FinTech disintermediation has innovated and improved the banking experience, but new research shows that consumers are tired of managing these services as separate relationships, with nearly half saying they would prefer to have more of them bundled by one financial institution (FI).

That’s a huge opportunity for banks and other FIs to win new account holders, especially among younger consumers who drove the finance app revolution and now see value in consolidating into one core relationship, while still getting what they want.

In the study “Bundled Banking Products: Matching Product Offerings With Customer Demand,” a PYMNTS and Amount collaboration, we surveyed nearly 2,300 U.S. consumers about the growing demand for bundled services — from deposit accounts to buy now, pay later (BNPL) loans — finding a powerful appetite for unifying financial services with one primary entity.

Looking at the top motivators behind this consumer quest to streamline and simplify, we found this desire is strong enough to convince people to switch FIs to get bundles they most value.

Get the study: Matching Product Offerings With Customer Demand

Bundling Up

Checking accounts are the most common service consumers hold at their primary banks at 89%, followed by 79% using their primary bank’s debit card and 71% holding savings accounts. This trend deviates with credit cards as 44% of consumers have credit cards from their primary banks, while 37% favor credit cards from other issuers.

The big differentiator tends to be the number of financial products a given consumer uses. The higher that number goes, the more likely a respondent is to vote for more bundling.

Noting that 41% of consumers earning over $100,000 “have six or more products at their primary banks,” the study added that “the fewer banking products a consumer uses, the less likely they are to be interested in a bundled solution with one bank. Nonetheless, PYMNTS’ data shows that 38% of consumers with one to three banking products also want everything bundled at their primary banks.”

Turning Switchers On

As the findings clearly showed, the more banking services and payments types a consumer uses the more likely they are to gravitate to bundled banking. We found that those who think they aren’t getting this level of consolidation from their current FI will go to a competitor.

“Younger generations tend to view bundled solutions as fundamental for their banking needs,” the study stated, noting that 65% of bridge millennials and 64% of millennials “would consider moving their accounts out of banks that do not offer bundled banking products, including 43% of bridge millennials and 40% of millennials who say they are very or extremely likely to make a move. Just 8% of baby boomers and seniors have this view about bundled banking.”

Building Better Bundles

To craft bundled banking offers that appeal to existing account holders and attract those disaffected with their current FI, take a good look at payments preferences.

Among more fascinating findings is that consumers want recommendations on payment methods from FIs, helping match payment type to purchase for optimum value and experience.

For example, the study noted: “Millennials and consumers who use more than six products from their primary banks lead all groups in wanting bank recommendations about which payment methods to use. Overall, 80% of millennials and 76% of bank customers with six or more products say they want their primary banks to recommend the best payment methods for different purchases.”

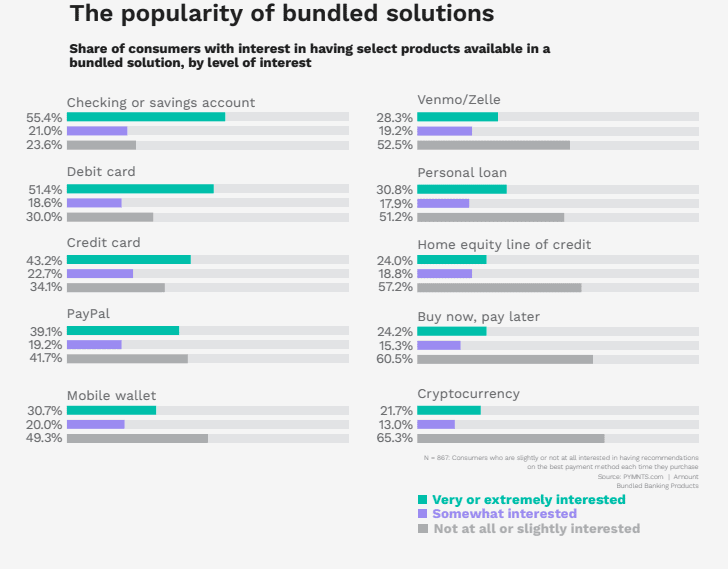

What’s in those ideal banking bundles? We found that 60% of consumers want a credit card, 55% are “very” or “extremely” keen there be a checking or savings account, nearly one in four (39%) want PayPal as part of their banking bundle, and 30% want a mobile wallet.

Download: Matching Product Offerings With Customer Demand