Much focus has been given to fundamentals like the payment technologies needed to support features from transactions on real-time payment rails to instant cross-border payments. When it comes down to it, though, some financial institutions are better poised to take on new features and improve current ones.

How much does IT infrastructure and confidence in core processing contribute to success?

The latest Innovation Readiness Playbook surveyed more than 200 bank executives to reveal the role that core processing and IT infrastructure play in innovation performance and strategy.

The study categorized financial institutions into four groups:

- Core/IT-enabled: FIs that believe they are able to effectively leverage both of these systems to support innovation.

- Core-enabled: FIs that consider only their core systems to be effective.

- IT-enabled: FIs that consider only their IT infrastructures to be effective.

- Core/IT-deficient: FIs that feel neither system is effective.

Readiness Levels: Does Size Matter?

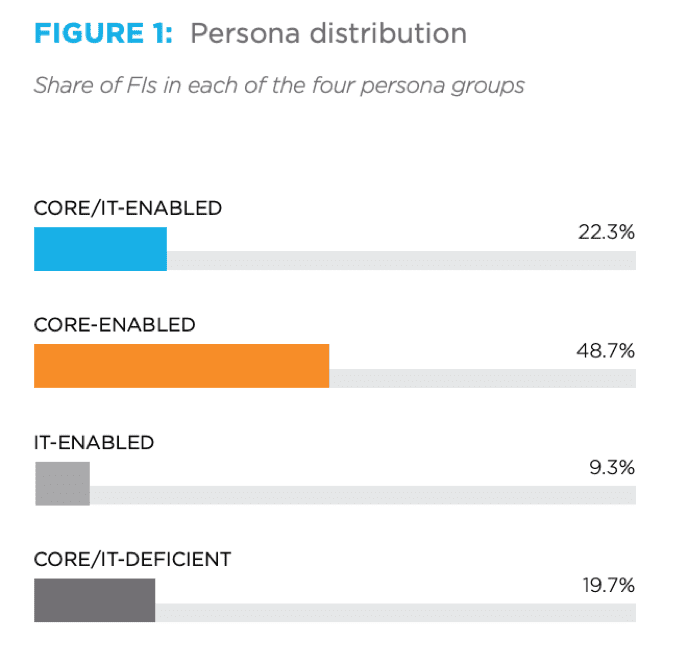

Just 22.3 percent of all FIs consider both their core and IT systems effective for innovation, while 19.7 percent believe neither is. That means more than three-quarters of FIs do not have confidence in both their core and IT systems’ abilities to support innovation.

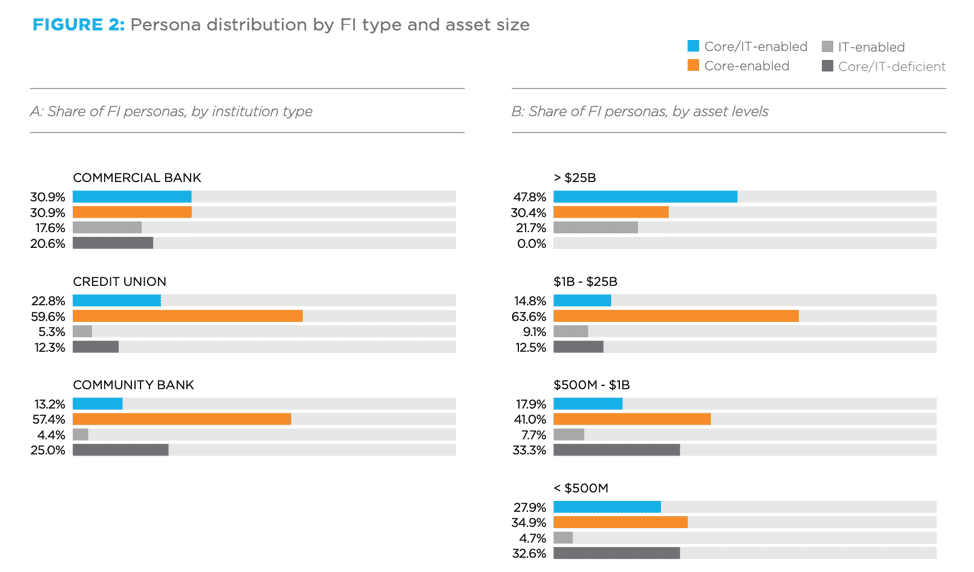

It’s no surprise that commercial banks and those with larger asset holdings are more likely to be core/IT-enabled. It makes sense that institutions with larger budgets might also have dedicated IT departments. Commercial banks make up the greatest share of core/IT-enabled FIs at 30.9 percent, compared to 22.8 percent for credit unions and 13.2 percent for community banks.

Smaller FIs are more likely to be core/IT-deficient. Institutions with assets between $500 million and $1 billion and those with below $500 million in assets make up 33.3 percent and 32.6 percent of core/IT-deficient institutions, respectively.

Size and budget are not necessarily the be-all and end-all, though: 12.5 percent of medium-to-large FIs with between $1 billion and $25 billion in assets are core/IT-deficient, while a considerable portion of smaller banks have effective core and IT systems. FIs with assets below $500 million comprise a greater share of core/IT-enabled FIs than those with between $1 billion and $25 billion.

