Why Retailers Should Worry About Inflation but Dread the Wealth Effect

A new survey of U.S. consumers, hot off the presses at PYMNTS, tells a lot about how they’re handling the current economic turmoil and when they think it will end. It’s important information for any business or policymaker trying to navigate through the next couple of years.

Let me begin by playing armchair economist to put the findings in perspective before I spill the beans.

Economists have long studied the impact of macroeconomic news on consumer spending, and most agree there is one. Even marginal positive news about unemployment rates can boost consumer spending — with visible, long-lasting effects. Conversely, bad news about unemployment rates has been found to reduce consumer spending by 1.5% — including by consumers who have jobs and are unaffected directly by the news.

In 2022, the economic news impacting all consumers today isn’t unemployment rates, which are at historic lows, but the impact of historically high inflation rates — and the continued stock market and housing market volatility — on their real and perceived financial well-being.

Inflation robs all consumers of their purchasing power, unless their wages have kept pace, and influences decisions and tradeoffs about what they’ll buy and from whom. The majority of consumers have lost a lot of purchasing power over the last year. Unfortunately, those least equipped to handle it — lower income and paycheck to paycheck consumers — have been hit hardest of all.

But it’s the wealth effect that is the more important determinant of whether consumers with money to spend will actually open their digital wallets and spend it.

That’s particularly true for high earners — they have probably had the greatest proportion of wealth destroyed, in part by the massive drop in stock prices, and they could be hit more if the continued decrease in housing demand sends housing prices south.

Because high earners account for so much of the retail economy, their pull-back in spending could be the most damaging to it.

Not Feeling That Flush

Studies show that consumer spending increases 2.8 cents for every dollar of increased stock market wealth.

A March 2006 speech given by then Fed Vice Chair Roger Ferguson reported Fed data showing a 3.5-cent loss in spending power for every dollar of wealth destruction felt by consumers, with half of that spending pull-back felt in the short term.

The downside impact to the economy is more severe when consumers feel shaky about their financial situation than the upside when they are feeling flush. Consumers don’t feel comfortable spending money until they have confidence that they can replenish what’s been lost. The longer that takes, the more constrained consumers may feel about spending money.

In July of 2022, the majority of U.S. consumers don’t feel that flush.

That’s despite a collective $33 trillion increase in their household net worth between 2019 and 2021 and the strongest consumer balance sheet in decades.

