The pandemic has prompted consumers of all ages to sharpen their focus on planning for their financial futures, including the unexpected. This has resulted in a new generation of consumers entering the life insurance market — and many of them are young and interested in learning more about policies and options on their preferred channels.

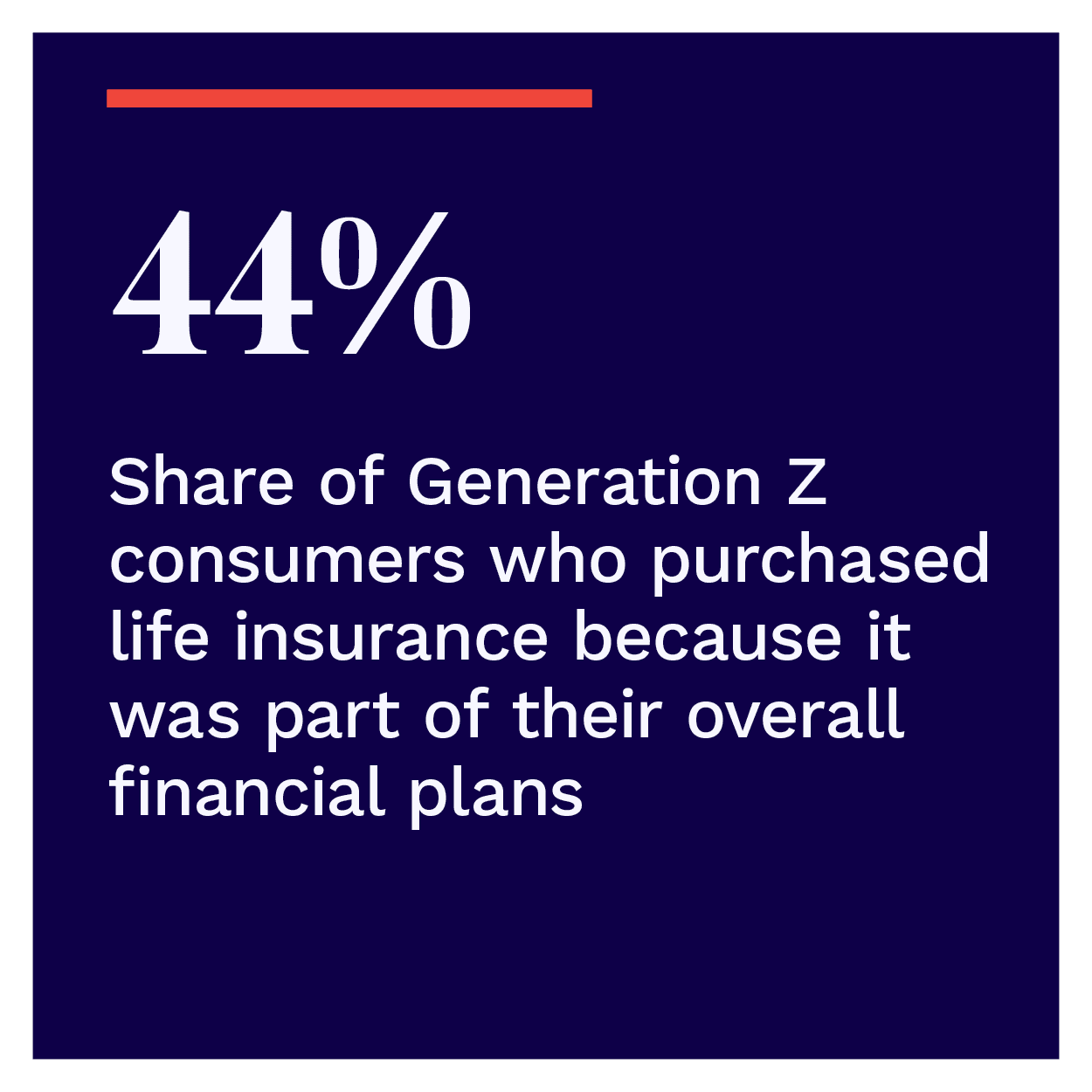

Consumers are also becoming more open to purchasing life insurance from sources ot her than their employers and insurance brokers, with 26 percent considering buying policies through their primary financial institutions (FIs). Those who do so are also likelier to be younger — millennials (18 percent) and Generation Z members (20 percent) — and have annual incomes of more than $100,000.

her than their employers and insurance brokers, with 26 percent considering buying policies through their primary financial institutions (FIs). Those who do so are also likelier to be younger — millennials (18 percent) and Generation Z members (20 percent) — and have annual incomes of more than $100,000.

