The earnings are out, the early moves are made and the race for the consumer’s whole paycheck in 2020 is officially underway and moving full speed ahead.

Thus far the advantage seems to be tipping toward Amazon, which got out of the gate with a stronger than expected earnings showing, one-day shipping yielding dividends, 150 million prime members and series of expansions, introductions and leaps outward as it seeks to stake out a larger share of average American consumers.

Walmart’s start to 2020 has been a bit bumpier. After eight consecutive earnings beats, a slower than expected holiday season caused Walmart’s first miss on expectations in two years.

“Walmart’s results show it’s a food fight out there, with Amazon re-accelerating holiday sales growth,” Evercore Analyst Greg Melich said on Feb. 18.

Walmart is apparently working hard at restructuring itself to win, particularly in regards to how it manages it growing its eCommerce business — operationally and logistically.

The firm is also, it seems, interested in changing the consumer-facing front end, as news broke late last week that Walmart will soon be launching Walmart+ — a membership program designed to be a direct competitor to Amazon Prime.

The anecdotal field has been rich in the first two months of the year, as both Walmart and Amazon are clearly committed both consolidating their current positions on the field while also finding ways to make inroads into new ground — or take back ground from the other. But how does it look by the numbers?

PYMNTS follows that question monthly to keep quantitative track of the race for the consumer’s whole paycheck. So where are the areas of relative strength — and where are the rising battlegrounds?

Amazon vs. Walmart, the Overview

The typical American household spends $65,960 per year, the largest share of which goes toward retail spending — 30.8 percent, or a little over $20,000 a year. Other leading categories are housing and utilities, which captures 18.5 percent of consumer spending, and healthcare with 16.9 percent. Restaurants, financial services, personal services, insurance, telecom and entertainment/recreation round out the rest of the top consumer spending categories.