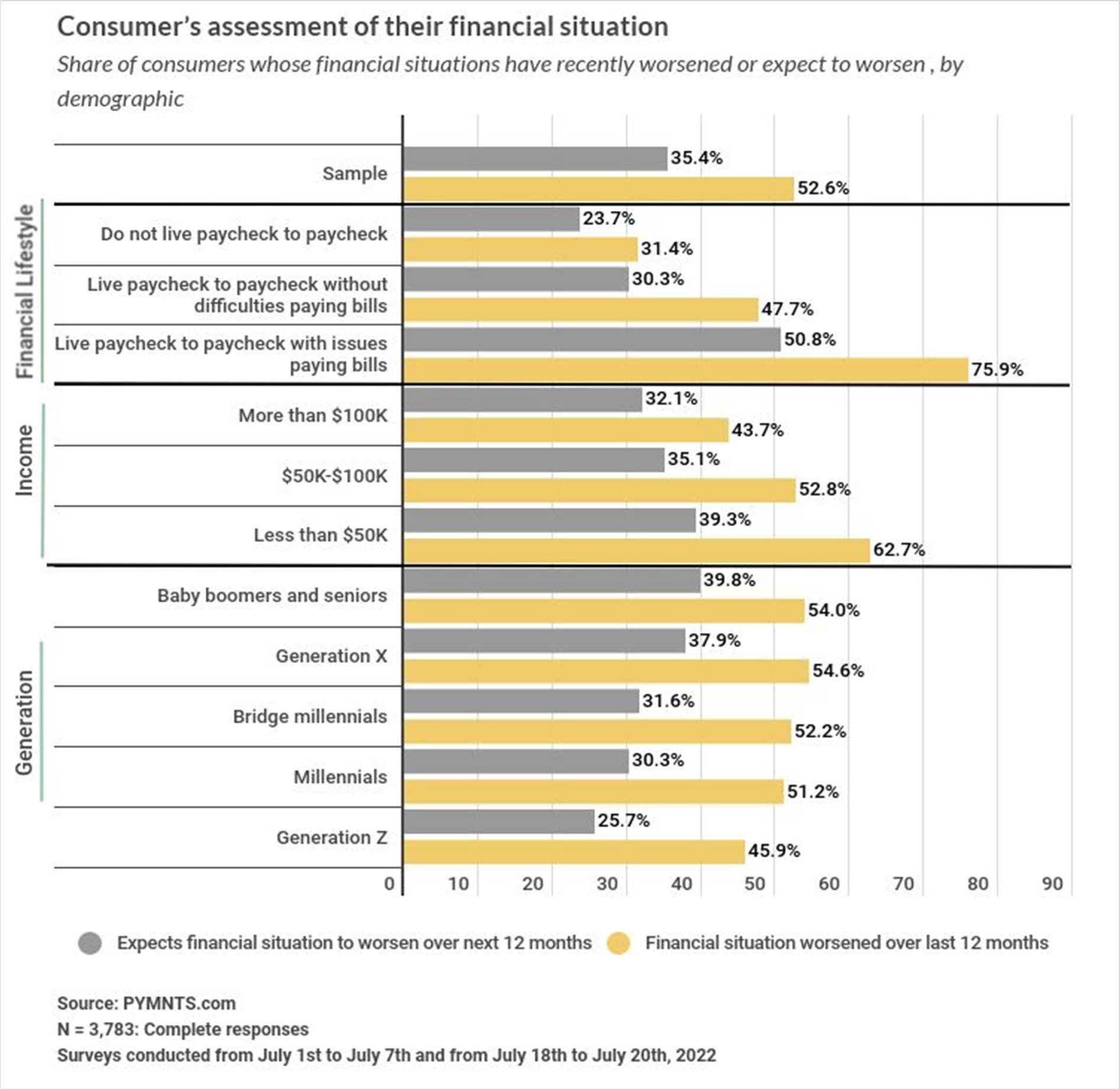

More than half (53%) of consumers say their financial condition is worse in 2022 than it was in 2021. Nearly a third believe it will deteriorate over the next 12 months.

That’s according to a national online study of 3,783 consumers conducted by PYMNTS in July 2022 (July 1-7, July 17-20).

Nearly 8 in 10 of those living paycheck to paycheck with issues paying their bills say they’ve seen their financial situation worsen over the last year, and half expect it to erode further.

Forty-four (44%) percent of those earning more than $100k report they are worse off today than a year ago. A third of those high earners believe their financial situation will deteriorate in the year to come.

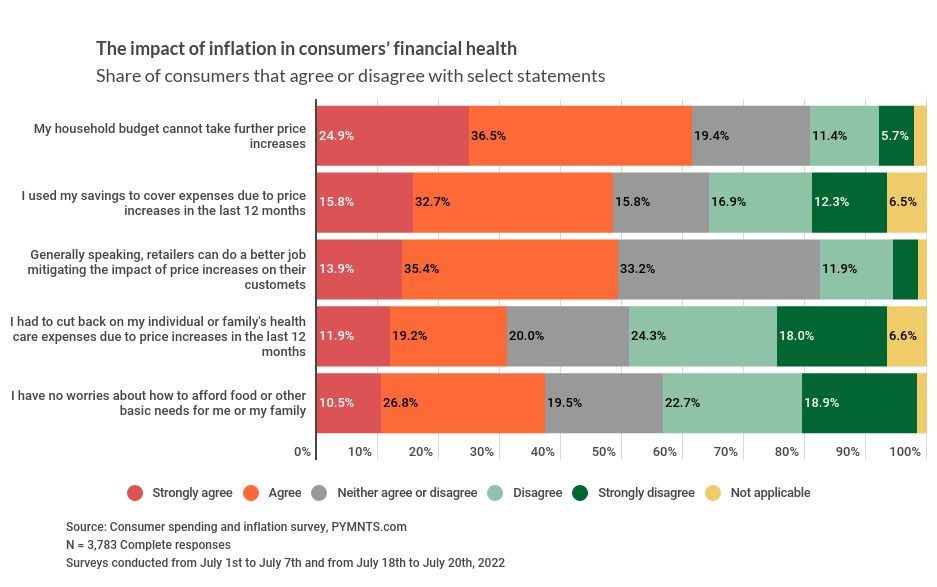

Inflation is part of what’s driving that sentiment. Few will argue that inflation is clipping the wings of consumer spending — now and for the foreseeable future. According to our data, half of all consumers report that high inflation has caused them to dip into savings to cover expenses that their paychecks once covered — millennials most of all. Pay may be rising, but not enough to cover the higher cost of living.