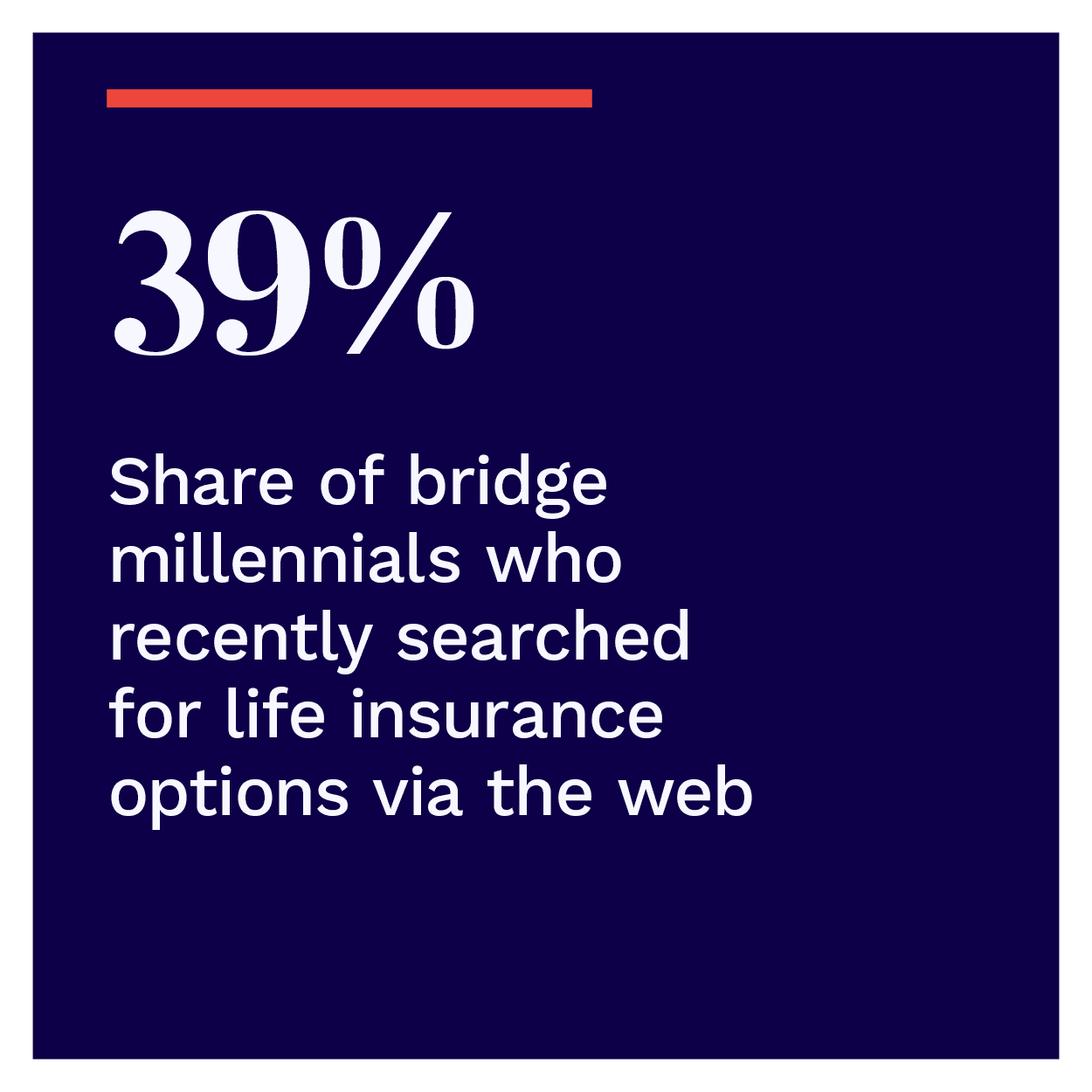

Despite this new shift, younger consumers are still setting a few ground rules when it comes to making life insurance purchases. They are open to new providers and policies — so long as they are allowed to shop, browse discover and ultimately purchase as they see fit. PYMNTS’ research indicates that this increasingly means insurance providers and FIs must lean on digital efforts to reach this valuable new client base.

So, which outreach methods resonate most with younger consumers, and what must insurance providers and FIs do to ensure that they are hitting the mark with their outreach and engagement efforts?

The Life Insurance Engagement Report: Consumers, FIs And The Life Insurance Digital Path To Purchase, a PYMNTS and Franklin Madison collaboration, examines how consumers’ attitudes regarding how they shop for and purchase life insurance are shifting both online and offline. The report is based on surveys of 2,326 consumers and highlights how FIs can encourage consumer engagement with life insurance products.