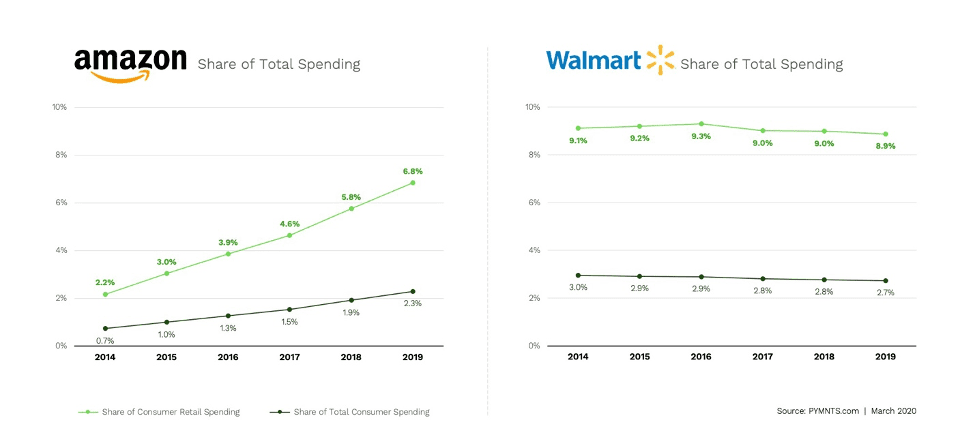

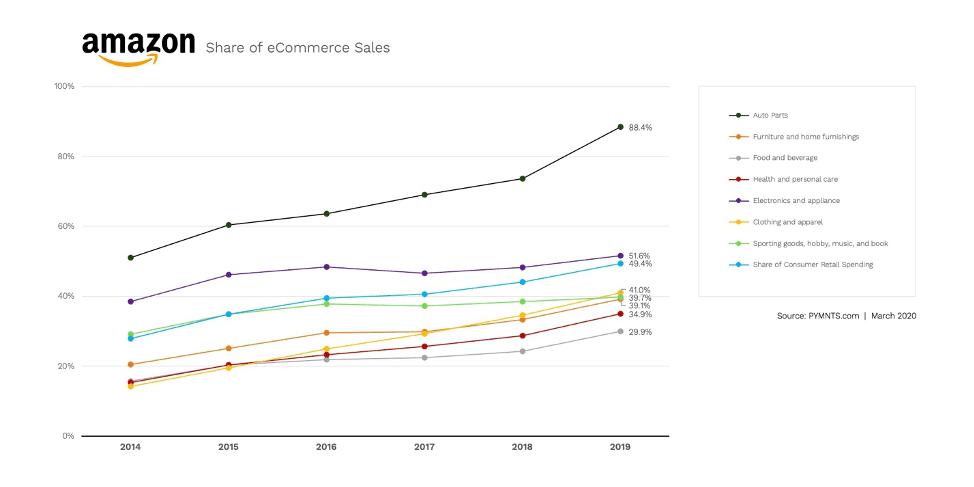

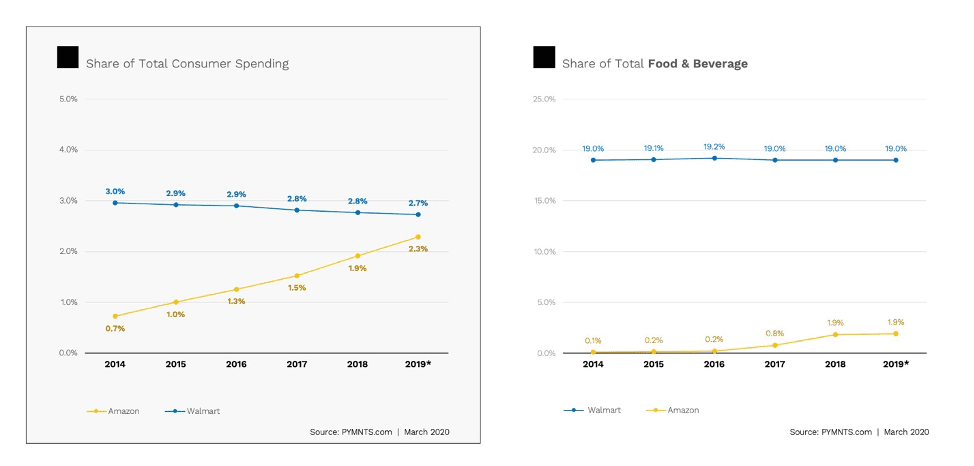

Taken as a total, sales on Amazon constitute 2.3 percent of total consumer spending, 6.8 percent of total consumer retail sales as of 2019 and nearly half (49.4 percent) of all U.S. eCommerce retail sales.

All of which represents a massive growth story for Amazon over the last half decade, when Amazon’s share of consumer retail spending was 2.2 percent and its share of total consumer spending was 0.7 percent. That big jump in market share is explained by the massive uptick in sales on Amazon in the last five years. In 2014, Amazon’s U.S. gross retail sales were $86 billion. By the end of last year, that had grown to $339 billion. During the same time period, Amazon’s eCommerce retail sales have grown from $83 billion to $294 billion. That pencils out to cumulative annual growth rate for total sales and eCommerce sales of 31.5 percent and 30.1 percent respectively.

Walmart’s story is a bit different. Taken as a total, Walmart accounted for 2.7 percent of total consumer spending and 8.9 percent of consumer retail spending and (according to PYMNTS estimates, as Walmart does not report this data directly) 4.6 percent of eCommerce sales.

And while Walmart remains leading the race — by a nose when it comes to total spending — its growth has been markedly flatter than Amazon’s. Walmart’s gross sales are up — by a much less steep amount — growing from $349 billion to $403 billion last year. eCommerce sales, based on our estimates, came in around $27.8 billion, roughly doubling the 14 billion they brought in in 2017.

And most notably, Walmart’s market share is heading in the wrong direction, despite the fact that its sales are growing. In 2014 Walmart controlled roughly 9.1 percent of consumer retail spending, and 3 percent of total consumer spend — meaning it’s not losing ground quickly, but it is steadily losing ground every year.

Strengths and Weaknesses

While Walmart has lost ground in a lot of areas (more on that in a second) food and beverage — more specifically grocery — has been its fortress, one that Amazon has found nearly impregnable thus far. Walmart as of the start of 2020 has 19 percent of the food and beverage sales market, a category that on its own accounts for roughly 8 percent of household retail spending annually. That is the same market share it has held since 2014.

And for Walmart, grocery is more than just a stabilizer for its hold on the consumer’s whole paycheck, it is also the power source behind its burgeoning eCommerce program — as buy online, pick up curbside has been, by Walmart CEO Doug McMillon’s own admission, the main driver of the retailer’s eCommerce growth over the last several years.

“Our strength is being driven by food, which is good, but we need even more progress on Walmart.com with general merchandise,” McMillon noted to investors during the firm’s last earnings call.

Amazon, despite its nearly $14 billion acquisition of Whole Foods Market in 2017, has struggled to move the needle when it comes to radically upping its share of the food and beverage market, having only increased its market share in the segment from 0.1 percent in 2014 to 1.9 percent in 2019.

But Amazon is nothing if not persistent. Apart from expanding free Prime Delivery from Whole Foods locations, and folding Amazon Fresh into the standard Prime offering (for those who live within range), in the last week Amazon has both opened a traditional grocery store in LA and a new cashierless offering in its Seattle hometown.

A long way of noting, stay tuned, as it remains to be seen how long grocery can remain a fortress for Walmart.