Also driving that sentiment is the sinking feeling that consumers get when they are brave enough to check their investment account balances — which many consumers now have, especially those with higher incomes.

In June of 2022, the St. Louis Fed reported the first decline in household net worth in two years. The collective $3 trillion decline in stock market value swamped the $1.7 trillion collective increase in the value of their homes.

Some dismal scientists worry that future stock market and housing market instability at the levels experienced in the first half of 2022 could further weaken those household balance sheets and dent GDP growth. Why? Because consumers may not spend — even those with money in their accounts who could spend — unless they feel confident that their financial situation is secure.

Boomers, with lots of money to spend, may pump the brakes the hardest. In fact, the June Fed data also finds consumer checking and savings account balances increasing as consumers appear to keep, not spend, the money they have.

Feeling the Inflation Heat

Of course, this news comes at the same time that inflation at levels not seen in 41 years is chipping away at the consumer’s overall purchasing power.

The Bureau of Labor Statistics (BLS) reports inflation rates in June hovering at 9.1%, with average wages for U.S. workers increasing 4.9% over the last 12 months.

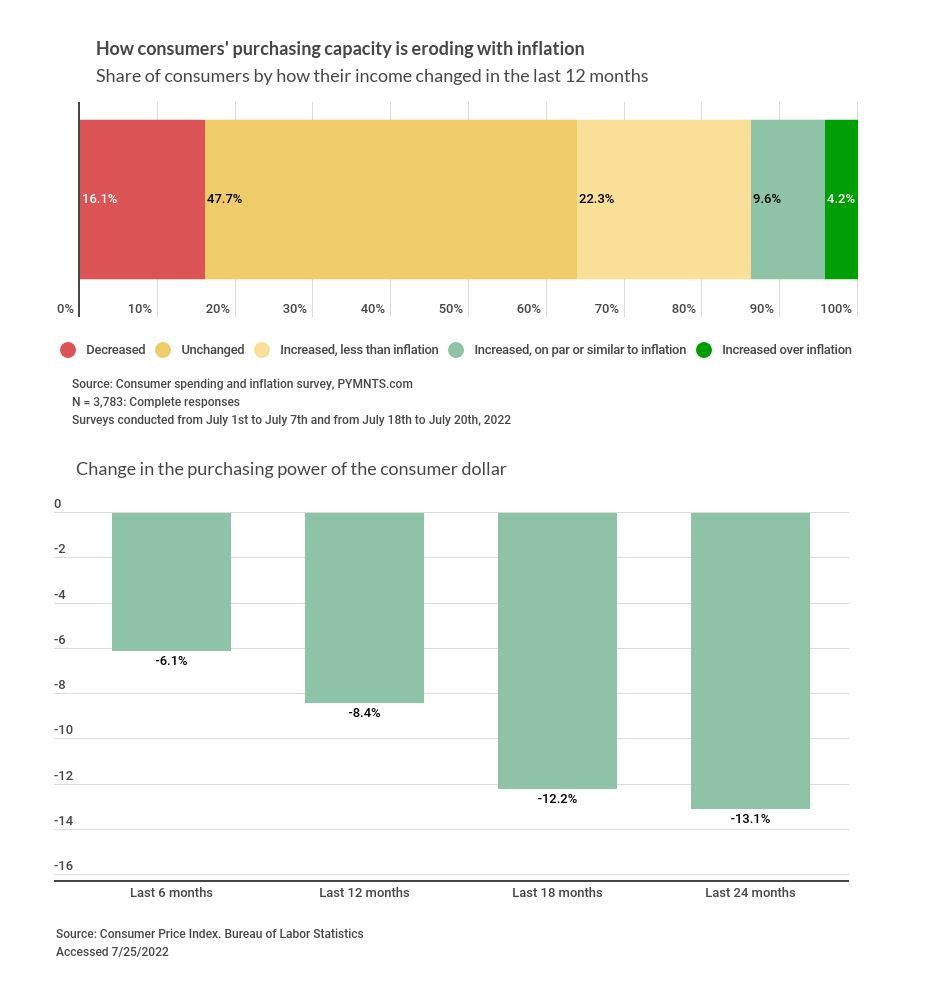

Inflation has robbed consumers of 8.4% of their spending power, on average, over the last year. This figure considers the variation in the purchasing power of the U.S. consumer across cities, as measured by BLS. It now takes about $109 now to buy the same basket of groceries consumers purchased for $100 last year.

