In business, and especially for smaller firms, there are any number of exit strategies depending on the macro environment they must confront.

When markets are booming, management teams can pursue an initial public offering, seeking to tap the stock market to raise operating capital. In many cases, these founders can also monetize their own existing holdings in the company. In tougher times, liquidation or bankruptcy are options.

There usually exists the possibility of pursuing another avenue, where a merger or acquisition can help a struggling firm survive, linking up with cash, yes, but also a strategic roadmap where the combined entity’s proverbial whole would be greater than the sum of the parts.

The window for an M&A exit may be closing for at least part of the FinTech sector — specifically for those smaller companies that have seen share prices plummet and cash burn accelerate.

As reported earlier this month, it’s gotten tougher for would-be suitors in any industry to obtain the capital that’s necessary to finance any deal-making in the first place. Would-be deals totaling more than $150 billion have either been postponed or canceled as financing becomes scarce.

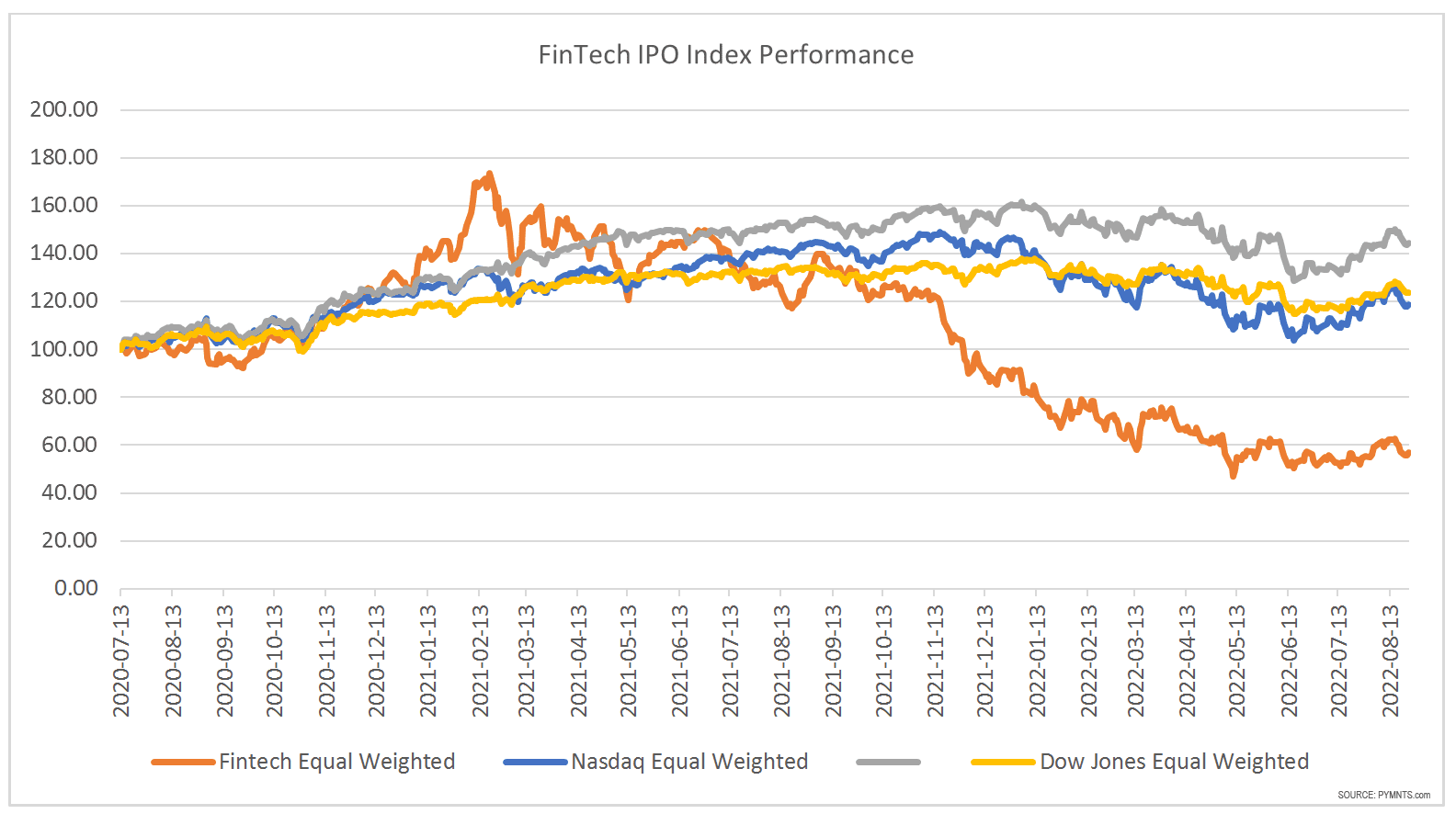

The FinTech IPO Tracker, as formulated by PYMNTS, shows that sentiment on the sector — at least the prospects of some digital-only upstarts — has been anything but positive. As seen below, the index has plummeted 38% for the year, far worse than any benchmark.

Getting a bit more granular in detail, the average return for the more than 40 names in the Index shows an average loss of 46% since the companies’ IPOs — a number that is skewed (to the upside) considerably by Bill.com’s more than 380% return.

None of this is meant to signal any particular name out — but given the fact that only a handful of firms tracked are expected to post any earnings over the longer term, the pressures are a bit evident.

The average market cap of the FinTech IPO member is about $3 billion, which indicates that the financial “hurdle” of acquiring one of these companies is not insignificant, even with the recent downturn. Of course, there are names such as Katapult and OppFi where the market caps are, respectively, about $100 million and $300 million. In just one example, Katapult, as noted in this space recently, has seen its gross originations decline by double-digit percentage points and has cited macro turbulence as impacting consumer confidence and spending. Elsewhere, companies that are busily expanding operations (such as Paysafe, into Argentina, in a recent announcement) are being punished by the markets.

And as share prices continue to be volatile, it must be noted that using stock as currency becomes less attractive (and less feasible) to get deals done. And in the meantime, at least for some companies, the cash burn continues, as evidenced by, for example, Katapult’s negative $1.7 million in operating cash flow through the first six months of 2022.

Now, innovation is a long-term game, and within FinTech innovating financial services away from paper-laden and manual processes takes time (and money). But in the current environment, with deal-making increasingly on the back burner, the pressure is on to make more money in less time.