For a sizable share of consumers, embedded lending options such as buy now, pay later (BNPL) would be their first choice of payment method at their preferred stores, PYMNTS Intelligence reveals. As such, those that do not offer the option risk alienating their shoppers.

By the Numbers

The PYMNTS Intelligence report “The Embedded Lending Opportunity,” commissioned by Visa, drew on a survey of more than 8,000 consumers in Australia, Germany, India, Japan, the U.K. and the U.S. to examine consumer preferences around embedded lending — any credit tool or capability for which borrowers apply directly within the merchant or provider’s platform.

This includes the option to apply for a new credit card, an installment on an existing credit card or a BNPL service, as well as dedicated apps or financial services platforms that provide cash advances or instant loans.

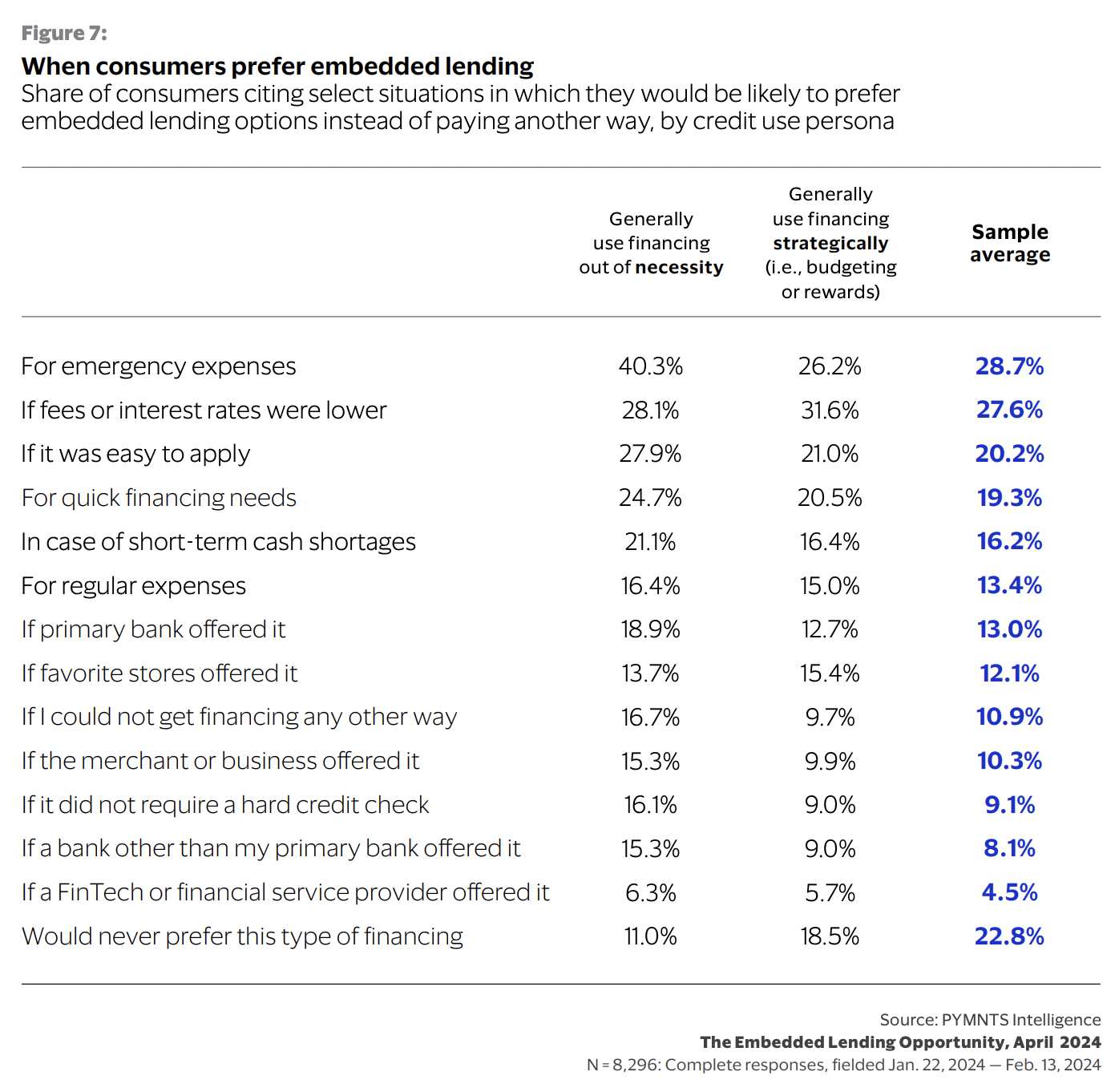

The study found that 12% of consumers would be likely to prefer embedded lending options instead of paying another way if their favorite stores offered it. That share jumps up to 14% for those who generally use financing out of necessity and 15% for those who generally use financing strategically, such as for budgeting or rewards.

The Data in Context

“It’s never been more important for people to be able to hang onto their cash, as more consumers are looking to use BNPL to pay for the necessities of life … all the way around to fun things like travel and entertainment,” i2c President Jacqueline White told PYMNTS in an interview in January.

Plus, for Walmart, BNPL may offer the means by which the retail giant pushes even further into financial services and toward super app status. It has begun offering BNPL loans via One and Affirm at some locations, per recent reports, making it available for purchases ranging from $100 to as much as a few thousand dollars. The categories range from electronics to jewelry — and notably, not groceries.