Tick. Tock.

Or to quote a bit of T.S. Eliot — hurry up, please, it’s time.

For special purpose acquisition companies (SPACs), raising cash the past few years has been easy. The hard part has always been getting the deal done — now, more so than ever.

And for those that don’t get the deal done, the great unwinding looms. And for many payments companies, indications are, it’s already begun.

By way of example, Bloomberg reported on Tuesday (Aug. 16) that some SPACs have been pushing back investment deadlines. Typically, the horizon has stretched over two years: If that period comes and goes, investors can opt to redeem their shares, take their money, and effectively go home.

Bill Ackman’s Tontine Holdings, with $4 billion in hand, liquidated earlier this year, a high-profile case of what might happen to the SPAC industry at large.

In illumination of the pressures, Bloomberg reported that two SPACs launched by Chamath Palihapitiya have, through filings with the Securities and Exchange Commission (SEC), been moving the goalposts a bit (those are our words) by resetting their acquisition deadlines to 2023.

“Inking a deal will likely be no easier in 2023, assuming that investors in the SPAC even opt to stick around,” noted Bloomberg.

Reining in the Projections

And the pressure seems to be building a bit, at least in terms of the projections made in the very SEC filings that launch the SPACs in the first place. Those projections had gone largely unchecked all through the halcyon days of those investment vehicles.

And now, 600 blank check firms will be hitting their deadlines over the next (roughly) year and a half, as Bloomberg has noted. It turns out, in this market environment, investors may be more skittish than ever to tie up their cash for two years in the hopes that an attractive merger candidate will come along — and cash in hand offers those same would-be investors a surety that SPAC deals emphatically don’t. After all, there’s no guarantee that the listings will not trade below the initial pricing.

See also: FinTechs Choose ‘Traditional’ IPOs, Shun SPACs, Amid Muted Listings

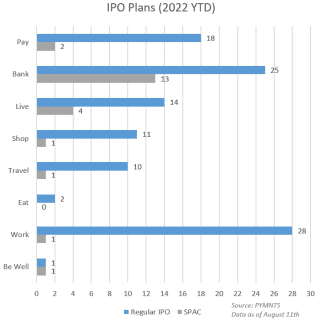

To get a sense of just how anemic SPAC activity has been in the payments space, consider the chart. As tracked by PYMNTS, the IPO “plans” by segment — that is, the announcements of SPACs formed to find targets within financial services and related technologies — has dripped and drabbed to a listing here, a listing there (and none in the “Eat” segment).

Traditional IPOs have been the listing route of choice, possibly because they are not under the same scrutiny as SPACs are and have what we might term an “implicit blessing.” There’s an old saying on Wall Street that states “don’t fight the tape,” and we’d amend that here to state: Don’t fight the SEC. The SPAC may, eventually, go the way of the dodo, an investment bird of a certain feather that we realize was a bad idea to go hunting for.

In hindsight.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More