Local and regional banks may have once been more insulated from these trends than other businesses since they are often trusted names within their communities and maintain long-standing relationships with their customers. Yet, PYMNTS’ latest research indicates that these financial institutions (FIs) may be the most vulnerable to losing customers in search of better digital services. How can conventional banks stay relevant and stand out in this shifting digital landscape?

Local and regional banks may have once been more insulated from these trends than other businesses since they are often trusted names within their communities and maintain long-standing relationships with their customers. Yet, PYMNTS’ latest research indicates that these financial institutions (FIs) may be the most vulnerable to losing customers in search of better digital services. How can conventional banks stay relevant and stand out in this shifting digital landscape?

This question is at the heart of the Building A Better App Playbook: The FI Playing Field Edition, a PYMNTS collaboration with Ondot. This series, based on a survey of 3,000 cardholding U.S. consumers, seeks to better understand how spending and banking preferences are changing in the digital age. In the Playbook, we examine how the different bank types — local and regional, national and digital — are responding to these trends, in particular the demand for highly functional mobile card apps.

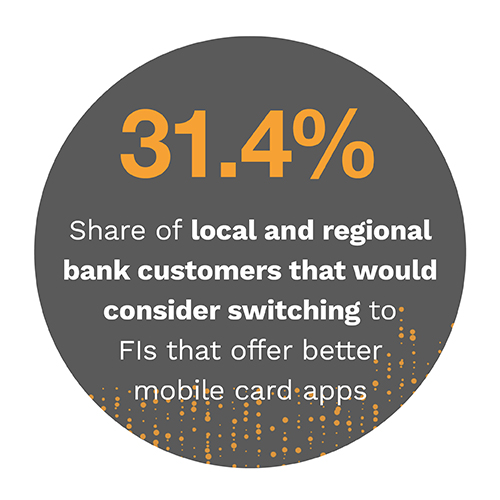

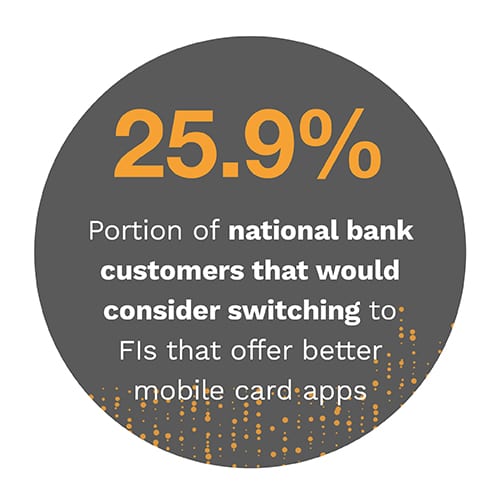

Our research shows that 28.5 percent of cardholders would be at least somewhat likely to switch to FIs that offer superior mobile card apps — and these levels are higher among those whose primary debit or credit cards were issued by local and regional banks. Among this group, 31.4 percent would be at least somewhat likely to switch FIs in pursuit of better card apps. In contrast, national bank customers are less likely to switch FIs, with 25.9 percent of them somewhat or more likely to do so.

Our research shows that 28.5 percent of cardholders would be at least somewhat likely to switch to FIs that offer superior mobile card apps — and these levels are higher among those whose primary debit or credit cards were issued by local and regional banks. Among this group, 31.4 percent would be at least somewhat likely to switch FIs in pursuit of better card apps. In contrast, national bank customers are less likely to switch FIs, with 25.9 percent of them somewhat or more likely to do so.

Our research reveals that different types of banks are in different places when it comes to delivering the specific app features consumers want. For example, 90.3 percent of national bank cardholders report that their card apps allow them to set preferences for notifications and alerts, compared to 82.3 percent of local and regional FI cardholders that report the availability of this feature. Another popular feature — reporting cards lost or stolen — is offered by 86.2 percent of national banks, versus 77.5 percent of local and regional banks, according to respondents. Overall, national banks offer 6.9 separate app features on average, while digital banks offer seven and local and regional offer 6.6.

Our findings on digital bank cardholders demonstrate how consumers’ expectations for mobile financial tools are changing. While digital bank customers are more likely than those at other banks to consider their overall digital offerings very good or better, they are also more likely to be willing to switch FIs in pursuit of even better ones. This suggests that for banks to capture the interest and loyalty of digitally oriented consumers, they must work to continually align their digital products with the demands of their customers.

Our findings on digital bank cardholders demonstrate how consumers’ expectations for mobile financial tools are changing. While digital bank customers are more likely than those at other banks to consider their overall digital offerings very good or better, they are also more likely to be willing to switch FIs in pursuit of even better ones. This suggests that for banks to capture the interest and loyalty of digitally oriented consumers, they must work to continually align their digital products with the demands of their customers.

To learn more about how brick-and-mortar banks can thrive in the digital sphere, download the Playbook.

About The Playbook

Building A Better App Playbook: The FI Playing Field Edition, a PYMNTS collaboration with Ondot, examines what consumers are looking for in mobile card apps and other digital services, and it assesses how different types of banks are delivering them.

There was a time when consumers did not require much more from their local bank than a checking account, savings account and an ATM card. This has changed dramatically in recent years as consumers’ financial lives have migrated to the digital realm. Consumers are paying with credit and debit cards more than ever before, and they are increasingly looking to their smartphones to gain greater control over how they spend and manage their money. It is likely that the COVID-19 global pandemic will further propel these trends, as in-store and cash purchases become less and less common.

There was a time when consumers did not require much more from their local bank than a checking account, savings account and an ATM card. This has changed dramatically in recent years as consumers’ financial lives have migrated to the digital realm. Consumers are paying with credit and debit cards more than ever before, and they are increasingly looking to their smartphones to gain greater control over how they spend and manage their money. It is likely that the COVID-19 global pandemic will further propel these trends, as in-store and cash purchases become less and less common.