It is safe to say that most American consumers are fans of real-time payments.

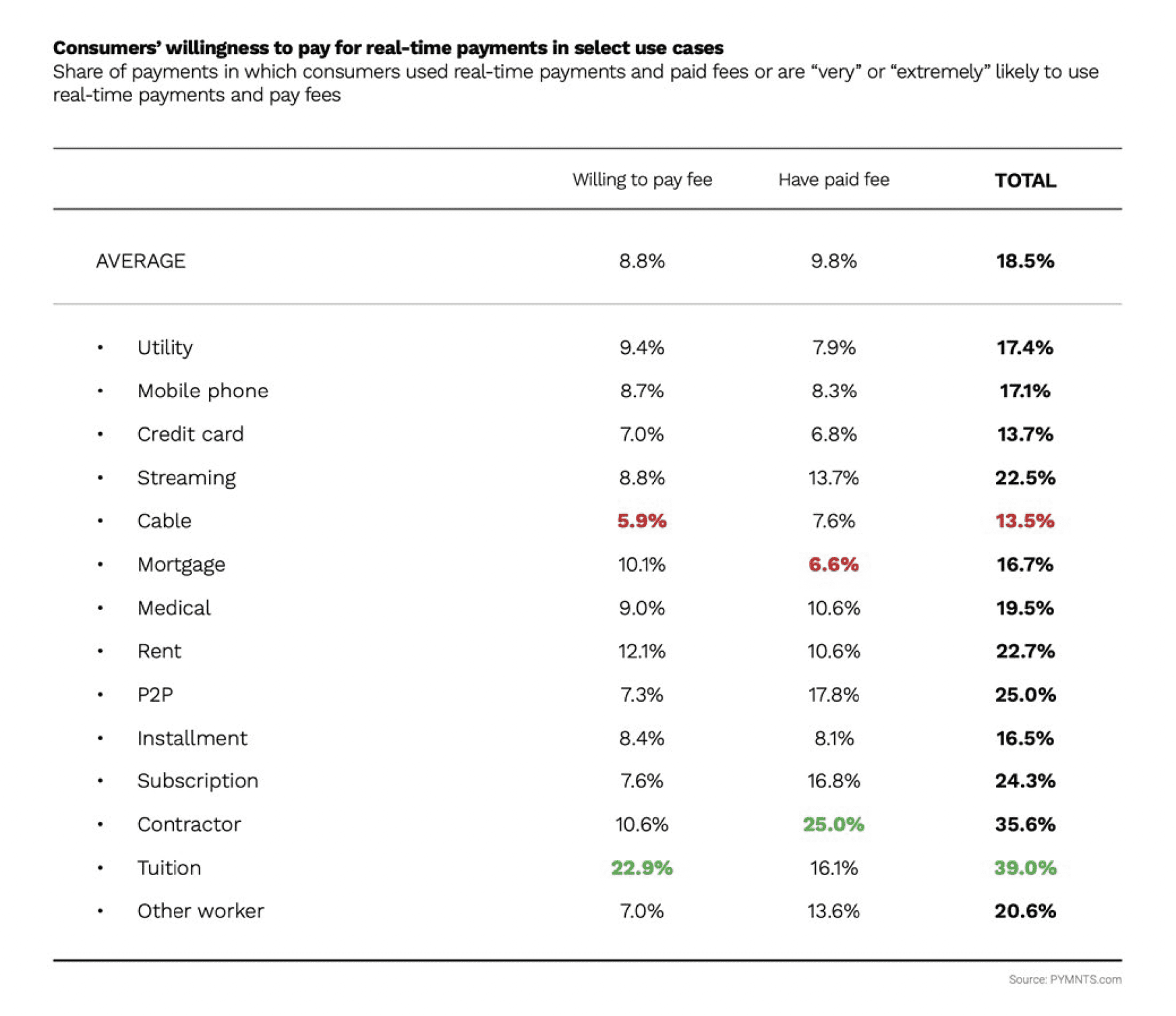

PYMNTS research demonstrates that 70% of U.S. consumers who have used real-time payments services likely would use them again if they were available for free. Their satisfaction with these payment methods is great enough even to transcend cost concerns in some cases, with more than one-quarter of respondents saying they would be willing to pay for access to immediate payments. The survey found that 25% of consumers who have used real-time payments to pay contractors, 18% of those who used them to make peer-to-peer (P2P) payments and 16% of those who used them for tuition payments have already paid fees to do so.

