For all the harm caused by the COVID crisis, one clear winner to emerge from the mess is debit. Consumers have turned to debit in battalions as fear of accruing debt in a time of severe economic uncertainty caused a drop in credit card usage.

And however much its high-interest rates dissuade people during what are hopefully the final months of this pandemic, credit cards remain popular and will continue to be so.

PYMNTS January 2021 Online Security And The Debit-Credit Divide, a collaboration with Elan, surveyed nearly 2,500 U.S. consumers to discover what they like (and don’t like) about credit card usage during this strange economic episode. The findings are good news for credit cards.

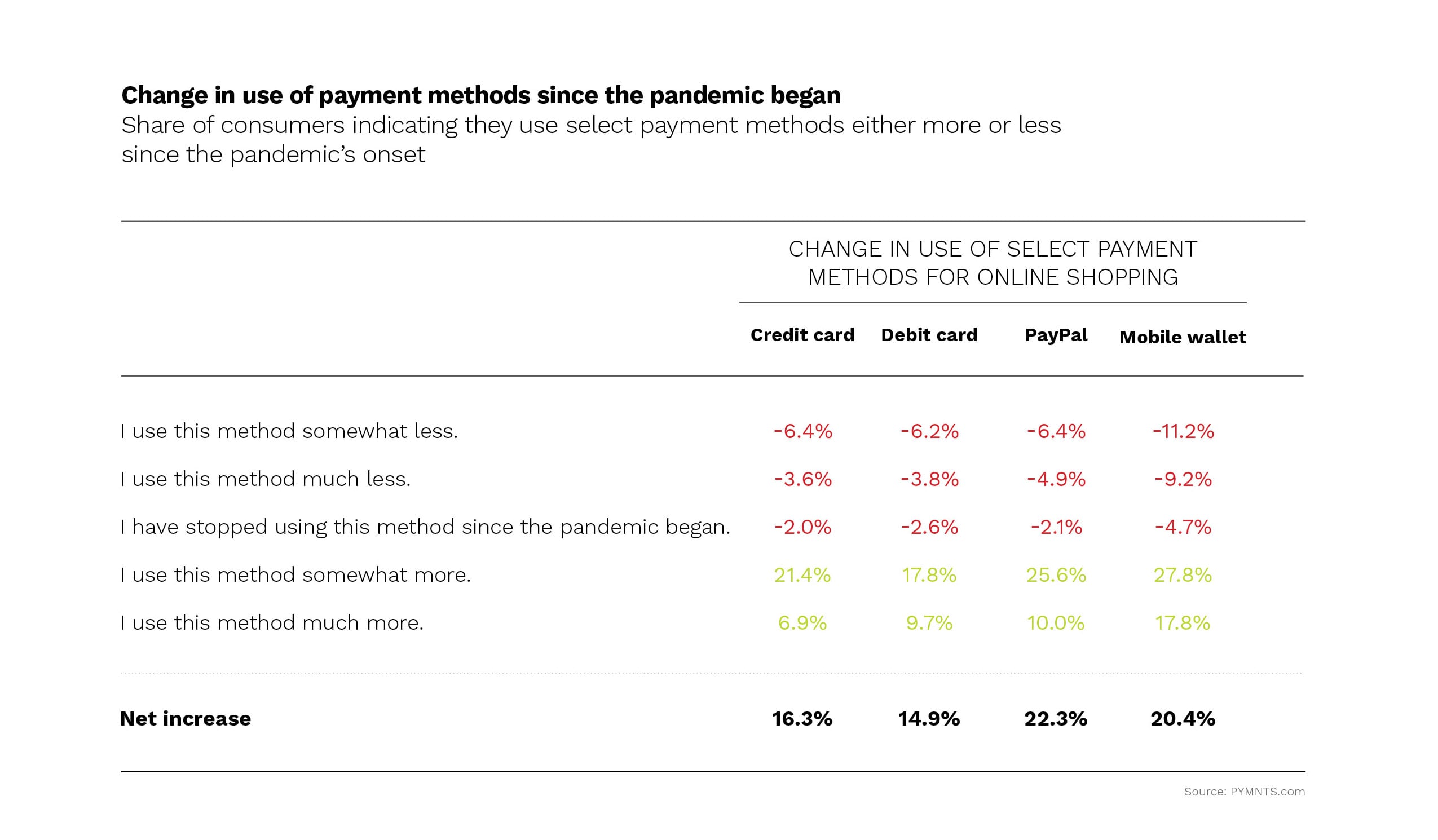

“Our research indicates that credit cards will remain an essential and growing component of the online payment mix,” per the new study: “41 percent of consumers prefer credit cards when paying online, making it the most commonly used payment method, and 28 percent have increased their online usage of the cards since the pandemic’s onset.”

Debit and credit cards and digital wallets saw net usage increases since COVID-19 struck, “yet at least 10 percent of the users of each of these payment methods report using them less.”

Payments Choice Is Profoundly Personal

Payments choice was on parade in 2020 and will stay that way, as a large amount of consumer commerce is shifing permanently online, though physical stores will survive and even thrive.

A great deal of switching went on during that time as cards and apps vied for top-of-wallet status. It’s reflected in the numbers, with Online Security And The Debit-Credit Divide stating, “44 percent of consumers who use debit cards less shifted to other payment methods while the remainder have not adopted payment alternatives. The largest share of these shifters — 18 percent — now favor credit cards while 16 percent use PayPal and another 16 percent tap mobile wallets. These switchers fall predominantly into either high- or low-income brackets.”

