More consumers are shifting to online shopping and adopting digital payment methods for in-store purchases the longer the pandemic continues — a trend that could have a significant impact on how payments take shape in the future. Consumers are also tapping peer-to-peer (P2P) apps and other types of mobile wallets for a growing list of use cases, with expectations of seeing these methods supported by their favorite retailers and offered by their financial institutions (FIs). This follows preexisting trends as most consumers already tie their mobile wallets to their preferred debit or credit cards.

Card-not-present (CNP) transactions made up 27 percent of all debit payments by the end of 2019, according to a recent report by interbank electronic funds transfer network PULSE, for example. Account-to-account (A2A) transfers, which include P2P payments, were also the leading use case for growth in debit payment volume at the end of that year. Consumers’ comfort and familiarity with mobile P2P transactions has ramped up during the global health crisis, following their rise in availability. Sixty-seven percent of FIs offered mobile P2P payment services in 2019, according to one recent study, while 26 percent of banks said they would offer them by the end of 2021.

How P2P app use has shifted during the pandemic and how this may impact what consumers are seeking from their payment experiences could prove critical for the merchants and banks expected to meet these needs. The following Deep Dive takes a close look at why A2A transfers have grown so popular among consumers, the role debit plays in this space and how the pandemic has accelerated or otherwise impacted this shift.

