Payment software company Abrantix announced news that it has partnered with UL to launch the UL Brand Test Robot for a quicker and more efficient way to automate payment terminal brand certification testing.

Testing payment terminals is usually a manual and repetitive process that involves a considerable amount of time pressing buttons, entering pins and inserting cards. Not only is it time-consuming, but there is also a risk for human error.

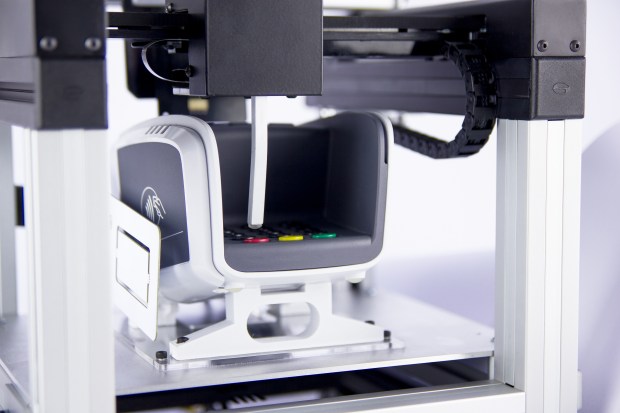

With the Abrantix AX robot performing the test operator’s work, the UL Brand Test Tool boosts efficiency, saves a considerable amount of testing time and minimizes the need for human intervention.

“We are very pleased with this successful product in the market nowadays, and the integration with the Abrantix AX robot solution will reinforce its positioning and current list of features by adding innovative automation capabilities,” said Henrique Di Lorenzo Pires, global products director in UL’s transaction security division.

The UL Brand Test Robot can enable acquirers, acquirer processors, merchants and terminal vendors to execute a high volume of repetitive payment terminal tests, ensuring the process is more efficient while maintaining the required levels of quality and accuracy. In addition, it works for terminal manufacturers and payment acquirers who may want to “stress” their payment acceptance devices by performing a high number of unattended transactions to prove the durability of the terminal software.

‘‘We had an amazing collaboration with UL,” said Daniel Eckstein, CEO at Abrantix. “We tightly integrated the UL BTT with the AX Robot. This gives our customers the ability to fully automate EFT/POS terminal testing, either for certification or regression testing.”