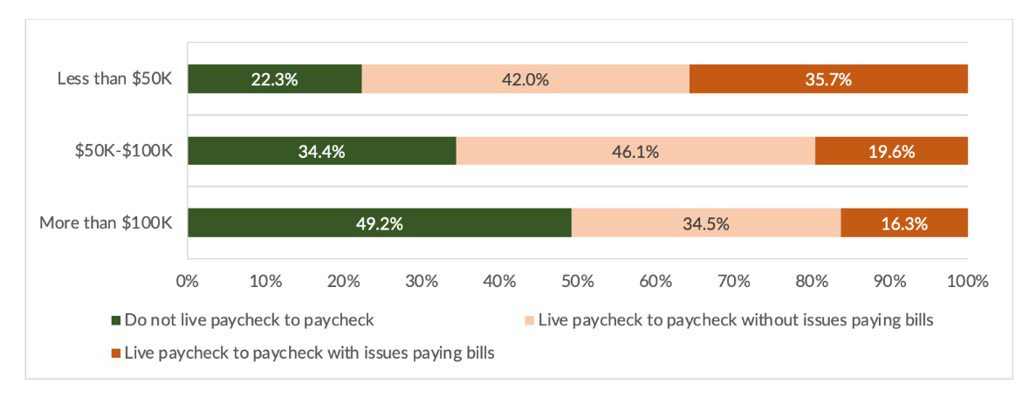

Consumers whose annual incomes exceed $100,000 are hardly skating through current economic conditions. In fact, data shows that as of December, 16% of high-income consumers have trouble making ends meet, a 45% increase year over year.

Inflation has eaten into the budgets of consumers across income and age demographics, as the average U.S. shopper spends 22% of their income on basic essentials such as food, clothing and shelter. This category does not include some costs that most consider necessary, such as transportation or healthcare.

As wage adjustments are still lagging behind rising cost-of-living increases, the share of consumers living paycheck-to-paycheck was bound to include those in higher income brackets. PYMNTS’ recent collaboration with LendingClub, “New Reality Check: The Paycheck-to-Paycheck Report,” details consumers’ financial lifestyles by income demographic.

While still comprising the lowest share across demographics, 16% of higher-earners living paycheck-to-paycheck with issues paying bills is sobering. Putting those percentages into concrete numbers, 9.3 million more U.S. consumers were living paycheck-to-paycheck as of December 2022 than during the previous year. The fastest growing demographic was those making over $100,000, with 8 million of these consumers joining the ranks. It’s small wonder that higher-end grocers such as Whole Foods have seen spending pullbacks.

An end to higher prices may take longer than initially hoped, as the Federal Reserve signals that it will continue to raise rates in response to economic indicators. This is no surprise to consumers, as over half of those surveyed said they expect both higher inflation and interest rates throughout 2023. It may stand to reason that some portion of these consumers may be doing their best to plan for this predicted continued volatility.

That portion of planners may represent a retention opportunity for financial institutions (FIs) and FinTechs specializing in consumer spending. Digitally driven education tips and tools have proven to increase customer loyalty for FIs, so providing budget help and similar offerings may give providers a competitive edge. Although all income demographics may be seeking these solutions, PYMNTS research has found that higher earners are the most digitally connected. Aiming tools towards this demographic may make sense for providers just starting to explore making these offerings available.

Some sector players are already rolling out these tools. In Europe, neobanks like Bunq are hosting features aimed at assisting account holders to better understand their finances. Bunq’s tool helps users set individual budget lines for categories such as groceries or housing expenses and automatically and automatically assigns payments to the correct subaccount. Also across the Atlantic, U.K.-based Starling rolled out a similar “Saving Space” app for its customers.

Stateside, Klarna’s “Money Story” section helps users better understand their spending patterns. Mimicking a Spotify-style year in review, the feature shows users where they spent the most money. Money Story and similar tools are predicted to catch on with the increasing portion of online users who have embraced buy now, pay later programs recently.

Consumers across demographics are buckling down for a longer-than-expected rocky economic road. FIs and related FinTechs have an opportunity to both provide consumers with empowerment through education, as well as use those education tools to strengthen long-term customer relationships.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More