For some people, that extra $8 or $9 may not be a big deal. But it comes on top of lots of other $8 or $9 increases — including what it now costs just to pay for the basics.

PYMNTS data shows that more than half (53%) of consumers say that interest rates on their credit card balances have increased, and 60% report spending more to pay their mortgage or rent and for household maintenance. Eight in ten consumers report higher utility and transportation costs (car payments, maintenance, public transportation). Nearly everyone (90.1%) has felt the pain at the pump.

All of that influences the consumer’s perception of how much she actually spends at retail and grocery stores. PYMNTS data finds that consumers say they pay 20% to 30% more for retail and grocery purchases and to eat at restaurants, even as published BLS data reports an increase of 5% to 15% in those same categories.

For the average consumer, reality is not shaped by how much the government tells them things cost, it’s shaped by their personal reality when they go shopping and pay their bills.

Maxing Out

Unsurprisingly, nearly two thirds (62%) of Americans report maxing out their household budgets, including a fifth of high earners. Millennials are most negatively impacted. Nearly everyone — 80% to 90% of all consumers — reports taking at least one step to adjust their spending levels.

Seventy percent (70%) of retail shoppers say they’re cutting back on purchases they don’t consider essential, including 87% of consumers earning over $100,000. Few consumers say they’ll compromise quality to save money — instead, they will reconsider whether a purchase is necessary at that time.

Seventy-one percent (71%) of consumers say they’re eating at home more often. That includes two thirds of consumers earning over $100,000 and those not living paycheck to paycheck. These are two groups who presumably have discretionary money to spend, but they aren’t spending it at restaurants right now the way they once did.

More than half of retail shoppers (52.6%) look at competitors to their favorite merchants to find cheaper prices on the items they want to buy, including one in five high earners. Forty-five percent (45%) of consumers say they’ll shop other grocery stores for better prices on the things they want to buy, too, including nearly 20 percent of those with incomes over $100,000 per year.