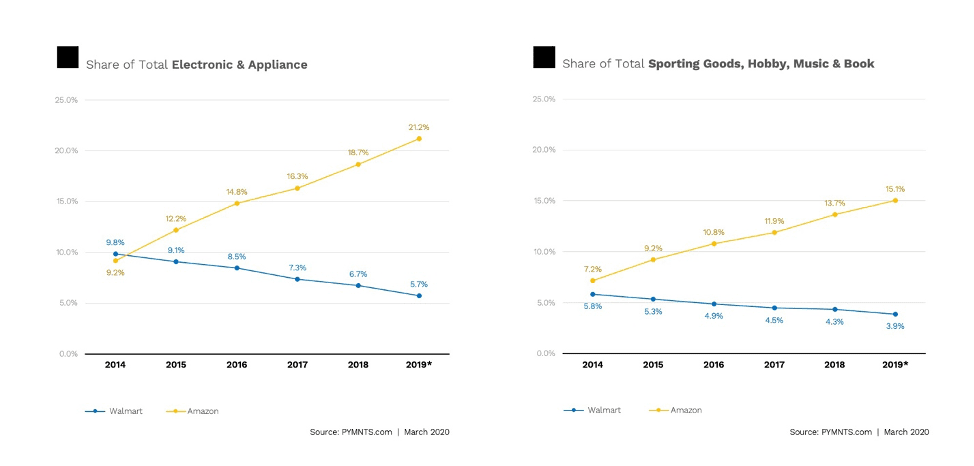

Meanwhile, Amazon’s areas of strength are growing. According to PYMNTS data, Amazon now dominates in electronics and appliances and is just consolidating its strength, with approximately 21 percent of the market to Walmart’s 5.7 percent. A similar story is emerging in sporting goods, hobbies, music and books — where Amazon holds 15.1 percent of the market to Walmart’s 3.9 percent.

And there is, of course, Amazon’s wholesale eCommerce dominance — but with 50 percent of that total market Amazon isn’t so much a problem for Walmart as it is for everyone who wants to conduct commerce online.

The Battlegrounds

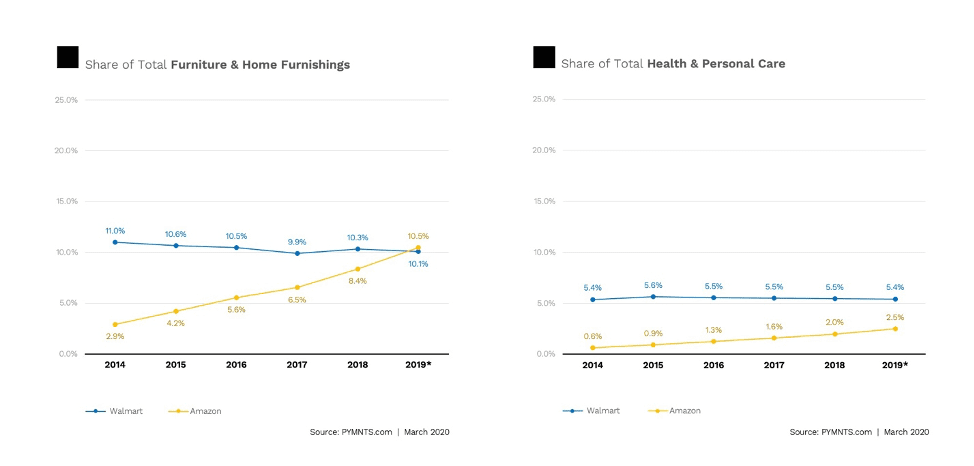

There are also categories where Amazon has a lead, but that lead is more recently taken. As of the start of 2020, Amazon has finally fully snagged the advantage in clothing and apparel from Walmart since the line first crossed in 2017. Amazon now has 9.5 percent of that vertical to Walmart’s 6.9 percent. In home furnishings and furniture, Amazon has 10.5 percent of the market to Walmart’s 10.1 percent.

And it seems that while the margin is still slim enough, and Amazon’s lead is still relatively new, Walmart is not willing to go down without a fight. McMillion said last week Walmart intends to push more aggressively into selling home goods and clothing.

“We’ve invested a lot to do it, but we’re now in a position to play offense in an omnichannel game,” McMillon told analysts as well as investors. “We’ve got a strong set of chess pieces to work with.”

The other emerging battleground area to stay focused on is health and personal care. This is still an area where Walmart is holding a commanding lead, buttressed by its long presence in the space, with 5.4 percent of the market. But Amazon has been closing the gap rapidly, particularly since 2016. As of 2014, Walmart controlled the exact same share of the market that it does today — 5.4 percent. Amazon, on the other hand, has grown from 0.6 percent of the health and personal care market in 2014 to 2.5 percent of the market in 2019.

And both players seem to be avidly interested in moving on the space — Amazon with its PillPack acquisition and push into prescription drugs , and the virtual health clinics it started piloting with its employees in Seattle last week.

But Walmart has been battling back — with experimental full service health centers opening late last year, and more recently by offering health insurance through Sam’s Club.

It seems clear that both Walmart and Amazon are eying the $3.6 trillion opportunity that is U.S. healthcare spending and trying to figure out how to capture a larger slice of it. Walmart has a lead, but as the last five years have demonstrated, a lead can be a hard thing to hold when Amazon starts targeting a market.

Hard, but not impossible — and Walmart is clearly not ready to give up any more ground than it already has without a fight.

A fight we will keep you updated on, with the news items and the data standing behind all of it.