The buy now, pay later (BNPL) market is skyrocketing, fueled by both increasing consumer awareness and aversion to high interest rates, particularly among younger generations. Recent PYMNTS research found that consumers’ enthusiasm for BNPL continues to grow regardless of channel. Shoppers across both physical and online environments evidence similar interest in BNPL, and the main factor that appears to inhibit BNPL use in physical retail is the lack of BNPL as an option.

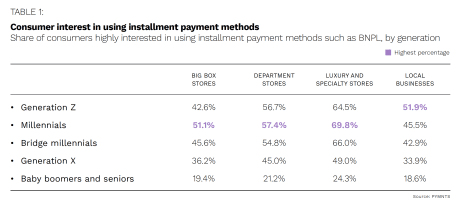

Among surveyed department store shoppers, for example, 46% said they are highly interested in using BNPL online, while 41% are interested in using BNPL in-store. BNPL’s appeal is greatest among millennials, 70% of whom said they are highly interested in using installment plans at luxury and specialty retailers, with approximately two-thirds of bridge millennials and Generation Z consumers saying the same.

Interest in BNPL is not limited to the young or to those concerned about debt, however. As its popularity rises, BNPL increasingly offers opportunities to empower even worry-free consumers with a wider range of options for managing their finances. This month, PYMNTS examines how BNPL is influencing consumer behavior across a wide swath of demographics.

Removing Friction at Checkout

Consumers abandon up to 75% of online shopping carts, and reducing that rate provides retailers with a significant opportunity to improve sales and revenues. Many factors can impact cart abandonment, from difficult website navigation to a slow shopping process, but 6% of consumers abandon carts due to a lack of payment options, while 18% give up due to price. Adding BNPL to retailers’ payment options can address both concerns and may even encourage buyers to make additional purchases.

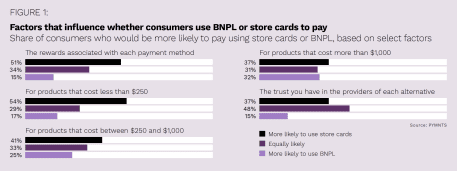

BNPL is gaining traction among consumers in general as a low-friction and easy payment option. A recent PYMNTS survey found that 42% of consumers were interested in BNPL because of its ability to spread payments over time, but 33% said they were attracted by its ease of use and convenience. BNPL also reduces the friction associated with increasing the amount of a customer’s final purchase. Even so, BNPL has frictions of its own to tackle. As BNPL becomes more popular, it also becomes a bigger target for bad actors, and BNPL providers face the same need as other payment providers to balance convenience with security.

BNPL as a Credit Alternative for Worry-Free Shoppers

As the number of providers offering BNPL has increased, so has the variety of BNPL services and products available. Common BNPL features include four or more installment payments with no interest, but providers are creating many variations on that theme, with some offering as many as 30 installments.

Other approaches are permitting customers to use the existing limits on credit cards to secure BNPL loans. Under such an option, the provider places a hold on the customer’s credit card for the full amount, then reduces that hold as each installment payment is made, usually with that same card. The hold proves that the consumer is able to pay off the full amount, removing the need for a credit check. It also enables consumers to make use of credit limits without raising their debt ratios or accruing interest. If the installment payments are made from the same card, the consumer may even collect rewards.

Financially worry-free consumers with good credit or access to credit thus present a promising opportunity for BNPL products that can make use of that credit. While these consumers may not have difficulty finding other means to pay for purchases, they are interested in alternative credit products that help them budget. Forty percent of worry-free consumers surveyed who have not used a credit card in the past year said they are concerned about overspending, and 35% said they avoid credit cards because of high interest rates. Moreover, 43% of worry-free consumers said they would be interested in using BNPL for expensive, one-time retail purchases, and 24% would consider it for medical expenses.

As BNPL providers and retailers plan for the future, the expanding interest in BNPL will undoubtedly reveal new and different ways shoppers can make use of these products. Providers will want to give careful consideration to how different consumers may want to use BNPL and the value it can add to their shopping experiences.