Despite the recognition of these threats, many CUs find themselves struggling to roll out innovations for a variety of reasons. Chief among them is their continued reliance on a remote workforce, a factor that has hampered innovation for 81 percent of CUs. Complex internal decision-making processes and a lack of budget are also cited by more than one-third of CU decision-makers.

These challenges have been exacerbated by the pandemic, yet some of these factors are also long-standing issues that CUs have grappled with since PYMNTS began studying CU innovation three years ago.

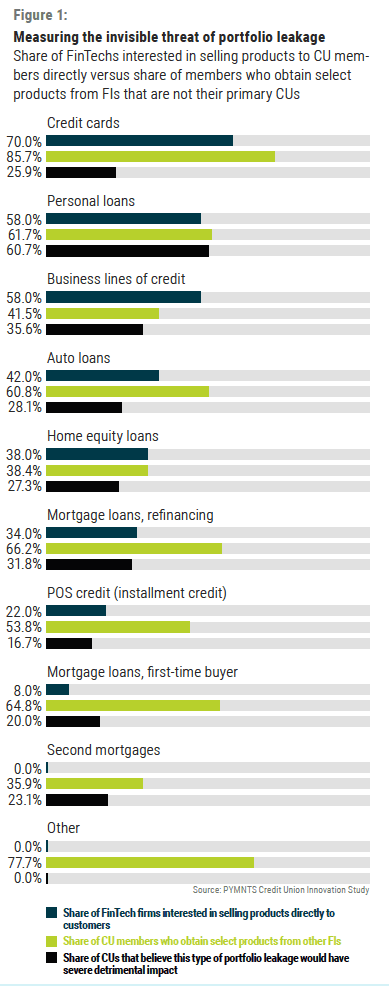

Keeping FinTechs At Bay

Several key approaches can help CUs overcome these challenges and improve on their credit offerings. Nearly 55 percent of CU executives identify having processes in place for employees to make suggestions as an approach that is critical to the innovation process. Testing innovations with members and doing business case and ROI calculations are other factors that about 50 percent of CU decision-makers value within the innovation process.

CUs would also do well to hire outside help to put their innovation plans into overdrive. Nearly 41 percent of CU managers said that partnering with credit union service organizations (CUSOs) can help them get a leg up during innovation, as these organizations can help their CUs avoid releasing new products and services that fall short of members’ needs and expectations.

It is worth remembering that members are more than willing to seek access to innovative credit products from other FIs, even if they might not leave their CUs. It is imperative for CUs to assess the impediments to their credit innovation strategies and act on them without delay.