The Pandemic’s P2P Payment Push

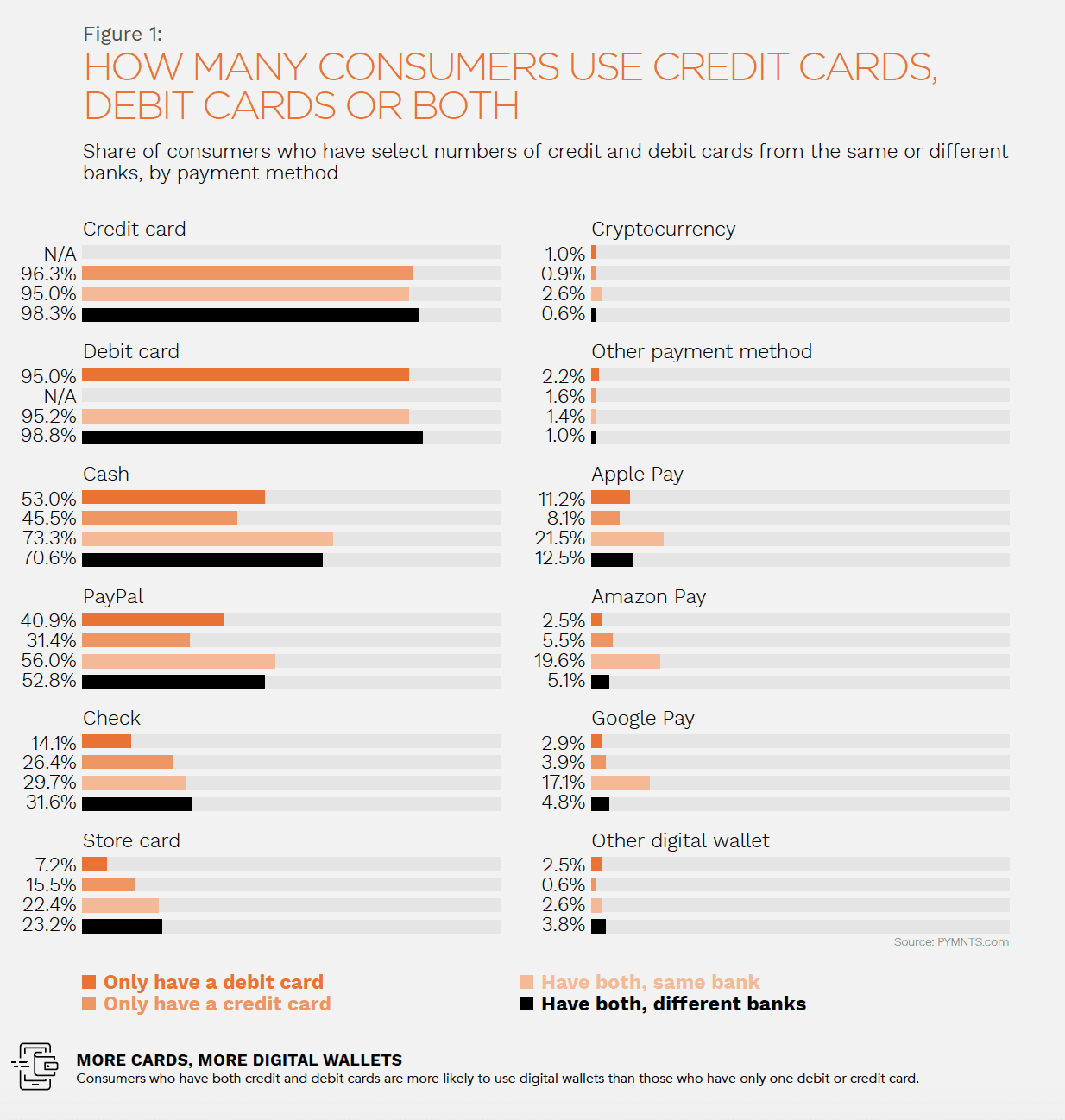

P2P payments are far from new, though reasons why consumers may choose to use these digital wallets can vary. Consumers are especially likely to make the jump to P2P when they use the same bank for all their cards, indicating that trust in their FIs plays a key role in this trend. One recent PYMNTS study showed that cardholders who have both their credit and debit cards with the same bank are more likely to use digital wallets. Nearly 22 percent of consumers whose cards are issued by the same FI use Apple Pay, for example, compared to the 13 percent of individuals with cards from different banks.

Debit’s relationship with P2P has continued strongly through the pandemic, too. According to this same PYMNTS study, approximately 41 percent of PayPal users have only debit cards and no credit cards, for example. These users may not necessarily be connecting their PayPal accounts to their debit cards as they can still connect directly to their bank accounts, but it does imply that P2P apps and debit are strongly linked. This suggests that consumers may think of their P2P apps as extensions of their debit cards. This is crucial for FIs as well as merchants to consider as the pandemic pushes P2P use outside of individualized payments and more into the traditional retail sector.

Debit’s relationship with P2P has continued strongly through the pandemic, too. According to this same PYMNTS study, approximately 41 percent of PayPal users have only debit cards and no credit cards, for example. These users may not necessarily be connecting their PayPal accounts to their debit cards as they can still connect directly to their bank accounts, but it does imply that P2P apps and debit are strongly linked. This suggests that consumers may think of their P2P apps as extensions of their debit cards. This is crucial for FIs as well as merchants to consider as the pandemic pushes P2P use outside of individualized payments and more into the traditional retail sector.

Consumers are using contactless payments, including those made via mobile payment apps and tap-to-pay contactless cards, more often when they shop in brick-and-mortar stores. Sixty percent of consumers now want to use touchless payments at point-of-sale (POS) terminals in stores, according to recent PYMNTS data. Another PYMNTS study found that 51 percent of consumers make both virtual and in-store purchases with mobile wallets, indicating that consumers may be associating contactless with their mobile phones more than with their plastic cards.

Individuals are expecting to pay with their chosen wallets regardless of channel, device or use case, and this is occurring as P2P use becomes increasingly ubiquitous among consumers. One other study found that 71 percent of American adults are now using P2P apps.

Debit In The Next-Gen Cardless World

Consumers are not giving up their debit cards in favor of P2P apps despite the latter’s growth in popularity, however. Debit is becoming one of the top choices when consumers go to pay through connected devices, whether that involves paying merchants in stores, paying friends through their mobile devices or making utility bill payments through other smart devices in the home. Nearly 46 percent of U.S. consumers in one recent PYMNTS study said they prefer to use debit cards to power their “connected experiences,” including mobile and contactless payments or those made through smart speakers.

This indicates that debit will continue to play a key role in the next-gen payments space following the impacts wrought by the ongoing pandemic. It is important for FIs and merchants that are looking to successfully compete for consumers’ engagement and attention to consider how and why P2P payments have become so important — and why they are not going away.