calls from fraudsters pretending to be government authorities and hackers attempting to break into bank networks. These scams can result in the loss of both money and personal information if not stopped, but FIs are deploying a variety of defensive measures to counter them. This month’s Deep Dive explores how FIs are fighting these fraud methods on a number of fronts by leveraging both employee training programs and scanning technologies that harness AI and ML.

About the Playbook

The monthly Preventing Financial Crimes Playbook, a NICE Actimize collaboration, offers coverage of the most recent news and trends in the financial crime prevention space.

Financial crime is a never-ending concern for banks, credit unions (CUs) and other financial institutions (FIs), with trillions of dollars and untold terabytes of personal information stolen every year.

Financial crime is a never-ending concern for banks, credit unions (CUs) and other financial institutions (FIs), with trillions of dollars and untold terabytes of personal information stolen every year.