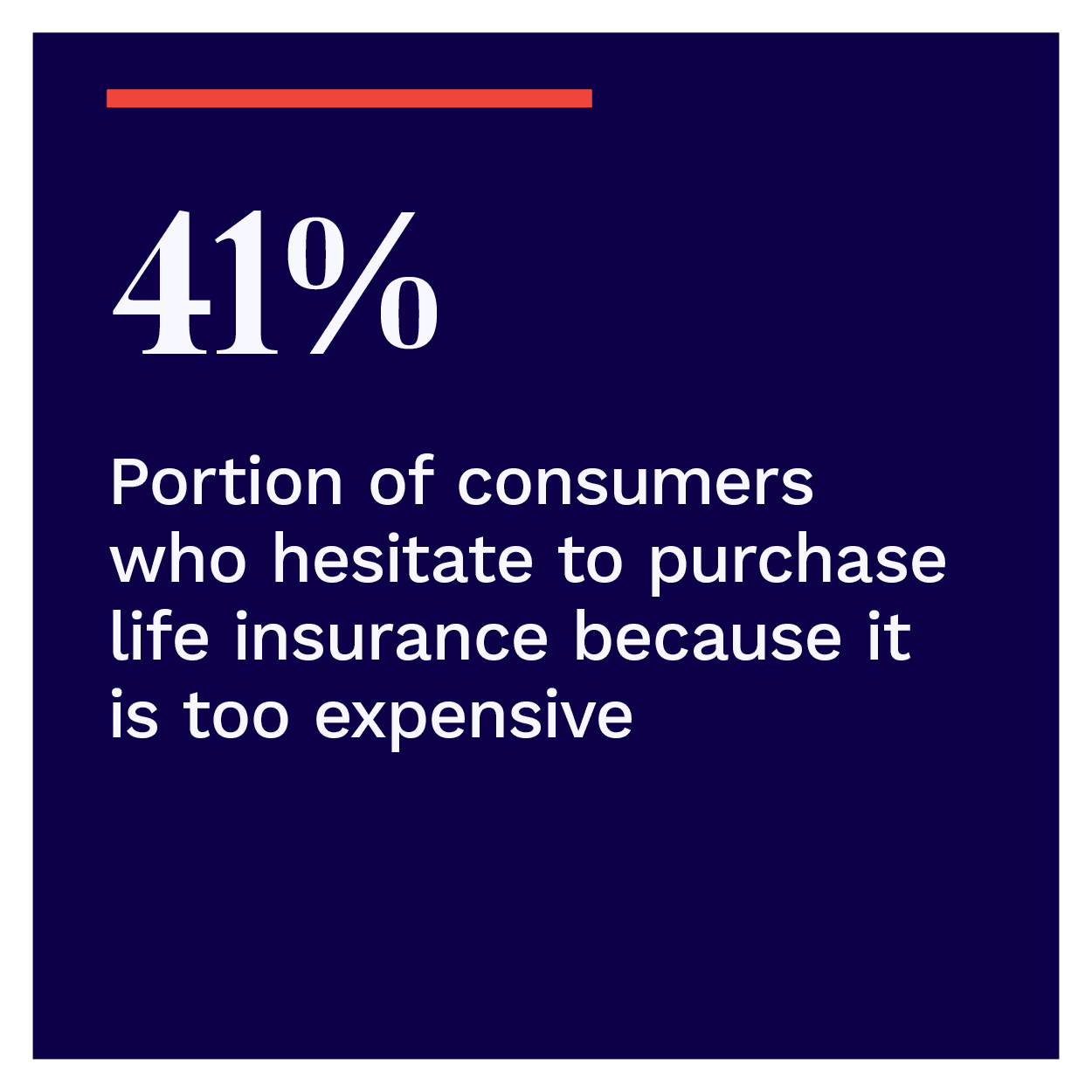

PYMNTS research determined that perceived costliness is keeping many consumers from taking the life insurance plunge, with 41 percent of consumers stating that they have held off on purchasing life insurance because it is too expensive. This points to the need for more robust marketing strategies that can dispel many of the purchasing myths that surround pricing and other common consumer concerns.

PYMNTS research determined that perceived costliness is keeping many consumers from taking the life insurance plunge, with 41 percent of consumers stating that they have held off on purchasing life insurance because it is too expensive. This points to the need for more robust marketing strategies that can dispel many of the purchasing myths that surround pricing and other common consumer concerns.

Even clear marketing efforts can fall flat if they fail to reach their intended audience, however, and this is especially evident when examining FIs’ life insurance offerings. PYMNTS’ data reveals that 37 percent of consumers do not know whether their FIs offer life insurance, and that one-third want more information about their FIs’ product offerings. This signals a missed opportunity among FIs that could be remedied with 360-degree marketing strategies that are informed by high-quality data and focused on content.

While digital channels remain crucial to FIs’ outreach and engagement efforts, this does not mean that consumers are ready to eschew human contact when making their life insura nce purchasing decisions. PYMNTS’ research shows that in-person contact with financial services advisers is how 35 percent of consumers prefer to discover more about life insurance options, indicating that a hybrid approach leveraging both in-person sales and the availability of information online could be the key to satisfying most life insurance customers’ needs.

nce purchasing decisions. PYMNTS’ research shows that in-person contact with financial services advisers is how 35 percent of consumers prefer to discover more about life insurance options, indicating that a hybrid approach leveraging both in-person sales and the availability of information online could be the key to satisfying most life insurance customers’ needs.

These findings highlight only a few of the key insights outlined in the study. To learn more about consumers’ evolving life insurance purchasing habits and about the opportunity FIs have to carve out a larger slice of the market, download the report.