The 653-Day March to Lower Inflation

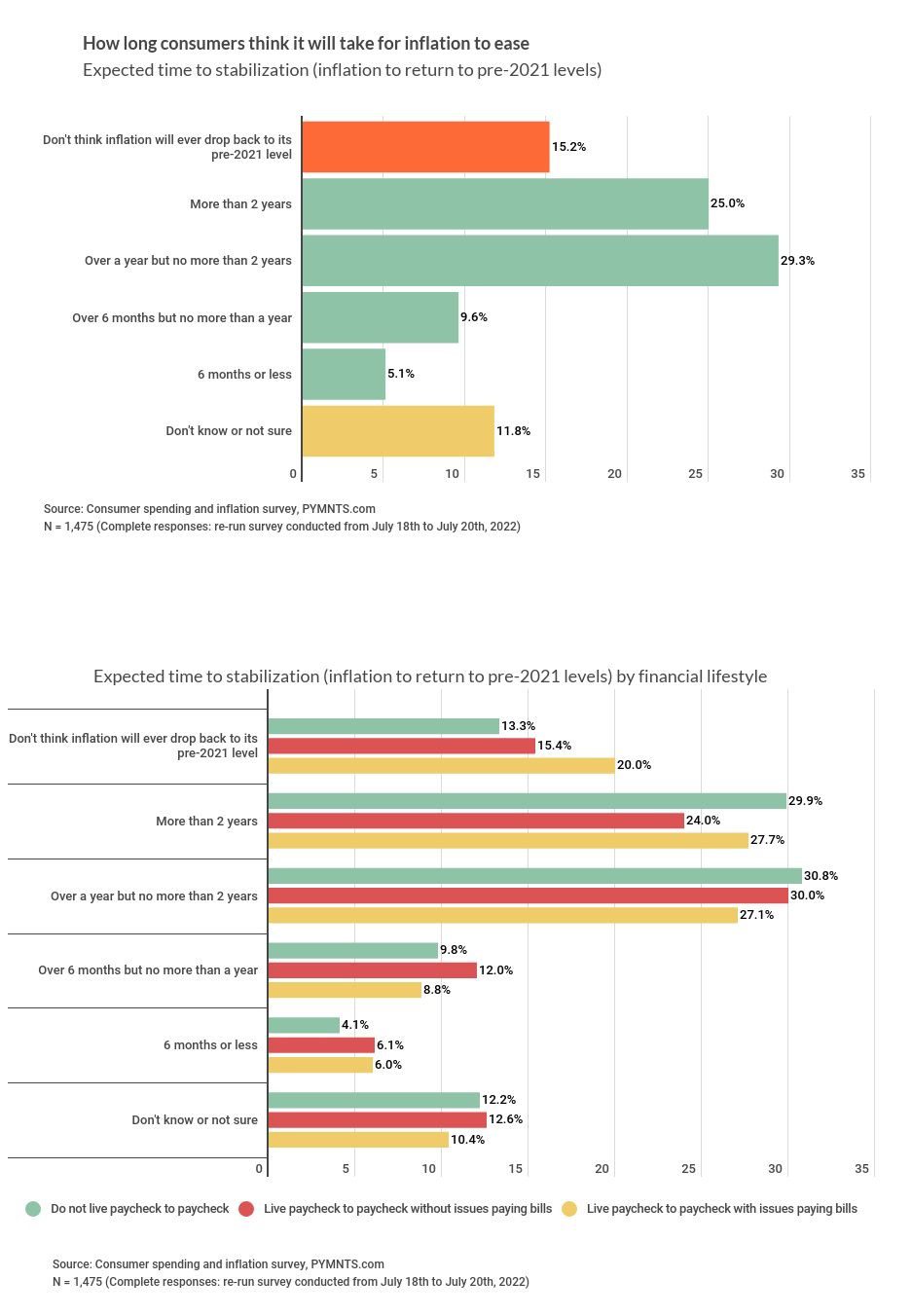

Consumers also think they’ll be living with higher prices for a while. Specifically, they estimated 653 days longer from the day they responded to the survey.

Which means they’ll likely continue to make their own adjustments for some time to come.

On average, consumers say it will take until Q2 2024 for inflation to return to the level it was in 2020, which averaged 2%. Higher earners expect high levels of inflation to persist until mid-April 2024.

PYMNTS research finds that the number of consumers who believe that it will take at least a year or more for inflation to return to that 2% is three times as high as the number who believe things will return to those levels by the end of the 2022.

What’s Next

When I saw these data, three thoughts crossed my mind.

The first is how the current macroeconomic environment is becoming the great consumer spending equalizer.

The double hit of the decline in financial wealth from stock market volatility and the high levels of inflation are causing nearly all consumers, regardless of demographic group or income, to adjust their spending. It isn’t only about whether consumers have money to spend, it’s whether they will spend the money they have — and where. When high earners tighten their purse strings, the ripple effect across the economy will be felt.

The second is how remarkably accurate consumers were at predicting the duration of COVID, and whether the same will be true for their predictions about inflation’s persistence.

On March 4th of 2020, PYMNTS fielded the first of our monthly COVID studies asking consumers a number of things about their physical and digital shopping behaviors. We also asked when they thought COVID would end. At that point, there were a very small number of COVID cases in the U.S., and we were still a few weeks away from a national lockdown.

Even then, consumers started ramping up their digital activities and throttling back their physical interactions. Consumers in our first study said it wouldn’t be until the Fall of 2020 before things would return to normal; experts and the media predicted that a return lockdowns and reopening would take two months. Every month we fielded the study, consumers extended that deadline, giving predictions about the duration of COVID that turned out to be pretty accurate in retrospect.

If they are right on inflation, we won’t be back to normal until more than a year from now — maybe two, given what they know now. Their spending behaviors will almost certainly mirror those views.

Finally, it’s often the most challenging times that surface the most creative solutions. This one is tailor-made to help consumers make smart decisions about how to spend their money and navigate the difficult times ahead. Most consumers we studied think that retailers and payments players can do more to help them.

I guess that’s as close to a call to action as you can get.

So, for everyone across the payments, retail and financial services ecosystems, now is your time to shine. Just as so many of you did during the pandemic to help consumers make it through to the other side, stronger, healthier and more digitally savvy.