In times of turmoil, when the economy wreaks havoc with household budgets, visibility into cash flow becomes king.

No surprise, then, that debit, as a payments choice, should be top of mind and top of the proverbial wallet.

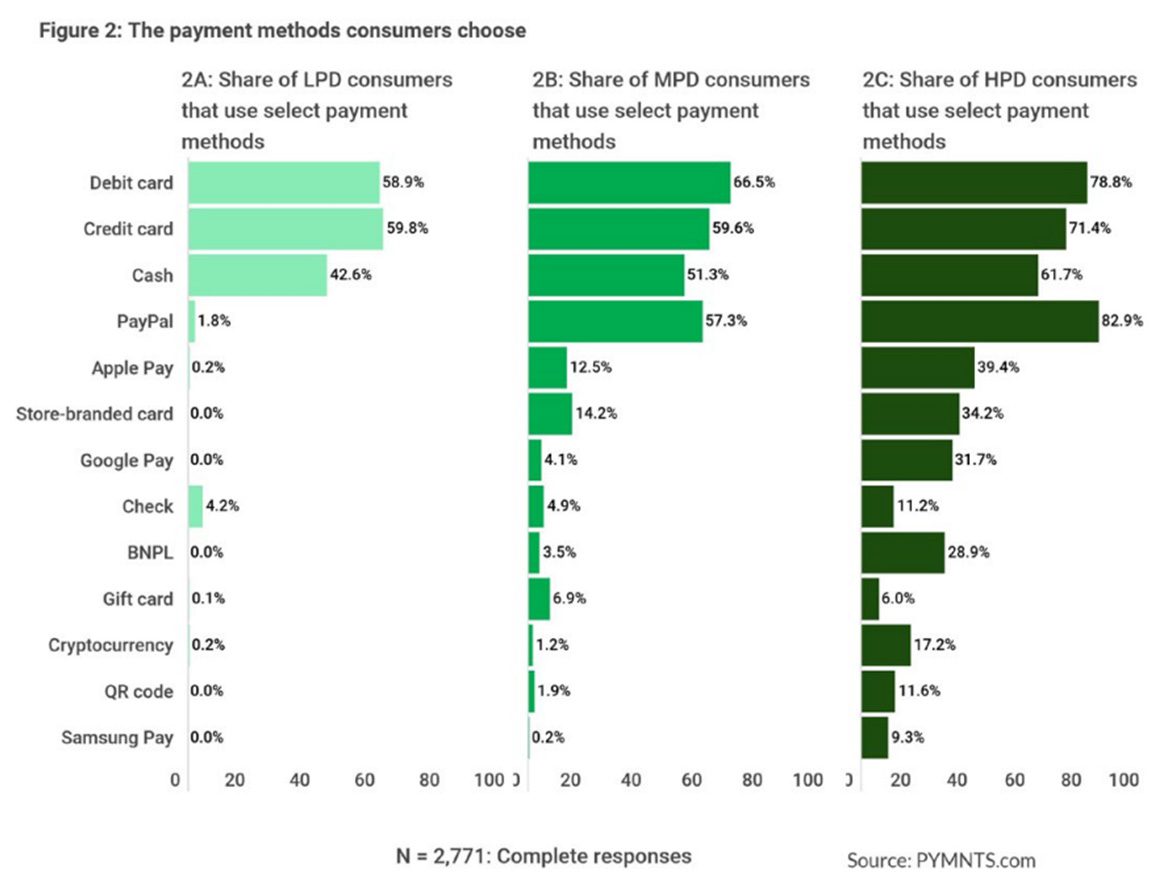

That sentiment is borne out by the recent findings of PYMNTS’ deep dive into the spending habits and preferences of more than 2,700 consumers in the United States last month. In the PYMNTS report: Digital Economy Payments U.S. Edition: Payment Method Diversification — June 2022, we found that debit edges credit, in some cases, significantly.

Read more: Digital Economy Payments: Payment Method Diversification

That preference cuts across all permutations of what we might call payments demographics — those consumers who show a broad or high range of payment diversification. These are the consumers who utilize at least three payment methods, with at least two of them classified as nontraditional methods, such as crypto.

The mild payments diversification segment uses at least two payment methods, and one of them can be classified as nontraditional.

Finally, there are the low payments diversification consumers, who use only a single method.

The chart below illustrates just how pervasive debit has become — where the payment method has been embraced by a majority (at more than 50%) of each of these segments.

The use of debit coincides with the fact that ours is a paycheck-to-paycheck economy. More than 60% of us have little to nothing left over after paying our bills each month. We contend that the juggling act of satisfying the monthly obligations becomes a bit fraught in the midst of 8.6% inflation. Given the fact that the payments diversification report centers on spending in-store and online on retail and groceries, it’s important to note that in the first category, the expenditures are at least somewhat discretionary; in the second case, they are staples of everyday existence. And yet debit cuts across it all.

That may be because debit spending is linked directly to one’s bank account; the bank account, of course, has a finite amount on hand (and is the likely destination of the household paycheck). Consumers are less likely to overextend themselves if they are mindful of what’s in the till and what can be spent.

Consider the fact that, in the highly-diversified payments group, 41% have annual incomes greater than $100,000, and 46% live paycheck to paycheck but still comfortably pay their bills each month. These consumers tend to be relatively younger, where the average age is 43, and the report’s overall sample’s average age is 48. Drill down a bit, and we see that buy now, pay later (BNPL) is actively used by this higher income, younger group, where almost 29% use BNPL.

At the same time, we see that 79% of these consumers use debit cards, and 83% use PayPal.

The stage is being set, then, for some significant cross-pollination. PayPal, of course (and any number of other players) has been making BNPL strides.

As reported in this space earlier in the month, PayPal has debuted PayPal Pay Monthly, a buy now, pay later (BNPL) offering issued by WebBank. The new offering lets customers space payments over a long period of time. Pay Monthly allows customers to choose between using their debit card or bank account for repayment and managing payments through the PayPal app and online. That cross-pollination has been in place for a while: In April, PayPal reported it logged $3.6 billion in volume in the first quarter, with 18 million customer accounts choosing this funding option since launch. In addition, 70% of those users engaged with BNPL using the company’s digital wallet.

Read Also: PayPal Launches Pay Monthly BNPL Offering

Macro headwinds abound – and debit, along with BNPL, may be clear-cut winners.