Specifically, PYMNTS researchers found that “45 percent who shifted to credit cards make more than $100,000 a year while 38 percent of such shifters make less than $50,000. These proportions are more than double the share of middle-income earners who shifted.”

The conclusion drawn is that “the movement away from debit cards to other online payment methods is driven both by choice, in the case of wealthier consumers, and necessity, in the case of lower-income ones who may need or want financing options for online purchases.”

For Many Cardholders, Security Decides

Debit is less loved as an online payment option for much the same reason you don’t give stacks of cash (or car keys) to strangers: trust. Folks feel safer using debit in-store where they at least have visual reminders of retail security, from ceiling cameras to POS terminal alarms.

Yet ironically, credit card lovers love them for their security as much as any other attribute.

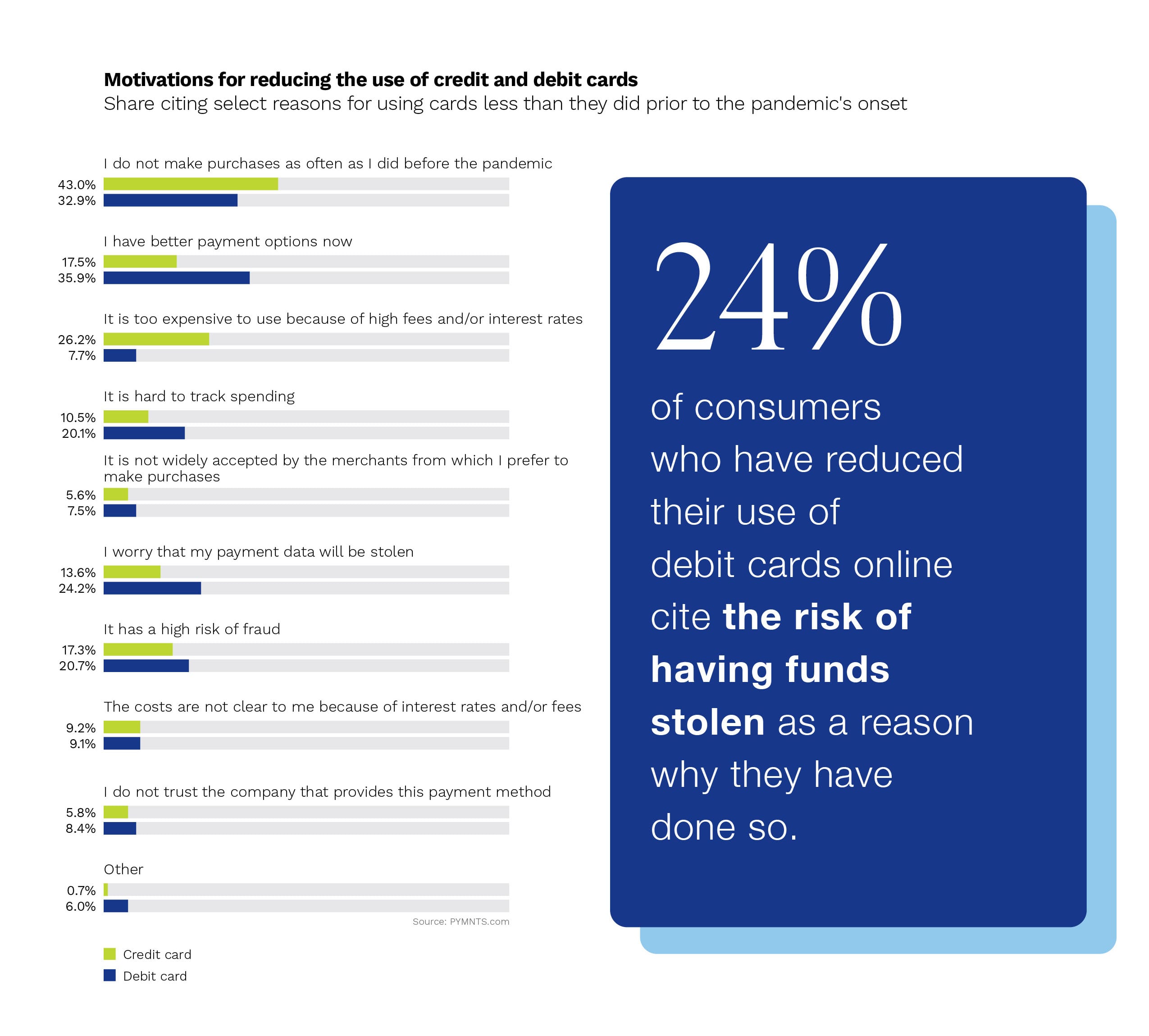

According to PYMNTS Online Security And The Debit-Credit Divide research, “protection against theft of funds is a motivating factor for 35 percent of credit card users — twice the share of debit card users with this view. Consumers also appear to have more confidence in the overall data security of credit cards: 27 percent of credit card users cite data security as a motivating factor while only 14 percent of debit card users do the same.”

When payments power alone doesn’t seal the deal, security often does. So it is in the credit versus debit debate that’s had the volume turned way up since COVID came to town.

“Debit and credit card users diverge in their considerations of security,” per the report, which adds that “24 percent of those using debit less cite concerns that their payment information could be stolen while just 14 percent of those who have cut back their credit card use online cite this concern. The heightened concerns debit card users have around security may relate to the fact that debit cards are linked directly to consumers’ bank accounts.”