According to Steven Leitman, vice president of Global Payment Experience & Solutions for Visa, that difference also underscores one of the main themes of the Visa report, entitled “Digital Transformations of SMBs: The Future of Commerce.”

According to Steven Leitman, vice president of Global Payment Experience & Solutions for Visa, that difference also underscores one of the main themes of the Visa report, entitled “Digital Transformations of SMBs: The Future of Commerce.”

“There is a wide divide between consumer preferences and what small businesses are doing,” he said during an interview with PYMNTS to further discuss the Visa findings. Those results were based on survey responses from 425 business and nearly 2,500 consumers.

Online Preferences

It’s not difficult to look back into recent, pre-digital history and find examples of significant divides between the practices of SMBs and consumers.

Take parking and hours, for instance. More than few retail-centric downtowns across the United States suffered when malls began to sprout near interstates, and those legacy merchants — many of them locally owned — moved too slowly to offer free parking or longer hours to better compete against those larger retailers.

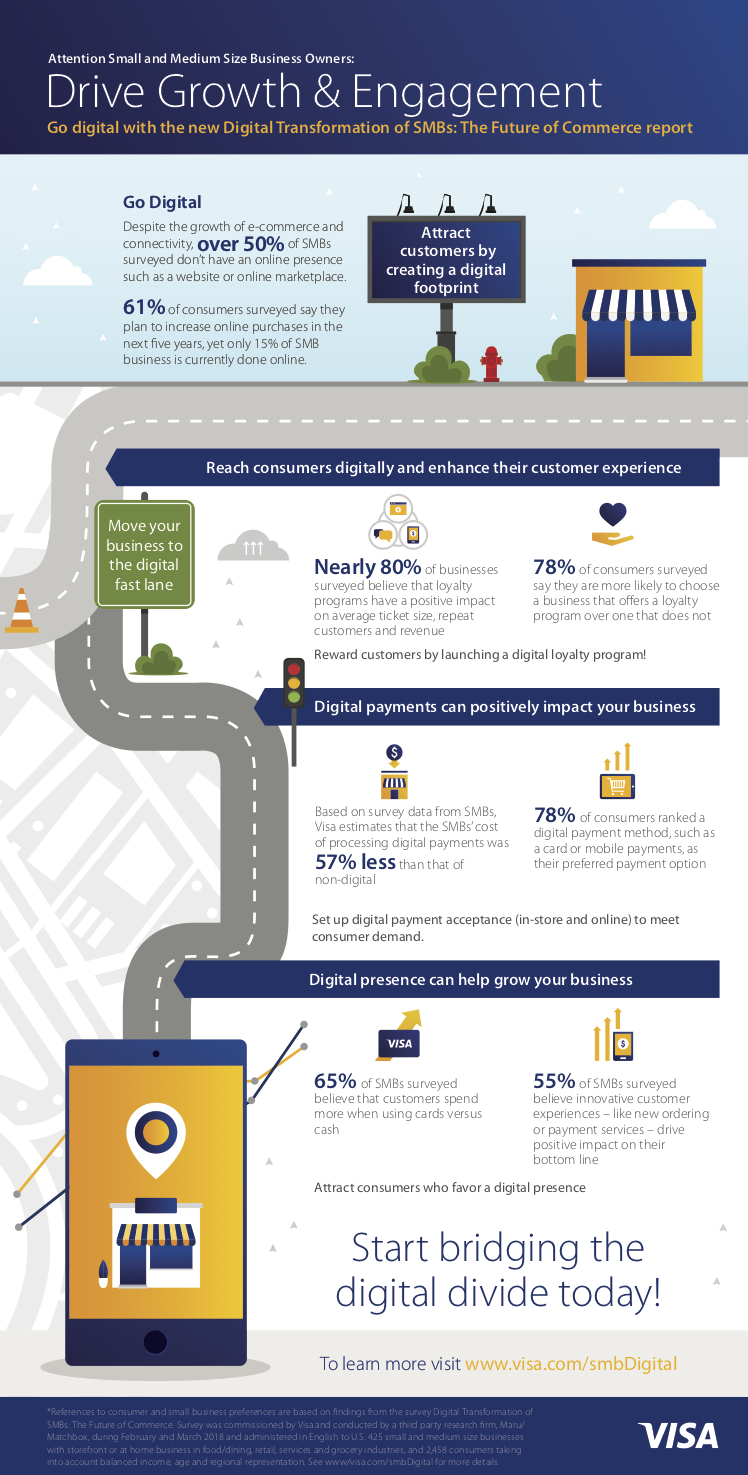

The sense of division continues in the digital age. Visa found that 51 percent of consumers desire to exclusively shop online, but only 46 percent of SMBs have eCommerce websites, sell via online marketplaces or otherwise have digital commerce presences. That’s not something SMB merchants can afford to ignore.

Visa said that “61 percent of consumers plan to increase their online purchases in the next five years” — meaning businesses that fail to up their digital games run the risk of consumers going elsewhere.

Digital Payments

As more consumers go online, more of them also turn away from cash.

The Visa study found that 78 percent of consumers list their top payment option as a digital method, such as a card or mobile device. That preference can lead to more revenue, as 65 percent of SMBs agree that “customers spend more when they use cards versus cash” — a finding that not only applies to products, Leitman said, but results in larger tips for servers, a factor that helps business owners retain good employees.

Still, SMBs often resist moving too fast or far away from cash, discouraged by the real or perceived costs of installing the latest payments hardware or software, or perhaps even slowed by worries that some of their customer base might not entirely trust the security of digital payments. Simple inertia can also play a role.

However, digital payments come with an additional appeal: lower costs. In its report, Visa estimated that the average costs of processing digital payments, including direct expenses and labor costs, are 57 percent lower than for non-digital payments. As Leitman noted, the digital costs are relatively straightforward (such attributes as interchange, chargebacks, cost of POS gear), while the expense of cash can involve a longer list of costs that are not always as clear — for instance, armored car services, leakage, fraud and robbery.

Loyalty Laggards

Loyalty, too, provides an example of the divides that often exist between consumers and SMBs. Visa found that one in five SMBs offer loyalty programs, even though nearly 80 percent of businesses acknowledge that loyalty programs increase average ticket sizes, attract repeat customers and otherwise boost revenue.

“We know that customers want loyalty,” Leitman said. In fact, Visa found that 78 percent of shoppers are more likely to spend money with a business that offers a loyalty program over one that does not. Furthermore, 65 percent of consumers said they study loyalty programs before they go out to eat, choose a service provider or visit a store.

The finding involving loyalty demonstrates that going digital means more than just accepting payments. Tying together the wider consumer experience into a unified SMB platform can increase customer acquisition and loyalty, and serve to grow revenue over time.

“We are not just talking payments, but commerce,” Leitman said.