Revelations around the extent of paycheck-to-paycheck living are an eye-opener, with high-earners and strong credit scores living one experience, and those earning less or struggling with monthly bills having a very different time making monthly expenses and enjoying a few frills.

Credit use and monitoring for those living paycheck-to-paycheck and struggling a line of demarcation, as we might expect. Looking deeper into patterns among these groups, we find specific ways that struggling consumers particularly are interacting with and watching credit.

The New Reality Check: The Paycheck-To-Paycheck Report Credit Edition, a PYMNTS and LendingClub collaboration, the latest in this series, draws on a survey of over 2,300 U.S. consumers and finds that 64% of consumers were living paycheck to paycheck in March, a 2-percentage point increase over February, and consumer groupings have distinct attributes.

Get your copy: New Reality Check: The Paycheck-To-Paycheck Report Credit Edition

- 33% of Paycheck-to-Paycheck Consumers Are Less Likely to Be Using Credit

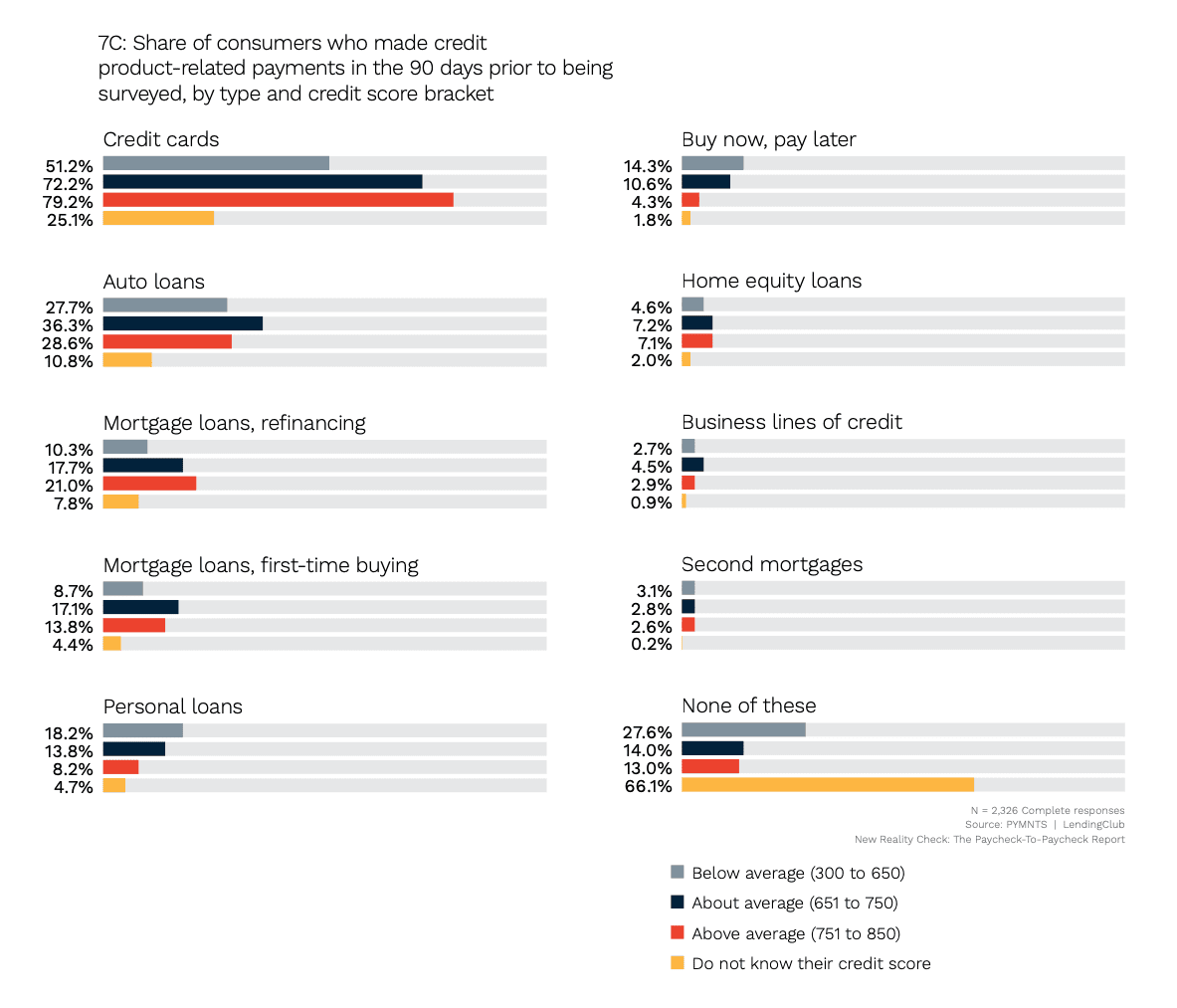

While 64% of all respondents report possessing at least one credit card, paycheck-to-paycheck consumers struggling to meet monthly expenses are considerably less likely to use credit.