Savvy banks would do well to pay attention to this data. Real-time payments are a crucial consideration for U.S. consumers when selecting financial institutions (FIs), with 30% of those surveyed saying real-time payments access is an important feature they look for when selecting a bank. This underscores the ease and efficiency that real-time payments methods offer consumers, as they can be made 24/7 year-round and enable immediate reconciliation with their bank accounts.

The benefits afforded by real-time payments do not stop there, however. Many of these payment systems, including the RTP® network, are developed with messaging services, such as the ISO 20022 standard, which transfer copious amounts of rich payments data during transactions. This can give payors and payees detailed information about the payments they make or receive, which can be useful particularly when it comes to an increasingly popular feature: request to pay.

Request-to-pay functions allow payees to send messages to payors that ask them to settle bills, and the option allows payors to determine whether to pay the amount requested, ask for alternative payment terms or even deny the payment outright. The clarity that request-to-payment functions provide has been cited as being beneficial particularly for digital payments, with the European Commission saying it adds value to the SEPA Instant Credit Transfer system, for example.

Real-time payments systems also pose challenges that request-to-pay features are well-suited to addressing. Such transactions are irrevocable once funds are sent, making it critical that payors know what they are paying for, and why, when they use such systems. The following Deep Dive examines the rise of request-to-pay features alongside real-time payments and the challenges that real-time payments providers must overcome to encourage further adoption.

How Request to Pay Is Reshaping the Real-Time Payments Landscape

Request-to-pay features undoubtedly are helpful for payors, as they allow them to confirm payment details before sending funds to the prospective payees requesting payment. This function gives payors added flexibility by allowing them to choose how and when to make their payments or whether to deny payment requests for any number of reasons.

There also are distinct benefits for payees when using these features. Request-to-pay can give them better control over cross-border and domestic payments. This ultimately enables them to speed up their reconciliation efforts and avoid spending undue time and resources tracking down payors with outstanding debts.

Research shows that these and other advantages have made request-to-pay functions desirable to a broad range of payments players. A staggering 96% of treasury and payments professionals across Europe are interested in request-to-pay features, according to a survey, and 89% are eager to use them for cross-border payments. The feature also has become closely intertwined with real-time payments systems around the globe, including India’s UPI and others.

Challenges to Request-to-Pay Adoption

Still, key factors must be addressed for the adoption of request-to-pay features to continue to grow worldwide. The treasury and payments professionals surveyed in the European study noted several missing elements they said were necessary to make such functions successful for eCommerce, namely 24/7 year-round service and compatibility with real-time payments systems. They also noted that a more standardized, pan-European request-for-payment system likewise would boost adoption, something the SEPA Request to Pay system aims to achieve.

Several obstacles stand in the way of the push toward a unified request-to-pay service, however. Individual countries in Europe and elsewhere — including the U.K., which operates its Request to Pay system — are rolling out their own request-to-pay services, many of which have unique capabilities and are not interoperable with other real-time payments systems. The continued development of these services could advance the use of request-to-pay features domestically, but the lack of a standardized regionwide system, or interoperability between various systems, could pose hurdles to enabling more seamless cross-border payments. This enhanced interoperability is likely to become increasingly necessary as more eCommerce occurs internationally.

The demand for request-to-pay features is robust worldwide, with businesses and consumers alike expressing appreciation for the capabilities and cash flow efficiencies they offer. Ensuring organizations and consumers make the most of these request-to-pay features will require the development of solutions that work harmoniously with real-time payments systems, especially those that can enable seamless domestic and cross-border payments.