More consumers are primarily interacting with their banks through online and mobile channels than ever before, meaning they are also looking online first when searching for a new FI or additional financial services. These consumers are also coming to FIs’ online platforms expecting to complete application processes virtually. One study found that 8 percent of consumers who were asked to complete onboarding processes by visiting a branch in person or uploading identity documents would rather give up entirely, and 25 percent would head to competing banks instead.

Providing onboarding convenience and simplicity is crucial for both legacy and digital-only FIs, but engaging consumers through this process also means they must understand how consumers’ views of digital identity and privacy are changing as well. Eighty percent of consumers would open new accounts digitally, according to PYMNTS data — a growing preference that appears to be affecting how they view online privacy and the overall level of trust they place in digital ID tools.

Understanding the connection between the expanding digital-first banking world and consumers’ evolved expectations for digital identity processes is vital for banks aiming to capture consumers’ attention and business. The following Deep Dive takes a closer look at not only how consumers’ trust in digital banking solutions has changed within the past few years — especially since the start of the pandemic — but how this has affected their expectations regarding online security and data privacy. It will also examine how banks can upgrade their onboarding processes to meet these shifting needs as well as detail the role emerging authentication technologies like biometrics are playing in this space.

Solving The Trust Conundrum

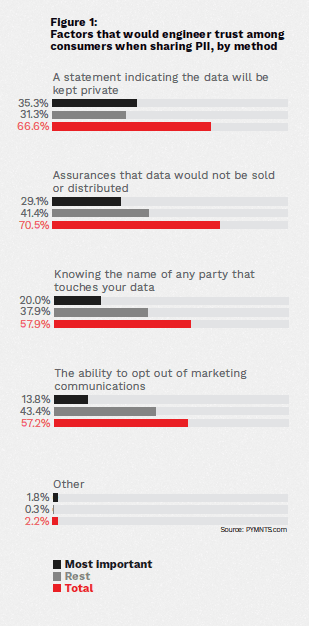

Successfully attracting consumers and persuading them to complete onboarding processes requires FIs to offer security or identification tools they are most likely to trust. Ascertaining which measures today’s individuals are willing to trust can be difficult, however, as digital privacy concerns are changing. The growth in digital fraud in parallel with online banking’s expansion has prompted bank users to express more worry, leading to more customer scrutiny of the security systems banks have in place. One August 2020 report found that 56 million U.S. consumers suffered new account fraud in the 12 months preceding the survey, and 66 percent claimed they expect organizations to do more to protect their PII.

Consumers growing more concerned about fraud are also becoming more trusting when sharing their personal data with banks — as long as they believe these FIs will use their information to swiftly verify their identities and protect against bad actors. Recent PYMNTS research found that 36 percent of consumers are more comfortable sharing personal data when banks make it clear the data will be used to speed up the onboarding or login processes. Another 35 percent of bank customers noted they would be much more comfortable sharing sensitive information if these FIs provided data privacy statements, for example.

This presents a clear opportunity for banks to build trust and strong relationships with this expanding crop of digital-first customers as long as they also keep pace with how consumers’ authentication preferences are shifting. More customers are seeking identification measures that are stronger than outdated usernames and passwords, which can be less secure and a hassle for consumers to memorize.

Biometric-First Banking

Consumers who are banking primarily online or through their mobile phones are instead indicating growing comfort with emerging digital identification tools that rely on other forms of data, notably biometric indicators such as fingerprints, voiceprints or facial recognition. Seventy-seven percent of American consumers said they trust organizations that tap “more advanced” authentication measures to verify their identities. Biometrics are emerging as some of the identification tools customers trust the most, in part because they rely on data that is unique to individuals. Unlike passwords, which have a tenuous connection to the real-world identities of online consumers, fingerprints and voiceprints are inherent physical qualities that are with consumers wherever they go.

Integrating biometrics into banking platforms could therefore prove key for smooth onboarding that digital-first consumers would be less likely to abandon. Bank customers are seeking not only easy, speedy onboarding or login processes but also experiences that speak to their changing views of digital identity and its protection. Banks must ensure they are adjusting their own digital identification strategies and tools accordingly.