Headlines show the employment picture is brightening a bit, economies are reopening … and perhaps, just perhaps, U.S. households are feeling more sanguine about their own financial footing.

PYMNTS’ research since March 2021, collecting input from more than 2,200 consumers each month, show that personal/household savings have dipped in recent weeks, across most, but not all segments. On balance many people are in good enough financial shape to weather surprise shocks to their wallets.

Stimulus payments and unemployment checks helped, there’s no doubt about that.

But there might be some warning signs in the mix for some paycheck-to-paycheck consumers — namely, that the preparedness to weather financial shocks is still precarious.

In past studies, done in collaboration with LendingClub, we’ve segmented consumers into several different financial profiles.

Read also: Reality Check: The Paycheck-To-Paycheck Report

As many as 131 million consumers live paycheck to paycheck, a status wherein individuals and consumers have trouble making ends meet. Within that cohort, into which 57% of the population falls, there are paycheck-to-paycheck individuals who struggle to pay the bills (about 25% of the overall population, and those who don’t (a bit more than 31% of the population).

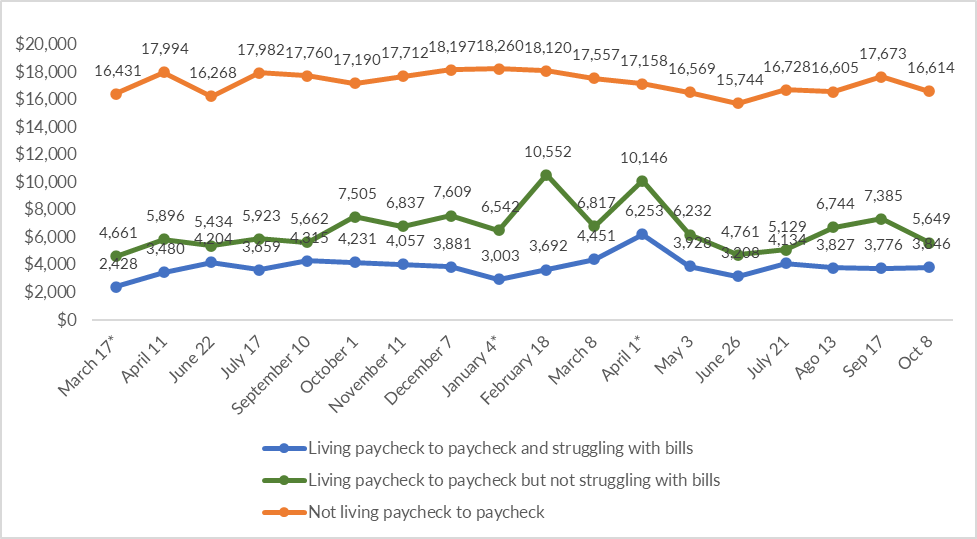

The remainder, at 43% of the population, those who don’t live paycheck to paycheck, might logically be thought of as having the most wherewithal to build up savings. And indeed, that’s the case here. Average savings for this segment, at the most recent reading in October, stood at a bit more than $16,600, down from the previous month’s tally of nearly $17,700, representing a 6% “drawdown.” The “peak” of savings of a bit more than $18,200 seen in the darkest days of the pandemic.

Average Declared Personal or Household Savings, by Financial Lifestyle

Source: PYMNTs.com

The paycheck-to-paycheck denizens are sharply divided in terms of how they’ve “treated” their savings. Those who are living P2P, as we might say, but are not struggling to pay the bills, seem to have spent some of the funds they’d accumulated — relatively drastically, when compared to the individuals/households who are not living P2P.

In this case, we see that paycheck-to-paycheck consumers who are less pressured depleted their savings by about 23% month over month, to a recent $5,649. And the amount saved is far below the pandemic peak of more than $10,552, indicating that this demographic might have been drawing down funds to make sure they weren’t struggling to pay the bills. One wonders, too, if the onset of holiday spending has led to at least some drawdown.

The only subset that did not deplete savings was found in the P2P segment of people who are struggling to pay the bills. Here, we see that savings increased by 1.8% month over month to an October reading of $3,846. Notably, the savings are significantly below $6,253 that marked this group’s zenith. A “tick” up in the most recent savings indicates, perhaps, some caution about near term financial stability. That caution seems warranted, given the fact that 18% of people who live P2P and struggle with bills would be unable to meet an unexpected expense costing $400, far outstripping the 1.9% of similar responses from those who do not live paycheck to paycheck.

The data show continue to show, then, that the financial preparedness to deal with life’s unexpected shocks is uneven across the board. Some consumers will be able to grapple with the challenges, while many people living P2P will find their cash cushions inadequate.