More than 74 million strong, millennials already account for nearly 3 in 10 consumer-spending dollars in the United States, and that share is projected to reach one-third by 2035. They are also digital natives with an analog memory. They’re old enough to remember life before the iPhone, young enough to have led the migration to mobile commerce, and now among the first consumers experimenting with artificial intelligence-assisted shopping.

That combination makes millennials a critical bellwether for banks, payment providers and merchants. Their financial lives remain pressured. PYMNTS data shows roughly 7 in 10 live paycheck to paycheck. But their economic influence is expanding. How they choose to pay today may therefore shape the products, rails and experiences that win as their spending power grows.

PYMNTS Intelligence’s forthcoming report, “The Millennial Consumer: How They Shop, Bank, Pay and Adopt Technology,” profiles U.S. consumers born roughly between 1981 and 1996. Publishing in full on June 23, the report draws on proprietary PYMNTS Intelligence surveys, including some tracked continuously since 2020. Findings are weighted to be nationally representative within each survey and span financial wellbeing, employment, income, shopping, payments, technology and AI adoption, and small business ownership.

The payments chapter reveals a cohort that readily adopts new options without abandoning familiar rails. Traditional banks still hold 61% of millennials’ primary checking relationships, while nearly 1 in 4 millennials use a digital-only bank or FinTech as their primary financial institution.

Their payment choices are similarly blended. Debit and credit cards remain the foundation, while wallets, FinTech apps and buy now, pay later (BNPL) expand the range of ways they can transact.

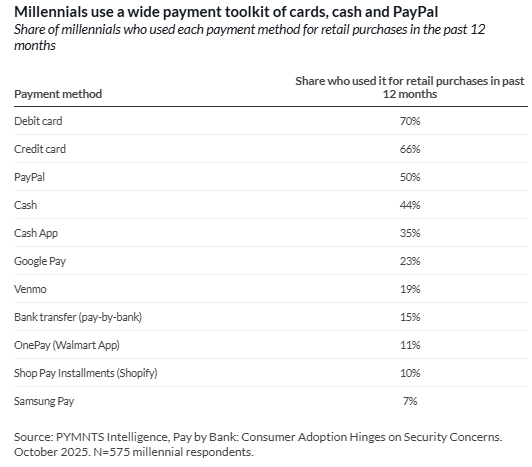

Key findings from the payments section include:

- Cards still anchor the millennial wallet, as 70% of millennials used a debit card for retail purchases in the 12 months before being surveyed, while 66% used a credit card. PayPal reached 50%, cash 44% and Cash App 35%. At the same time, 17% of millennials have no general-purpose credit card, underscoring that access and product fit remain uneven across the cohort.

- Digital adoption is broad, but habit still governs checkout. In stores, debit funded 43% to 47% of millennial transactions, and credit funded another 25% to 27%. Only 11% to 15% used Apple Pay for their most recent in-store purchase, while 27% to 29% were eligible to use it but did not. The barrier is less about device availability than routine, merchant prompting and the path of least resistance at the point of sale.

- Flexibility, immediacy and value drive emerging behavior. Monthly BNPL use ranged from 19% to 23% in early 2026, increasingly spanning both essential and discretionary purchases. When millennials could choose how to receive a disbursement, 56% selected instant receipt, even when a fee applied. On their most recent shopping trip, 3 in 4 used at least one embedded offer, showing how strongly speed and savings can influence payment choice.

Taken together, the data does not describe a cashless or wallet-first generation. It describes an option-rich generation that chooses the rail best suited to the moment. They use debit for control, credit for reach, wallets for convenience, BNPL for cash flow management and instant payments for access to funds.

For issuers, banks, FinTechs and merchants, winning millennial payments volume will depend less on forcing a single preferred method and more on making multiple methods easy to discover, trust and use. The providers that pair flexibility with immediate, visible value could be best positioned to capture this generation’s growing economic power.

“The Millennial Consumer: How They Shop, Bank, Pay and Adopt Technology” publishes in full on June 23. Subscribe to the PYMNTS Today newsletter to receive the report at launch and stay current on the data reshaping payments and digital commerce.

At PYMNTS Intelligence, we work with businesses to uncover insights that fuel intelligent, data-driven discussions on changing customer expectations, a more connected economy and the strategic shifts necessary to achieve outcomes. With rigorous research methodologies and unwavering commitment to objective quality, we offer trusted data to grow your business. As our partner, you’ll have access to our diverse team of PhDs, researchers, data analysts, number crunchers, subject matter veterans and editorial experts.