With paycheck-to-paycheck consumers 33% less likely overall to use credit, the study states that “24% of these consumers said they had not made a credit product-related payment in the 90 days before the survey. Respondents living paycheck to paycheck with issues paying bills reported even less credit usage, with 31% of these consumers saying they had not made payments related to a credit product in the last 90 days.”

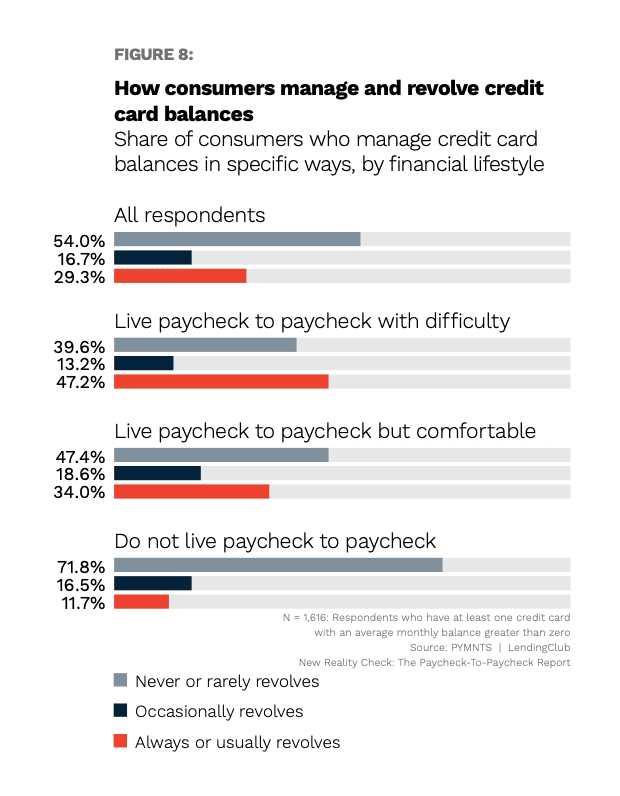

- 29% of credit card holders “always” or “usually” revolve their balances

Our research found that consumers who “always” or “usually” revolve credit card balances average three credit cards compared to the two cards averaged by all cardholders.

Additionally, “Among cardholders living paycheck to paycheck, 34% of those without issues paying monthly bills and 47% of those who struggle to pay their bills ‘always’ or ‘usually’ have a revolving balance. Just 12% of consumers not living paycheck to paycheck ‘always’ or ‘usually’ revolve credit,” the study states.

- 41% living P2Pcheck and struggling checked credit score at least once in the prior week

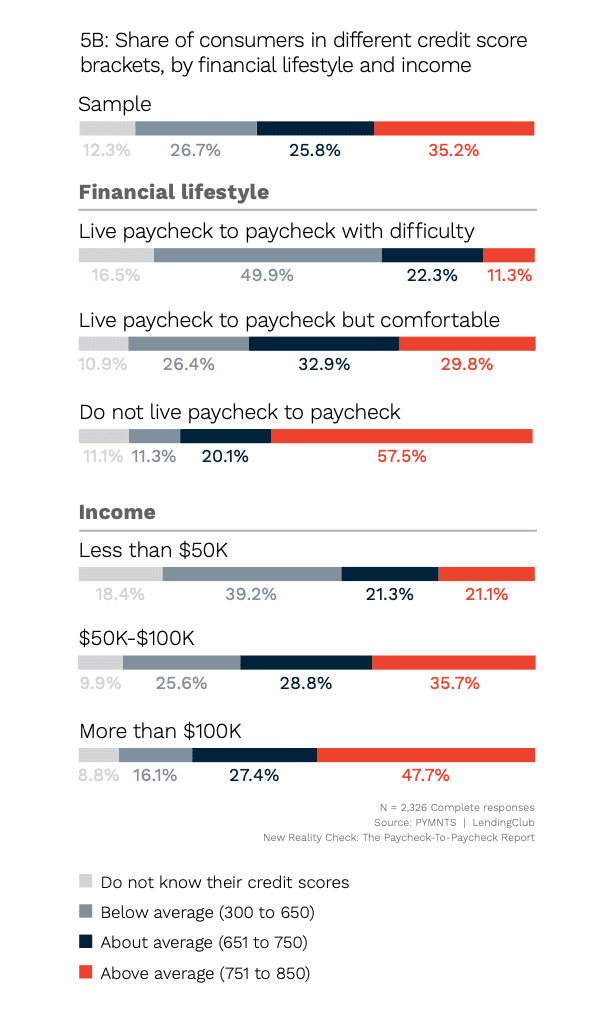

The latest research in the series shows that consumers living paycheck to paycheck and not struggling with bills average credit scores of 694, and those struggling typically below-average with credit scores in the 613 range.

Those with struggles are more concerned with creditworthiness, so it’s not entirely surprising to find them checking scores more often.

Per the study, “Of those consumers who live paycheck to paycheck with issues paying their bills, 20% checked their credit scores in the 24 hours before the survey compared to only 9% of consumers who live paycheck to paycheck without issues paying their bills,” adding that “As many as 41% checked it at least once in the week prior to being surveyed.”

See the study: New Reality Check: The Paycheck-To-Paycheck Report Credit Edition