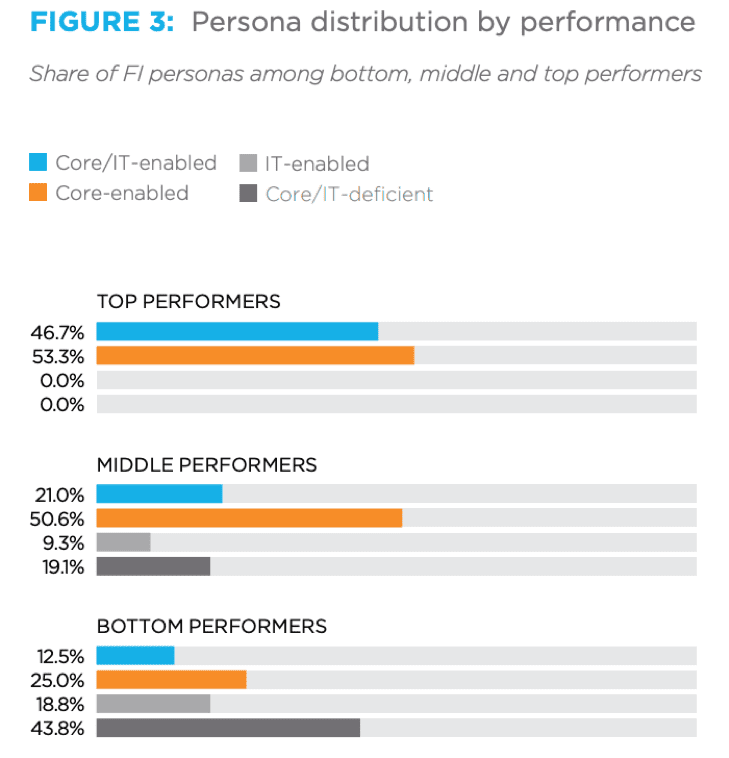

What is clear is that the banks that possess or have access to effective core processing systems and IT infrastructures are better innovators. The top-performing FIs in the Innovation Readiness Index are far more likely to be core/IT-enabled, while the lowest performers are more commonly core/IT-deficient. Nearly half (46.7 percent) of top performers are core/IT-enabled, compared to just 21 percent and 12.5 percent of middleand bottom performers, respectively. In contrast, 43.8 percent of bottom performers are core/IT-deficient.

Areas of Innovation Focus

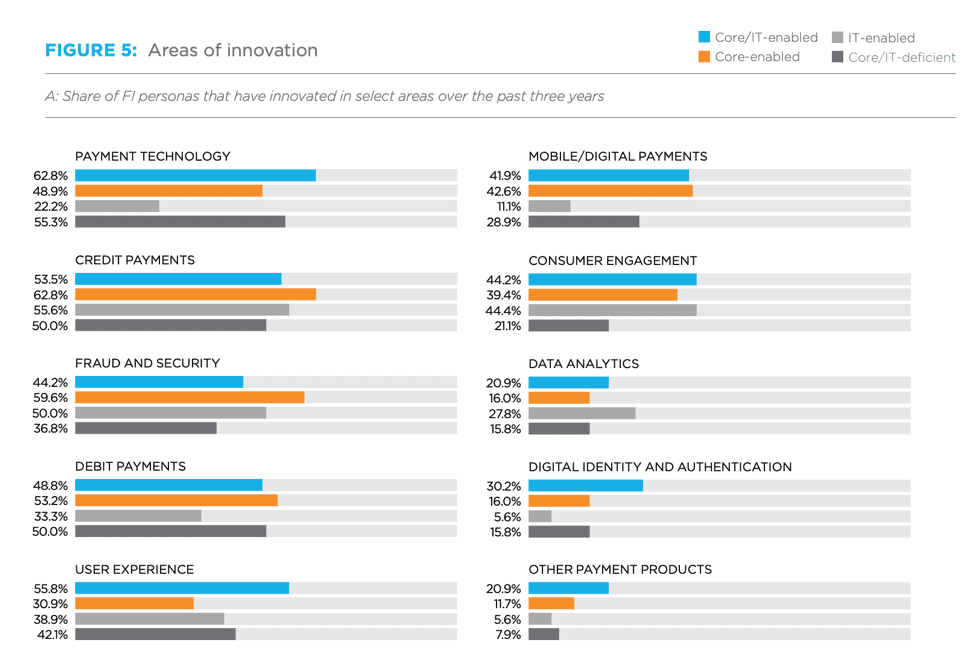

Innovation can mean different things to different businesses, of course. When asked about areas of innovation focused on over the past three years, payment technology was cited by roughly a majority of core/IT-enabled FIs (62.8 percent) and core-enabled FIs (48.9 percent), but also by core/IT-deficient companies (55.3 percent). Interestingly, core-enabled FIs over-indexed for a number of innovations: credit payments (62.8 percent), fraud and security (59.6 percent), debit payments (53.2 percent) and mobile/digital payments (42.6 percent).

Digging deeper into products, over the past three years, core/IT-enabled FIs made up the largest share, innovating in 13 of 19 features. Among the leading areas of interest for this group were digital wallets (55.8 percent), digital identity (41.9 percent), contactless payments (39.5 percent) and real-time payments (39.5 percent), all of which can be considered comparatively large innovations.

Digital wallets, P2P payments and real-time payments are areas in which core and IT-enabled FIs also have great future interest.

Core/IT-enabled banks identify fewer impediments to innovation compared to other banks. While 36.8 percent of core/IT-deficient FIs view inflexible technology systems as impediments, just 14 percent of core/IT-enabled ones say the same.

The top inhibitor cited by core/IT-enabled banks are regulation and compliance requirements that are too burdensome, mentioned by around one-third (34.9 percent). FIs that have confidence in both their core and IT systems are less likely than other banks to perceive innovation barriers across the board.