Keeping pace with and meeting shifting customer expectations is a perennial challenge across the financial services industry. A 2022 study found 51% of retail banks report that keeping up with customers’ changing needs is difficult. At the moment, personalized banking experiences are in high demand.

With the upcoming post-cookie environment, there is an opportunity for financial service providers to leverage zero- and first-party data strategies to create more personalized offerings. According to research, 62% of consumers are willing to share personal information in exchange for more relevant communications. Only 59% of those surveyed are collecting zero-party data and 61% are collecting first-party data, however.

Consumers Want What Traditional Banks More Often Cannot Provide

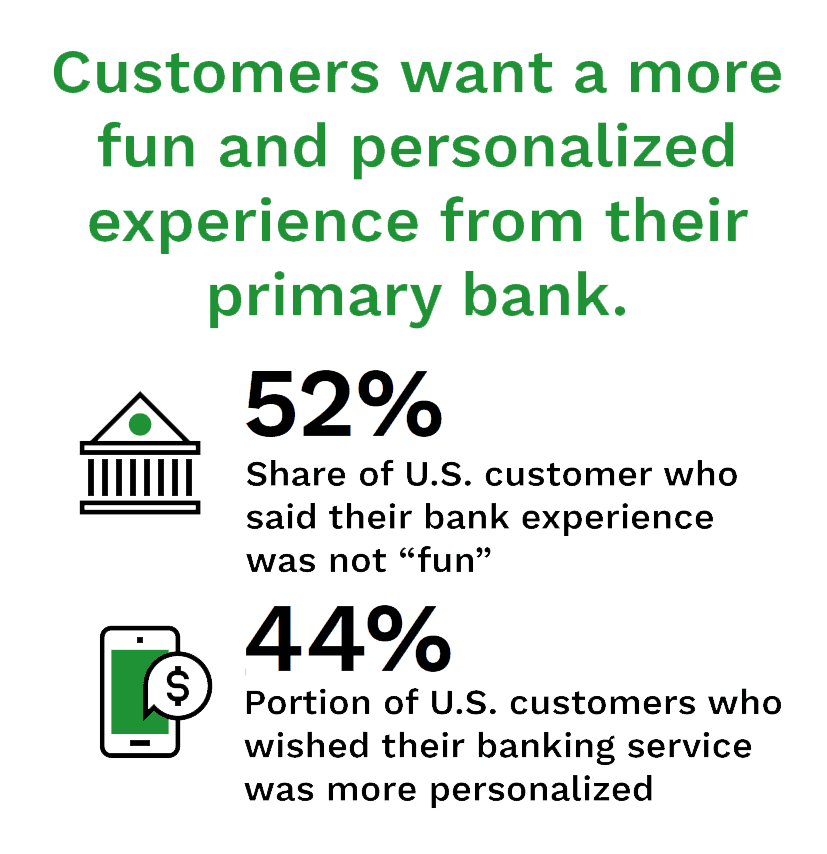

For traditional banks, customer satisfaction is increasingly tied to supporting customers during their most challenging times, which means they want a personalized mix of services. These services may be lacking, though, as three of the top five pain points for customers’ digital experiences all relate to poor personalization stemming from scattered information, such as difficulty receiving relevant content and personalized communications.

Another key aspect of personalization is getting support to the right person in the right place at the right time. One study found that 46% of United States customers said they want help avoiding fees and another 37% said they want to receive account alerts. Another study found overall customer satisfaction increased by 52 points when customers remembered two or more instances of advice. These customers are willing to share personal information to get what they want from banks, including 37% who are comfortable handing over channel preferences, 31% sharing major life events and 30% comfortable providing their household income.

Tapping Data for Improved Personalization

To meet customer demand, more banks are working to introduce personalized insights and customized app dashboards for authenticating users. Designing mobile banking dashboards to display key account information and streamline navigation are keys to successful user experiences, for example.

Customers — not products or business lines — are at the center of strategy, so data governance and a well-structured data program are prerequisites for success. Banks are still adjusting, according to a report. Only 9% have a full suite of machine learning models capable of driving personalized engagement at every touch point and a mere 8% are able to use machine learning to apply predictive insights. Data science teams should follow a standard protocol to develop artificial intelligence (AI) tools, but only 16% can say they do, slowing build times and limiting personalization initiatives.

Building Wealth With a Wider Net of Services

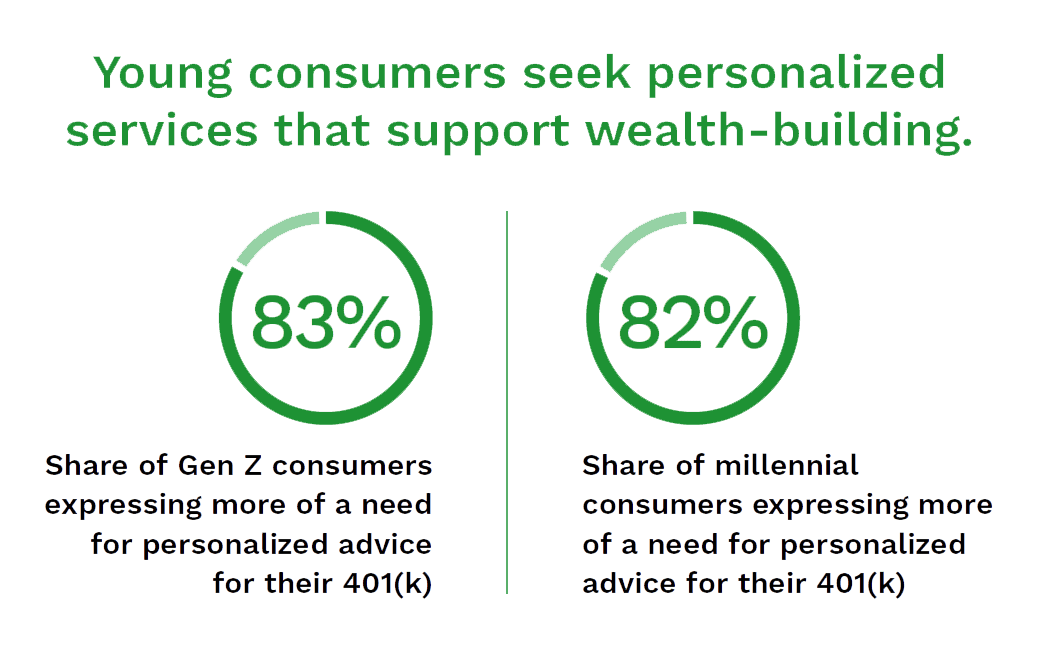

Younger consumers are more interested in financial wellness tools, like online options to help save for retirement, build an emergency savings fund and manage debt. Generation Z and millennials expressed more of a need for personalized advice for their 401(k), at 83% and 82% respectively, than the 79% of Generation X and 67% of baby boomers who feel the same way. Considering how PYMNTS research found Gen Z consumers are nearly three times less likely to have an open mortgage than baby boomers and seniors, it is also important for the industry to provide more tools to navigate a challenging homebuying market, for example, as a step toward building financial wealth.