This week, the latest spate of data from the government on spending trends will be released.

Retail sales data will track consumer demand for finished goods that fly off merchants’ real and virtual shelves. The Personal Consumption Expenditures Index will give a sense of how much of the monthly paycheck is being spent, overall, on tangible goods and services.

In addition, the latest Consumer Price Index (CPI) data drops on Wednesday. Core CPI is expected to increase 3.6% year over year. Car insurance, rent and healthcare are the categories within the index that are expected to lead the easing of price pressures for this latest reading. Generally speaking, for the core data — which does not include food and energy — consensus holds that CPI rose 3.6% in April, down from the March reading of 3.8%.

Continued Pressure

Despite the expected moderating pace of inflation, PYMNTS’ own data indicate that there are pockets of pressure on the purse strings, tied to a few key categories of everyday essentials.

Call it a divergence of sorts: Inflation’s stickiness may be ebbing, at least just a bit. By way of contrast, the stickiness of prices paid to keep daily life going is well-entrenched — nobody’s adjusting them lower even though the pace of the cost inputs themselves might be moderating. There’s a disconnect between what the high-level data tell us and what the costs of food, shelter and clothing really do — and how higher prices impact the decisions of how we juggle and pay for the “must haves” and the “nice to haves.”

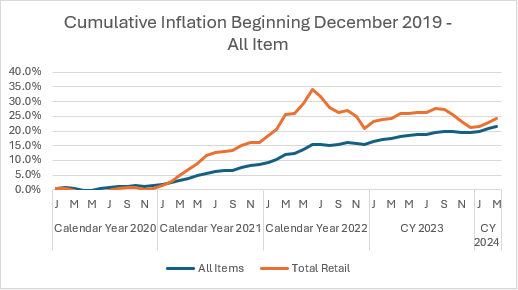

The accompanying chart gives a long-term view, as calculated by PYMNTS Intelligence, of inflationary trends. We are leagues above the inflationary pace seen since the darkest days of the pandemic, and retail-focused inflation has in fact been picking up into the most recent months of 2024. Cumulatively speaking, retail items are roughly 25% more expensive than had been seen since the pandemic; the cumulative impact across all categories of spending has been comfortably above 20%.

And in terms of actual spending: PYMNTS Intelligence found that of more than 1,700 consumers who purchased non-retail items through the past 12 months, the average purchase as of the latest quarter was $85.40, down from $88 in the midst of the pandemic, at the end of 2021. The tally’s roughly the same for groceries, at about $93 in the latest reading, and just about $92 during the pandemic, as measured across 2,500 responses.

Moving the Levers

The read across is stark: If purchases are stagnant, but inflation is on the rise, and merchants’ prices have gained ground too, then it follows that consumers are either 1) reducing the number of items they are buying 2) and/or trading down to lower quality products.

The need to do so comes as consumers feel that their wages have not kept up with inflation. A considerable majority of us — at 85% of consumers — have noted that wages had not kept pace with inflation. And through the last several months, though credit had been a preferred way to plug the gap between funds coming the door (via paychecks) and what needed to lead the coffers, the rising cost of debt has weighed heavily.

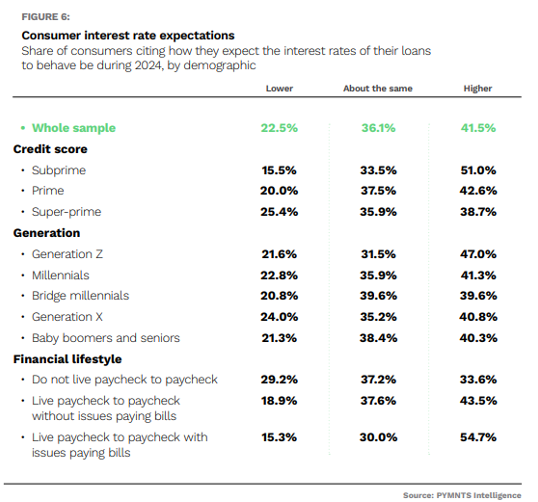

As PYMNTS Intelligence has reported, during the first quarter of this year 42% of consumers said they’d expected the interest rates of their loans to increase during 2024. As many as 20% of paycheck-to-paycheck consumers said they expected to have to dip into savings to pay their monthly bills.

More recent data have found that the use of cash was 34% higher for groceries and 23% for retail, which indicates a cognizance that dialing back on credit use, and using cash while trading down may be optimal strategies at present. Indeed, 32.5% of consumers at the end of last year said they had reduced the quality of the items they purchase, and the share cutting down on nonessential spending was nearly 62%. Perception is reality, as perceived inflation has been 29% for retail purchases and, on average, 23% more at the grocery store, as viewed since 2022.

“Whatever the monthly percentage is and whether it is up or down from the month before isn’t relevant to them. The average American’s view of inflation and the inflation rate is shaped by their costs — what’s left in their checking account after they buy the basics, pay the mortgage or the rent and their monthly bills — not the government’s monthly inflation report card for what’s true on average,” Karen Webster noted last fall.

The data this week may offer scant consolation for consumers.