There is a great deal of economic uncertainty in the world today, as many banking managers and executives are acutely aware. These circumstances have brought to the fore what has long been a central concern for lenders: assessing and managing credit risk.

This vital task is complicated even in normal times due to the multitude of financial risk factors in play at any given time. This is one reason why credit risk has emerged as one of the most promising applications of artificial intelligence (AI). AI is capable of processing and learning from massive volumes of data in real time and can flag risks long before they appear on the radar of conventional models.

Potential use cases and reality, however, are two different things. The actual use of AI in the banking sector has been quite limited, while older legacy systems have remained prevalent, such as business rules management system (BRMS). PYMNTS’ latest research reveals that this is changing, however: The share of financial institutions (FIs) using AI has increased dramatically since 2018. As important, banks are increasingly focused on two main areas where they want to put AI to work: credit risk and payment services.

Potential use cases and reality, however, are two different things. The actual use of AI in the banking sector has been quite limited, while older legacy systems have remained prevalent, such as business rules management system (BRMS). PYMNTS’ latest research reveals that this is changing, however: The share of financial institutions (FIs) using AI has increased dramatically since 2018. As important, banks are increasingly focused on two main areas where they want to put AI to work: credit risk and payment services.

PYMNTS has been closely tracking the adoption and potential of AI across a range of business sectors as part of its Unlocking AI Playbook series, a collaboration with Brighterion. In the latest installment of this series, Credit Risk and Payments Edition, we delve deeper into the specific use cases driving interest in and adoption of AI in the banking sector. The study is based on a survey of 150 U.S. bank executives from institutions with assets ranging from $1 billion to more than $100 billion.

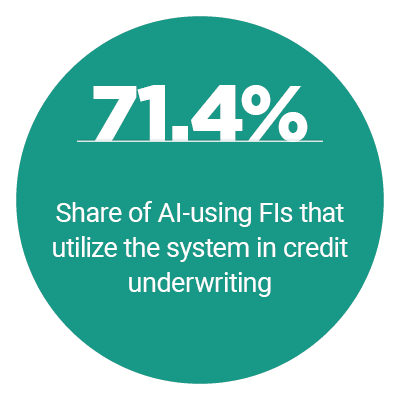

Our research reveals that while AI use remains limited among FIs, it has grown considerably, from 5.5 percent in 2018, when PYMNTS conducted a similar study, to 9.3 percent today. Another key trend is that early AI adopters are more focused in how they are applying the technology. Among banks that use AI, 92.9 percent do so in payment services, and 71.4 percent employ it for credit underwriting. This represents a dramatic increase from 2018, when just 27.3 percent reported using AI for underwriting and risk assessment purposes.

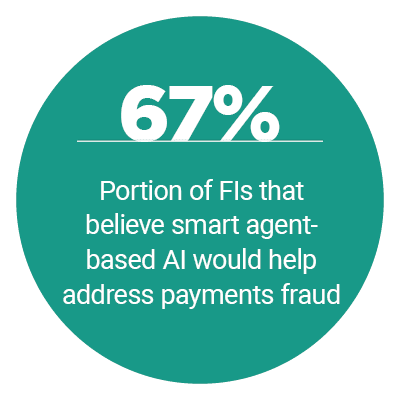

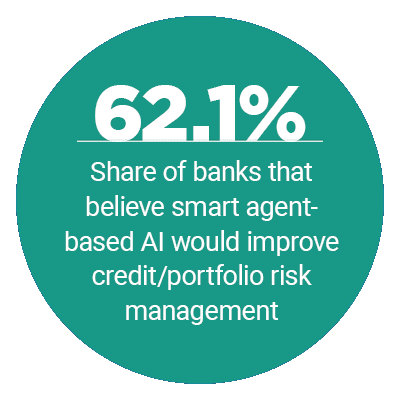

These trends are further reflected in how FIs view the potential of a specific form of AI that makes use of “smart agents,” which can be assigned to multiple entities within a system and offer personalized insights and responses. More than a quarter of FIs would be “very” or “extremely” interested in implementing smart agent-based AI, and among large institutions, those with assets over $25 billion, more than 70 percent have this level of interest. Moreover, FIs see this form of AI as being uniquely beneficial in the areas of payments fraud and credit risk. Among FIs interested in smart agent-based AI, 67 percent believe it would help address payments fraud, and 62.1 percent expect these systems to improve credit/portfolio risk.

These trends are further reflected in how FIs view the potential of a specific form of AI that makes use of “smart agents,” which can be assigned to multiple entities within a system and offer personalized insights and responses. More than a quarter of FIs would be “very” or “extremely” interested in implementing smart agent-based AI, and among large institutions, those with assets over $25 billion, more than 70 percent have this level of interest. Moreover, FIs see this form of AI as being uniquely beneficial in the areas of payments fraud and credit risk. Among FIs interested in smart agent-based AI, 67 percent believe it would help address payments fraud, and 62.1 percent expect these systems to improve credit/portfolio risk.

To learn more about the emerging use cases of AI in banking, download the report.

About:

The Unlocking AI Playbook: Credit Risk And Payments Edition, powered by Brighterion, examines the state of AI adoption in the banking sector and assesses the system’s most promising applications currently and in the future. It also examines how other computational systems are being used to manage payments, regulatory compliance, financial fraud and other important business functions.