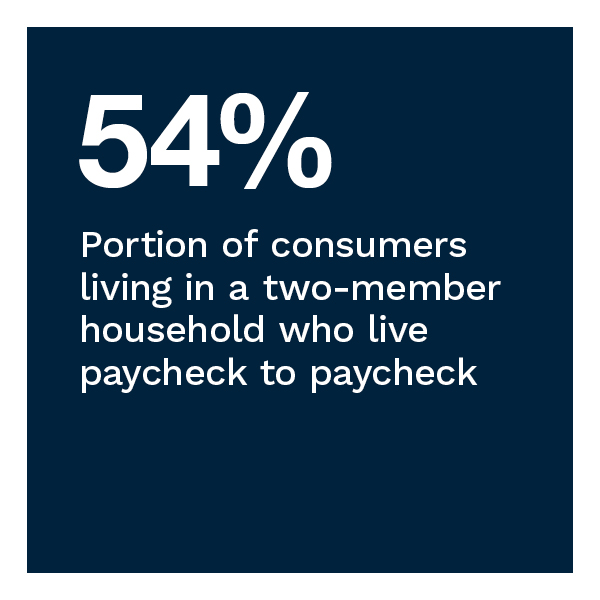

PYMNTS’ research finds that household composition, particularly the ratio of income earners to household members, is central to determining a consumer’s financial stability. Our data shows that those living with friends or housemates are more likely to live paycheck to paycheck, while those living with partners or spouses report lesser financial hardship. At 66%, consumers with children under 18 are 12% more likely to live paycheck to paycheck than those without children. Stage of life also determines the level of dependency among household members, with one-half of Generation Z respondents saying they live with family for financial reasons.

PYMNTS’ research finds that household composition, particularly the ratio of income earners to household members, is central to determining a consumer’s financial stability. Our data shows that those living with friends or housemates are more likely to live paycheck to paycheck, while those living with partners or spouses report lesser financial hardship. At 66%, consumers with children under 18 are 12% more likely to live paycheck to paycheck than those without children. Stage of life also determines the level of dependency among household members, with one-half of Generation Z respondents saying they live with family for financial reasons.

These are just some of the findings detailed in this edition of “New Reality Check: The Paycheck-to-Paycheck Report,” a PYMNTS and LendingClub collaboration. The “Household Finances Deep Dive Edition” examines the impact of household composition on consumers’ ability to manage expenses and put aside savings. The series draws on insights from a survey of 4,602 U.S. consumers conducted from June 5 to June 16 and an analysis of other economic data.

More key findings from the study include the following:

Living with a partner or spouse is the household structure with the strongest financial stability.

Living with a partner or spouse is the household structure with the strongest financial stability.

With costs rising for housing, food and other essentials, managing expenses is far from easy, regardless of the household composition or size. A significant portion of consumers also share financial information and bank accounts and borrow money from parents, siblings and housemates.

Sharing living costs, if not combining financial resources, can help mitigate financial challenges. Our data finds that couples share financial information 87% of the time and share a bank account 75% of the time. Parents are also likely to link financially with children residing in their household: 45% of parents share financial information with their children, and 34% grant them access to a shared account.

Economic reasons prevail in the decision to stay with family members, especially among Gen Z consumers.

A further indication of a correlation of household status, stage of life and financial standing is evident among consumers who decide to stay with family members. At 58%, Gen Z is the most likely to do so. Our study also finds that adult males, at 20%, are somewhat more likely to live with parents than their female counterparts, at 18% — a phenomenon that grows among those financially struggling.

Consumers living with family members are most likely to cite economic reasons for doing so, at 47%, followed by caregiving at 21%. Gen Z is the generation most likely to cite economic reasons, at 50%, and transitional reasons, at 25%, to explain why they live at home.

Consumers living with family members are most likely to cite economic reasons for doing so, at 47%, followed by caregiving at 21%. Gen Z is the generation most likely to cite economic reasons, at 50%, and transitional reasons, at 25%, to explain why they live at home.

Families and couples maintain outstanding credit card balances that are significantly higher, on average, than consumers who live alone.

PYMNTS’ research finds that cardholders living with just a partner or spouse are less likely to have outstanding balances and to use installment plans less than those with children under 18. Couples and consumers with children average higher credit card balances when they do carry balances. Couples average higher credit card balances, at $6,300, and families average balances of $7,200. These balances are 36% higher for couples and 50% higher for families than consumers who live alone.

Download the report to learn how household composition impacts U.S. consumers’ financial lifestyles.

Rising prices for everything from food to housing continue negatively affecting United States households’ financial well-being. Even as consumers continue to adjust spending to make ends meet and put aside savings, 61% of consumers lived paycheck to paycheck as of June 2023, with 21% struggling to pay their monthly bills.

Rising prices for everything from food to housing continue negatively affecting United States households’ financial well-being. Even as consumers continue to adjust spending to make ends meet and put aside savings, 61% of consumers lived paycheck to paycheck as of June 2023, with 21% struggling to pay their monthly bills.